Last year, as executives from the major banks answered to the royal commission, their non-bank competitors quietly issued 60% of all new mortgages. Now, with their sights set on regaining lost ground, the majors are back in business with new tools, touch points and tech – but is it enough to win back the third-party channel?

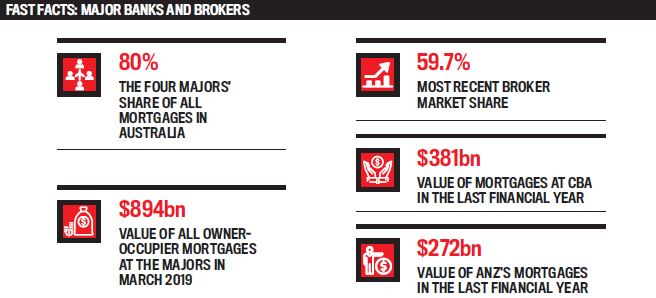

The major banks hold around 80% of Australia’s mortgage market, and brokers now drive 59.7% of residential loans across all lenders. So, when a royal commission was called to investigate misconduct in the industry, few expected the relationship between the two to sour as quickly as it did.

However, by mid-2018, the revelations from AMP and the departure of senior executives from across finance paled in comparison to the standoff occurring between banks and brokers.

Then borrowers started to vote with their feet, too. Whether correlation or coincidence, S&P found that non-bank lenders issued 60% of all new home loans in 2018. Although knee-jerk changes to lending policies across the majors handed a free kick to the non-banks, that number tells a story.

Now, five months and a federal election since the release of the commission’s final report, the majors are moving on – and asking brokers to move with them.

“The commission was an incredibly important examination, far more important – and necessary – than we originally thought. We have learnt, and are continuing to learn, a lot about ourselves, the industry, community expectations and where we must do better to deliver fair and responsible banking,” says Simone Tilley, head of national broker distribution for ANZ.

ANZ has been part of the broker industry for almost 30 years, and in the last financial year, its mortgage portfolio reached $272bn, 55% of which was broker-originated. During commission hearings, ANZ chief executive Shayne Elliott warned that a fee-based remuneration structure would turn broking into a “privilege for the wealthy”.

“Brokers play a vital role in helping our customers navigate what can be a stressful and complex process and are integral to promoting competition and choice within the industry,” Tilley says.

Her comments are echoed by Adam Croucher, who was promoted to GM for third-party banking at CBA in January of this year.

“Building a strong and sustainable third-party channel has always been a key pillar of CBA’s home-buying strategy, and that remains unchanged,” Croucher says.

“We remain completely committed to the mortgage broking channel and continue to invest heavily to support brokers. We note the recent discussions about broker remuneration structures and will continue to engage with all of our stakeholders in these discussions.”

CBA’s mortgage portfolio reached $381bn in value for the last financial year, 40% of which was originated through brokers.

New regulation

While remuneration may be safe for now, other changes are being implemented to regulate the broker channel and the wider lending space. For example, the best interest duty proposed by Hayne is a measure that has inspired both positivity and caution across the industry. While some employ a cavalier attitude, welcoming the chance to prove the difference brokers can make, others remain cautious of how such a duty will be defined and imposed.

As participants of the Combined Industry Forum (CIF), both CBA and ANZ have been across these changes for some time. Tilley serves as the chair of CIF’s governance, data and reporting stream, and she says it’s important any changes are phased and based on consultation from multiple groups.

“We support a new broker best interest duty. However, any changes need to take place over time and involve careful consultation with all affected groups,” she says.

“We do need to help the industry evolve to ensure its customers are served in a transparent, fair and responsible manner. In addition, any changes need to be decided by collaboration between industry and governments to ensure the outcomes are right for customers, brokers and the wider community.”

For CBA, the main area of regulatory focus at this point is living expenses. To support brokers, the bank has introduced a monthly living expenses calculation template, available through its website. The template is an editable PDF, which can be downloaded and emailed or printed.

