By

The start of the new year marks the beginning of the transition from a closed banking system to an open model in which consumers have control of their data and can share it with any institution they choose. Australian Broker examines how the industry should prepare

Australia will soon transition from a closed banking system – in which each financial institution keeps and controls its customers’ information – to one in which customers control their own data.

The new regulated system aims to allow customers to unlock their own financial data and to provide them with a wider choice of financial products and services, while enabling a more competitive marketplace.

In July 2017, the government commissioned the Open Banking Review chaired by Scott Farrell, who was asked to recommend the most appropriate model for Australia.

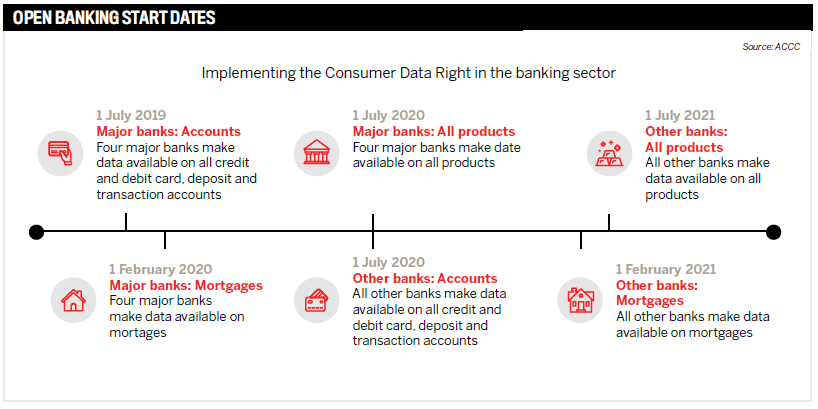

The time frame proposed by the Farrell report, and then accepted by the government, will see mortgage data and recommended financial products made available by July 2020 but with a transition period until 2021.

Originally, major banks’ mortgage data was scheduled to be available from February this year, but the ACCC has deferred the launch of certain aspects of open banking to July, delaying the implementation and launch of the Consumer Data Right (CDR) in the banking sector.

ACCC commissioner Sarah Court said, “The CDR is a complex but fundamental competition and consumer reform, and we are committed to delivering it only after we are confident the system is resilient, user-friendly and properly tested.

“Robust privacy protection and information security are core features of the CDR, and establishing appropriate regulatory settings and IT infrastructure cannot be rushed.”

What CDR means is that consumers will be able to direct major banks to share their credit and debit card, deposit account and transaction account data with accredited service providers from 1 July 2020. Consumers’ mortgage and personal loan data will be able to be shared from 1 November 2020.

Poli Konstantinidis, executive general manager, credit services and decision analytics A/NZ at Experian, welcomes the delay.

“Based on our experience in the UK, we have always believed the implementation of CDR [in Australia] needed to be exercised with care, so we welcome this considered approach to the CDR rollout,” Konstantinidis says.

“The additional time available should be used to increase the awareness of open data among Australians.”

While he believes the ACCC’s caution has been appropriate until now, Konstantinidis warns that open banking should not be delayed any further.

“Greater data sharing will see the ownership of customer data put back in the hands of Australians and give them the power to access better deals,” he says.

“While a true open data environment may be delayed for now, it’s vital CDR is implemented effectively and regulated properly so consumers can have access to the wide-ranging benefits.”

Brokers’ role in open banking

The data that will be made available is substantial; it will include all transaction information across customers’ accounts, including what they spend, their income, all loan details and repayment history.

Stephen Moore, CEO at Choice Aggregation Services, says customers, as opposed to their institutions, will own their banking data for the very first time.

But in order for open banking to work successfully, customers will have to provide permission to brokers to use such data. If they do, it means brokers will also have more insights into their clients than anyone else across the value chain.

Moore says, “All of that is enormously valuable, and the exciting bit about it is how brokers can then support customers in an open banking regime.”

He suggests brokers today know their customers at a personal level better than anyone else does. Brokers are aware of family circumstances, an individual's aspirations, and the ins and outs of what their customers are trying to achieve. The only thing missing until now has been the hard data around banking.

