An accountant, a financial planner and a mortgage broker walk into a bar. The bartender has a residential investment property and takes the chance to talk finance, specifically the level of return that can be achieved from property when compared to other asset classes, such as stock market shares.

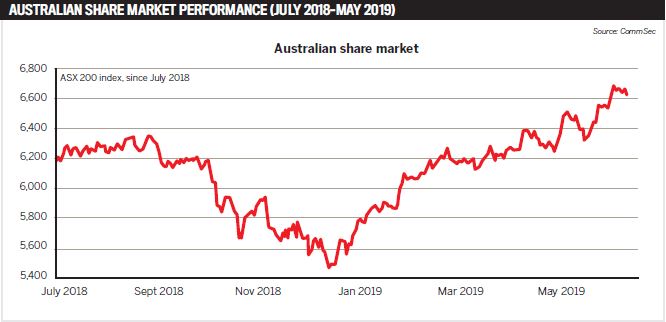

The bartender is concerned. According to data published by CommSec at the end of the last financial year, stock market investors saw a rally of 11.4% on their average ROI in the 2018/19 financial year. Meanwhile, property investors saw a decline of 3.6% on their ROI. It’s a notable development in a country where the tax office counts two million property investors.

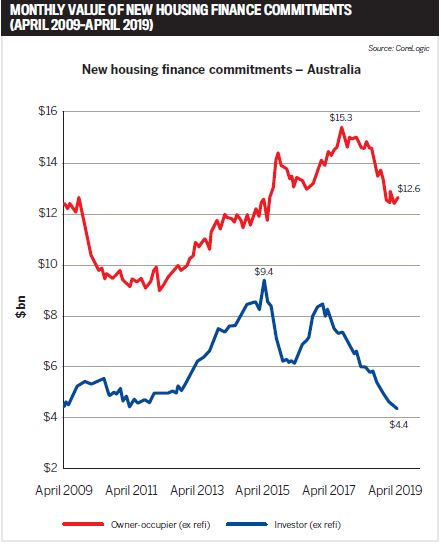

Further, June data from CoreLogic shows that while both owner-occupier and investor lending has slowed, investor credit is now limping along at a historically low growth rate of 0.7%.

It’s the latest in a string of blows for property investment, and the bartender is unsure how to act, or who to turn to for guidance.

“There are exceptions, but generally speaking an accountant tends to be reporting on what has happened in the past, so they aren’t necessarily looking to the future and what could happen. If they did look ahead, they would tend to be risk averse,” says Jai Martinkovits, MD of Finance Ferret.

“If you look at the financial planner, they’re certainly forward looking but are debt averse and will look at ways to reduce existing debt. However, mortgage brokers are in the debt and risk game, so it’s a very relevant conversation for brokers to be having.”

The investor property market has been rocked several times in recent years. From property prices and credit policy to APRA’s lending caps, CoreLogic has found property investors are under such pressure that activity has plunged from a high of 43% of all purchases to just 28%. When announcing that the RBA would cut rates for the second consecutive month in July, Philip Lowe said, “Demand for credit by investors continues to be subdued, and credit conditions … remain tight. Mortgage rates are at record lows and there is strong competition for borrowers of high credit quality.”

The million-dollar question is whether the latest hit to ROI is an anomaly, or the start of a new trend. There is evidence to support both sides.

Last year Aussie Home Loans published its 25 Years of Housing Trends report, which concluded that since 1993 property values had increased 412%, while the ASX All Ordinaries index had gained a mere 261%.

However, these figures were sourced before the lynchpin property markets of Sydney and Melbourne faced their worst value slide in recent history – a development that reframes everything.

This year’s federal election has yet to spark the trickle-down effect predicted by so many, but there are high hopes following two cash rate cuts and APRA’s relaxation of servicing rules.

“To really stimulate the property market, you have to get gun-shy investors to feel more confident again,” says Helen Collier-Kogtevs, MD of Real Wealth Australia.

“The way that is going to happen is a stable economy, low interest rates and banks lending freely again. Then people will feel they can borrow, they can afford the property and they will want to invest for their future.”

The wider view

That added economic strength could be just around the corner. Regulators and lenders have made a series of moves that have had the effect of stimulating or dampening the market at various points over recent years. However, the removal of the investor lending benchmark in April of last year didn’t reinvigorate this specific area of the property market as expected.