“As an advocate of the broker channel, it is important for us to know that the brokers we deal with understand their regulatory obligations, as well as CBA’s policies, systems and processes,” Croucher says.

“It is for this reason that we continue to work closely with our brokers to understand what tools they may need in order to deliver good customer outcomes.”

Focused on the future

All four major banks face significant remediation bills and ongoing work to restructure their businesses. However, their loan books continue to grow, even if their market share has stuttered at times.

APRA’s banking statistics for March 2019 – the first full-month figures following the commission’s final report – showed that the majors loaned nearly $894bn in owner-occupier mortgages, up from the February figure of just over $890bn. CBA posted the highest value of owner-occupier loans, followed by Westpac, ANZ and NAB.

For investor mortgages, the majors loaned $469bn over March, compared to the previous month’s $470bn. In this category, Westpac posted the highest total value, followed by CBA, NAB and ANZ.

However, just as the non-banks saw gains in 2018, the non-majors have also started to encroach on the big four’s market share. In March of this year, the owner-occupier loan book at the top 10 non-majors totalled $183bn, about $1.5bn more than the February 2019 figures.

Yet overall lending remains down, and brokers report that they’re struggling to meet client expectations amidst ongoing product and policy changes. Both ANZ and CBA have made a series of commitments to reconnect with brokers through both technology and processes, and both banks are looking to innovate their broker touchpoints.

CBA has recruited 60 new staff to its assessment team, allowing the bank to provide what Croucher describes as “an enhanced, consistent service offering for our brokers and their customers”.

The bank has also invested in its Broker Support Hub, which provides brokers with “expert advice and answers” over the phone and in March, CBA launched the CommBank Loan Tracking software platform. Based on broker feedback, the platform provides brokers with real-time updates.

“We recognise our mortgage broking partners are a key channel for customers who are looking to purchase a home. We have supported the broker channel for more than 20 years and will continue to support the channel through ongoing investment,” Croucher says.

Meanwhile, at ANZ, the focus is on data-led, timely and relevant education for both brokers and aggregators, based on feedback from BDMs.

“In 2018, we trialled partnered podcasts with aggregators and, not surprisingly, found that we got the best response from broker-led content,” Tilley says.

“We will continue to look for opportunities to partner with the broader industry in education over the course of 2019 and beyond.”

Although NAB declined to answer direct questions, the bank’s most recent financial results directly credit brokers for boosting business in the last reporting period. Compared to September 2018, the bank’s mortgage lending increased $6.8bn, which NAB attributed to growth in the broker channel and strong results in New Zealand.

Meanwhile, NAB’s business lending increased 5.3% year-on-year, following the launch of NAB QuickBiz for Broker in May 2018. The digital platform enables brokers to apply on behalf of their small business clients for unsecured business finance of up to $100,000.

The bottom line

The royal commission’s recommendations threatened the existence of thousands of broker businesses, but now the wider impact threatens the foundations of the Australian dream of property ownership.

Lending policy changes have had a far-reaching economic impact, and property values remain dampened, despite the efforts of APRA and several false starts in terms of recovery.

Pre-election auction activity came to a near halt; clearance rates were down more than 10% year-on-year at the start of May. In the March quarter, home-buying activity reached a 17-year low in Sydney, and arrears are on the rise elsewhere in the country, particularly in WA and Queensland.

APRA figures released in late June show that housing loans with customer-owned banks increased by 8% over the last 12 months, while the major banks grew by just 2.6%.

However, there is hope on the horizon for the market. The RBA has reduced the cash rate twice since June, and APRA has finalised its serviceability changes, meaning that all ADIs can now review and set their own minimum interest rate floor and use a revised interest rate buffer of at least 2.5% over the loan’s interest rate.

While it’s clear banks and brokers cannot thrive without each other, the most difficult lesson from this experience is that Australia cannot thrive without credit. If the last 15 months have demonstrated anything, it’s the value in a certain African proverb: “When elephants fight, the grass is hit the hardest.”