Moore continues, “To me there are two key benefits for brokers: firstly, from an efficiency perspective, we've seen the ridiculous scenario of having to highlight items on a bank statement for expense categorisation – all that disappears, and it’s going to be a far more efficient system.

“Secondly, and this is going to be the main benefit of open banking: having detailed insight into someone’s expenditure, savings, loan payment history, etc., will be enormously valuable from any lender perspective, and it will have a really positive impact on competition, and that’s where the true benefit for customers comes in.”

He adds, “But, naturally enough, it’s more complex. You’ve got lots of data and a myriad of new lenders, so it does mean the role a broker plays in helping customers navigate through a competitive landscape will become even more important.”

Jason Furnell, chief customer experience officer at Loan Market Group, suggests the changes could mean customers are more likely to choose brokers ahead of banks for the best mortgage outcomes.

“Customers trust brokers to do right by them,” he says.

But open banking won’t just benefit the consumer. Furnell suggests it creates a victory for brokers in numerous ways:

Furnell also notes that, in order to take full advantage of the opportunities, brokers need to be digitally savvy. He explains, “If we haven’t seen it already, open banking will certainly signal the death of ‘pen and paper’ broking.”

This means brokers will need to ensure they’re digitally ready for the arrival of open banking, and it might prove too complex and expensive to try to navigate it on their own.

“Customers want to win back their financial identities,” Furnell says. “They’ll want to use their own data to explore new options. And they’ll want experts with the knowledge of products and policies to help them utilise their data for better outcomes.”

How to prepare

A key thing to understand is that it isn’t just the influx of new data that is key to open banking – those are just the facts that will be provided.

Furnell says, “To prepare yourself to make the most of open banking, find an aggregator who is ahead of the tech curve. At Loan Market, we are working on further strengthening our security practices so we are prepared to hold even more client data. Plus, we are evolving our online fact-find so our brokers can collaborate transparently and easily with clients based on the additional customer data.”

Indeed, the most important skill to have will be the ability to collect and store the data in a secure and natural way, suggests Moore.

He says, “What will become fundamental is the ability to analyse and develop insights around that data, and this is where, in fact, we're already talking to a number of vendors to provide analysis tools to help brokers through that process.

“What [then] becomes important – in an environment where more data is shared – is the ability to store, analyse and act on those insights. That will just increase the importance of having the right sharing system.”

Moore also highlights the importance of analysis tools for the mortgage industry.

“There are some of those expense tools around to date. The expense tools are an example of a precursor for some of the things we would be able to do in open banking. But it certainly goes beyond just expenses, looking at income repayment history, loan type, loan details, etc.

“There are a number of people already developing tools in that space, and in fact that whole area will develop quite rapidly.”

But what will truly become critical, aside from analysis tools, is being able to integrate data into brokers’ customer relationship management.

“Otherwise, you're going to have all these disparate systems that do not talk ... the difficulty in managing customer data will just be a cost," Moore says.

“But if you get it right and integrate the data and do so efficiently, then it's going to be a real efficiency gain for the broker market too.”

There is also the issue of cost versus reward to be taken into account.

Moore explains: “At the moment there’s a substantial effort that goes into reasonable enquiry to validate customers’ income and expenses. What open banking will do is remove much of that effort if it gets set up in the right way.”

Furnell adds: “Open banking isn’t new. It’s been part of the world’s largest economies for several years, driven by the operators in the financial sector themselves.”

Aggregators and support

The role of aggregators in developing insights and providing support to brokers becomes critical in this space, especially through the transition period.

Moore says, “At Choice Aggregation we see any open banking supporting tools as an extension of our platform systems ... in fact, we've designed Podium (the platform that we provide to brokers) with Salesforce [a globally leading CRM system] at its core.

"Having a world best practice CRM means we're really building Podium with the future in mind for open banking – the ability to accept analysis tools and the ability to capture data and to manage it all the way through to the process.”

He adds that developing insights will be fundamental to open banking’s future. The risk that needs to be managed is that the more data that is shared, the greater the privacy and cybersecurity risk.