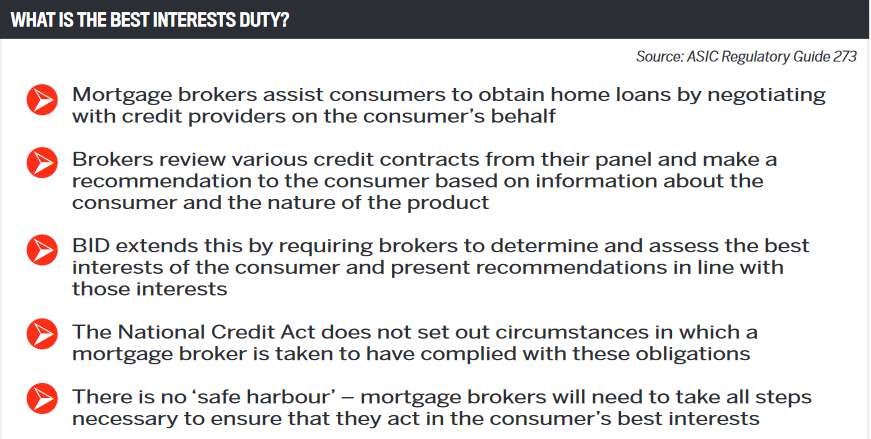

The arrival of the best interests duty in January will come as no surprise to brokers, given the intense spotlight on it following the royal commission into banking and financial services.

Australian Broker sought comment from four brokerages. We asked them how BID would affect brokers’ workloads and processes; what the government is trying to achieve and if it will be effective; and their views on the conflict priority rule.

Co-founder of Peasy Amanda Christmann

“I think BID is a great initiative,” says Amanda Christmann, “but where the government may be getting it wrong is by imposing more administrative work on brokers, which in turn can mean a more arduous process for clients, whereas going straight to the bank could be quicker and easier.”

BID won’t have a significant impact on Peasy’s processes, Christmann says.

“I think the question lies in what is actually in the best interest of the consumer and who gets to make a call on that. As a broker, our role is to advise, based on each client’s requirements and taking into consideration our knowledge, experience and lender panel, which lender/product would suit them better.”

It is not the broker’s role to “impose an option”, she says.

“My belief is that the ultimate responsibility is with the consumer, and I hope BID will play a role in protecting mortgage brokers when it comes to this point.”

Peasy already documents all interactions with clients and follows all of its aggregator’s compliance recommendations.

“Potentially there will be an impact on workload and extra paperwork required; however, as a broker, everything you do is already customer-centric,” Christmann says. “So if any broker needs to make significant changes to their process and current resources to ensure they are acting in a client’s best interest, then there probably isn’t space for them in our industry anyway.”

“The customer is clear that I am operating in their best interest, and they have legislation protecting their rights” Josh Egan, managing director, Astute Melbourne City South and Gippsland

She says most brokers do not recommend products solely to benefit from extra revenue or incentives from lenders.

“If you were to ask me which extra incentives there are from lenders or which lenders pay a higher or a lower commission percentage, I would not be able to tell you.

“These points do not come to our minds when recommending a product/lender, and I believe the majority of brokers would say exactly the same.”

IFA Mortgages & Finance co-owner Anthony O’Flynn

“The government appears to be trying to move brokers towards the financial planning model ... arranging home finance versus handling someone’s life savings is inherently different and should be treated as such,” says Anthony O’Flynn.

The previous duty on brokers to provide a loan product that was “not unsuitable” was confusing.

“If we have a new disclosure that mitigates any doubt that we are working for the client, I think this is a good thing and simply formalises what 99% of brokers had been doing anyway.”

O’Flynn says BID won’t affect IFA Mortgages’ client processes much.“We have been operating within the scope of BID prior to its roll-out and have always placed a lot of value on our disclosures and the continued education of our staff in relation to loan product.”

As a guest speaker at a FAST conference pointed out, “he with the best notes, wins”, O’Flynn says.

“Never a truer word was spoke. If you have the correct discussions with your clients and fully understand their position and intentions; it is very easy to log these discussions and protect yourself if a client has preferences beyond their ‘best interest’. ”

BID will add more compliance work, but “we aren’t talking hours and hours for every file”.

“We are fortunate that our aggregator, FAST, has been extremely proactive in providing up-to-date info and training on BID.”

O’Flynn is concerned about BID’s effect on competition. If brokers are accredited with 35 lenders, they need to understand all the loan products, which could number in the hundreds, if not thousands. “I would hate to see a world where brokers trim their product offering to just a handful of banks – this would stifle competition.”

In his nearly 20 years as a mortgage broker, O’Flynn has never heard of a broker recommending a lender simply to make an extra buck.

“The conflict priority rule is reasonable and affords adequate protection from this occurring.”

Oxygen Home Loans acting general manager Catherine McFarlane

“The government is trying to protect consumers, which is important,” says Catherine McFarlane.

“All brokers should already be putting their customers’ interest ahead of their own, and our brokers do the right thing by their clients without this legislation.”

BID is a good thing if it creates an environment that makes it difficult to put a broker’s own interest ahead of the consumer, as it will increase the quality of mortgage advice, she says.

“BID will also reinforce the value of using a mortgage broker and allow us to further differentiate ourselves from the lenders, increasing our market share in the long term.”

McFarlane says BID has increased the detail required and changed the delivery of information, but this protects the broker as well as the client.

“BID will also reinforce the value of using a mortgage broker and allow us to further differentiate ourselves from the lenders” Catherine McFarlane, acting general manager, Oxygen Home Loans

“It is also a valuable tool to educate clients through the process, empowering them to make their own choices and take ownership of their financial situation. Brokers will need to ensure absolutely everything is documented: the process, notes, conversations.”

Oxygen has been implementing changes for most of 2020 to ensure its brokers are ready, through file reviews and regular industry training.

“AFG has been on the front foot and introduced changes to its system well before it was required, giving our brokers ample time to be compliant. I am confident there will be no further impact to workload or business come 1 January 2021.”

Most mortgage brokers already do the right thing by their clients, McFarlane says.

“Our brokers are driven by a desire to help their clients, above and beyond any differing remuneration. Declaring known conflicts, incentives and commissions has always been a part of our process.

“BID is just another way to empower the client with information to make an educated decision. The challenge I see is declaring those conflicts that may not be known.”

Astute Melbourne City South and Gippsland managing director Josh Egan

“The new BID rule is aimed at ensuring that the prioritising of the consumer’s best interest is dictated in legislation, and that everyone in the industry is meeting the same obligations across the board,” says Josh Egan.

While the industry has always kept the consumer’s best interest at the forefront, he says BID formalises the requirement that brokers understand that the consumer is the priority.

“The customer is clear that I am operating in their best interest, and they have legislation protecting their rights.”

Egan says BID has not changed the way he operates.

“We have had a very strong compliance process for a number of years, with a focus on providing our clients with multiple comparisons and a record of the recommendation we have provided, and, most importantly, what we have based that recommendation on based on their needs and circumstances.

“A big component of what we already do is the education piece to help a client understand why a preference they have may or may not be in their best interest.”

Egan envisages a smooth transition to BID at Astute.

“Not much will change ... as within our client-documented process this is something we have followed for the better part of three years at Astute – we always operate in the best interest of the client.”

Egan says BID requires brokers not to make recommendations that would favour the broker financially or in any other respect at the consumer’s expense.

However, he adds that if the recommendation does prioritise the customer’s best interest and at the same time provides a higher revenue stream to the broker, as long as the client’s best interest is documented and demonstrated and potential conflict declared, it still meets BID requirements.