“While we have not seen a material lift in demand in the investor space since the removal of the benchmark, APRA’s subsequent change to the serviceability floor could bolster borrower sentiment, in turn stimulating investor appetite for property,” says Mortgage Choice CEO Susan Mitchell.

“Furthermore, APRAs serviceability floor [changes] may help to improve access to credit and enable some borrowers to obtain a larger loan, which may benefit property investors.”

Ironically, the strength of the ASX over the last 12 months could see a return of the sentiment that drives positive economic growth and therefore stronger conditions for lending and property purchase.

CEO and founder of Blue Wealth Property Tony Hayek says, “The upside of the share market performing well is that it gives everybody confidence. It reflects a strong economy, it drives positive sentiment, it means people will be positive about investment. All of that reflects on positive economic numbers, and that gives people confidence to invest.”

For Hayek, like others, the real issue is the availability of credit.

“Even though there has been much talk about giving some relief to the finance market and industry, that hasn’t yet translated into reality. What we have seen at Blue Wealth is that sentiment has significantly improved, but that hasn’t led to improved activity yet,” he says.

What is certain is that there has been a clear change in the economic returns that underpin not only the ‘Australian dream’ but the retirement aspirations of millions, as well as the stability of the wider economy. If these trends continue in the new financial year, it could signal a sea change in how Australians generate wealth, as well as the focus of thousands of broker businesses.

Mint Equity director Zac Peteh believes there are numerous reasons to be positive.

“We may see the property purchase price bracket drop [and that will] allow investors to have both shares and property. With property prices falling, now is the time to buy and benefit from future years’ capital growth. For most, property investment is a long-term strategy, so capital growth over a 10- to 20-year period, combined with good yields, is still likely to outdo share returns for the same time frame,” Peteh says.

.JPG)

Safe as houses

As Martinkovits highlights, brokers have a unique role to play as they work in both risk and debt. From this vantage point they can even leverage the uncertainty that exists in the property market currently to support their investor clients – as well as their own business diversification strategy.

“What brokers should be doing is having conversations to educate their clients, particularly around the power of leverage. Any broker who isn’t doing that is missing a huge opportunity and, beyond the opportunity itself, they are doing their client a huge disservice.”

For Martinkovits there is a simple formula – and it all comes back to capital growth. Imagine a client has $100,000 to invest. One option is to buy shares, either for $100,000 or for up to $200,000 by obtaining a margin loan to boost their capital dollar for dollar. Another option is to use the $100,000 for a deposit and buy an investment property for $500,000.

Apply a conservative return to both options and, over time, property leads while attracting less risk – even if that performance is at a slightly lower rate than that seen over the last decade.

“Brokers really need to be able to help clients, without getting into the financial planning area – there is a fine line there. The opportunity is to have a broad conversation around the shape of retirement and how property can support people in achieving their objectives,” Martinkovits says.

“Brokers really need to be able to help clients, without getting into the financial planning area – there is a fine line there. The opportunity is to have a broad conversation around the shape of retirement and how property can support people in achieving their objectives,” Martinkovits says.

The possibilities don’t end there. In addition to guiding new investor clients through the opportunities in the market, brokers can assist many existing investors who also require loan restructuring.

“There are two streams of opportunity for brokers who are savvy enough: one is to switch the investor from their interest-only loan to a P&I repayment structure that is affordable and manageable. The second is to structure the finance so that the investor can go on and obtain another property,” Collier-Kogtevs advises.

“I think it’s important that investors who think they can’t borrow keep trying. Don’t take a no now as a no forever.”

In the current environment, the bottom line is that investors prefer the tangible asset over the intangible and for that reason will often favour property over stock, or combine the two for a long-term strategy if their situation allows.

For those who still can’t decide, it could be that compromise provides the key. The share market is volatile and exposed to shocks from across the globe; however, shares in property and development firms saw a 12% total return last financial year.

Either way, from the broker’s view, the new figures are further evidence that diversifying from owner-occupier residential lending is a priority.

“I don’t necessarily think that property will perform as strongly as it has in the past, but you don’t need that same level of performance for it to be a very solid asset class. Property should be a core part of every Australian’s investment strategy,” Martinkovits says.