By

How are the banks progressing on remuneration reforms?

In the Retail Banking Remuneration Review released last April, Stephen Segwick made 21 recommendations aimed at improving how banks pay commission and bonuses to staff and third parties.

Four of those recommendations directly relate to mortgage brokers, including that banks should adopt approaches to the remuneration of aggregators and mortgage brokers do not directly link payments to loan size, and should end volume-based and soft-dollar incentives.

The big four banks committed to implementing all of Sedgwick’s recommendations, a goal that Sedgwick said should be achieved by 2020.

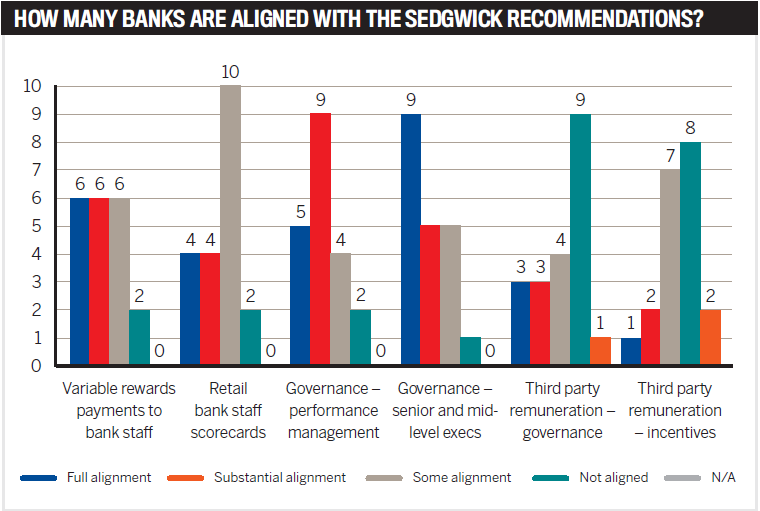

In January, former auditor-general Ian McPhee, who has been tasked with independently assessing the progress the banks have made on implementing the Sedgwick reforms, released his latest report. He revealed that while many banks had been quick to implement recommendations in certain areas – specifically, performance management, executive governance, and culture and conduct – it seemed that there had been little change in the third party remuneration sphere.

According to the McPhee report, 14 of the major banks are now substantially or fully aligned with recommendations for performance management, while just three have reached the same point with third party remuneration incentives.

However, Heather Baister, a partner in Deloitte’s assurance and advisory team, says making changes to third party remuneration was always going to be trickier than implementing other recommendations.

“Some of the recommendations in the Sedgwick review include what the banks can do internally. However, third party remuneration requires a collaborative effort between the aggregators and the broking industry, so by its very nature that will take more time.”

.PNG)

Baister, who specialises in mortgages and securitisation, also stresses that banks are likely to be cautious as they are facing a chorus of conflicting opinions.

We’ve had a huge number of entities professing their views on the mortgage broking industry in recent years – there’s been the ASIC review, the Sedgwick review, and now brokers have been scoped into the royal commission, while ASIC is continuing to do its shadow shopping of mortgage brokers,” she says.

The Combined Industry Forum (CIF), a body consisting of lenders, aggregators, brokers and consumers that came together following the release of the Sedgwick review and the ASIC remuneration review, also released its own report and guidance to the industry in regard to broker commissions.

MFAA CEO Mike Felton says the two reports have the same objectives.

“I believe that if the CIF reforms are implemented as proposed, that should address Sedgwick’s concerns,” he says.

“I don’t see them as being different things; we see them as being one and the same. They’re looking to improve consumer outcomes, improve trust and confidence, and drive sustainability of the industry into the future.”

As Baister points out, there are clearly a lot of different factors at play.

“It’s not as if there’s one set of recommendations that are trying to be implemented – there is fundamental structural change being considered, so I’m not surprised its moving slowly.”

With the royal commission still in its early stages and ASIC conducting ongoing investigations, Baister says its’ highly likely that additional guidance will be released in the near future, will be released in the near future, leaving banks reluctant to implement any changes that could soon be rendered outdated.

"I think any lenders would be very nervous about making a change to its third party remuneration processes and governance as a first mover, for fear of being out of line with the rest of the industry,” Baister says.

“I’m sure there is a lot of work going into what will actually work, what data is available, and what is practical on a cross-industry basis. That’s what’s taking the time.”

With significant amendments still to be made to third party remuneration, many brokers have expressed concerns that their current compensation structure will be altered beyond recognition.

“Certainly there is a fear that if the commission structure does change fundamentally, it will lead to brokers withdrawing from the market, and I’m not sure that’s a good thing,” Baister says.

“If you look at the fact that more than 50% of loans are currently originated via brokers, it’s clear that they play a very valuable role – they’re clearly servicing a market, they clearly help competition, and the service they provide from a customer viewpoint is generally very well received.”

However, while Baister hopes the recommendations will have a minimal impact on broker remuneration, she also acknowledges that other compensation systems are a possibility.

“When you look internationally, there are many other payment models in operation, so it would be rash to dismiss them,” she says. “However, I think the model that we have operating in Australia at the moment is working very well, and ASIC has acknowledged that. Although it’s by no means perfect, they did not see a more recommendable fundamental basis for a model.”

While it’s impossible to predict exactly what changes the forthcoming industry reviews will bring, Baister says the most significant are likely to relate to increased transparency across the industry.

“I think there will be more of a focus on transparency for the lenders in terms of the conversations a broker has with customers, and how lenders can be certain the conversations they believe are happening in regard to NCCP requirements are actually happening.”

Baister also expects the broker industry to demand additional transparency regarding the performance as the loans from the lenders as, currently, that data is not shared effectively.

“I also think there will be increased transparency over performances of individual brokers – for example, if a broker is raising a red flag with one lender, how is that information shared across lenders and the broker’s aggregator?”

For consumers, Baister says there will be an increased focus on the transparency of disclosure where there is vertical integration between lenders and brokers.

“That way, consumers can clearly understand the commissions that brokers are being paid and the relationship that those brokers or aggregators may have with banks when they are ownership structured.”

While there is still uncertainty clouding the future of broker remuneration, Baister says she knows one thing for sure – that the mortgage industry will only suffer if professionals are pushed out.

“I really believe the role brokers play in helping consumers with what is arguably the biggest purchases they ever make – and enabling them to navigate that – is so incredibly valuable that I really think there should and will be a long-term role for brokers in the industry here in Australia.”