By

On 1 July, Australia entered anew era with the launch of the first phase of open banking, which allows personal banking customers to share certain data with trusted third parties.

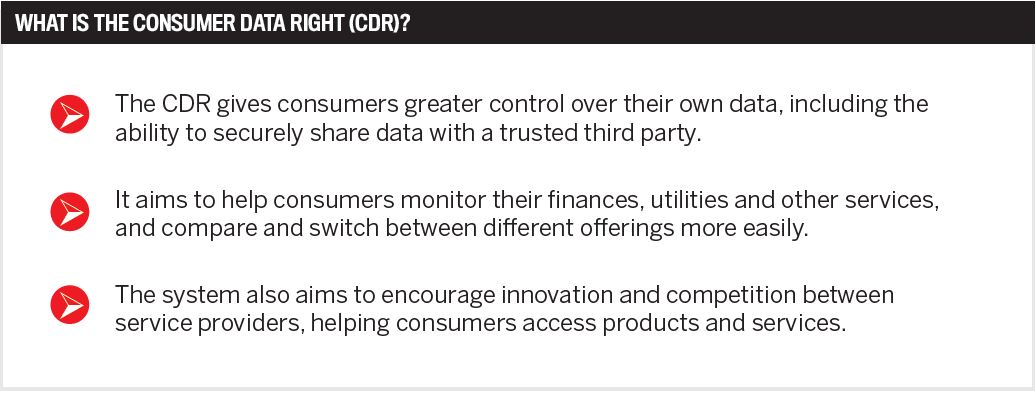

The Consumer Data Right regime, also known as open banking, is intended to give consumers and small businesses greater control over their personal information by allowing banks and fintechs to provide safe and secure access to their data to trusted third parties.

With this capability, Australians will be able to make better decisions regarding the products and services they purchase, and can switch between providers more easily. The transition to the new system will challenge existing providers to better look after their customers and will create room for new competitors to enter the market.

The ACCC had earlier launched a platform that enables banks and fintechs to apply to become accredited data recipients in order to be able to fully engage in the open banking environment.

Sarah Court, commissioner, ACCC

Sarah Court, commissioner, ACCC

“The launch of this Consumer Data Right (CDR) platform and portal means businesses of all sizes can take the first steps towards being part of this crucial economic reform,” said ACCC commissioner Sarah Court.

“This sharing of data is a watershed moment for competition in the banking industry and, in time, will enable every Australian to use their data for their own benefit” Anna Bligh, CEO, Australian Banking Association

“We are encouraging businesses wanting to participate in the CDR regime to apply for accreditation and take part in reshaping banking competition in Australia.”

The platform, launched at the end of May, not only provides a portal where businesses can apply to be accredited but is also crucial to ensuring that consumers’ data is shared exclusively and securely between parties that have been vetted by the ACCC.

Anna Bligh, CEO, Australian Banking Association

Anna Bligh, CEO, Australian Banking Association

Although the CDR system was introduced on 1 July, Anna Bligh, CEO of the Australian Banking Association, said it would start small but ramp up over time.

By the end of 2020, the ACCC anticipates that there will be dozens of companies accredited to help customers get a better deal – and the more accredited companies there are, the greater the competition battling it out for Australian customers who are searching for the best deal, Bligh said.

“This sharing of data is a watershed moment for competition in the banking industry and, in time, will enable every Australian to use their data for their own benefit,” Bligh said.

“Customers can be assured that they will always be in control of how and when they share their data. This is a great achievement by the major banks. Despite moving the majority of their workforce to work from home and processing unprecedented numbers of customer queries and loan deferrals as a result of COVID-19, the banks have stayed on plan and delivered open banking and ensured the data will start to be shared from today.”

Sydney-based purpose-fintech Frollo is one of only two companies that have so far been approved to access the data from the new CDR system as it goes live. With first access, Frollo is in a position to help traditional banks, neobanks, fintechs, lenders and employers get ahead of the competition with its B2B and open banking solutions.

The financial management company, which currently has over 100,000 users on its financial wellbeing and budgeting app for consumers, is the only fintech that’s an accredited data recipient (ADR) under CDR rules after it participated in the open banking trial and helped build and test the infrastructure alongside the big four banks.

Gareth Gumbley, CEO and founder, Frollo

Gareth Gumbley, CEO and founder, Frollo

Gareth Gumbley, CEO and founder of Frollo, said that after investing in getting accredited, the next step for organisations would be pulling the data and understanding how they could compete with it.

“Now that the Consumer Data Right is live, the next step for everybody is how to leverage the data for a competitive advantage. Given our experience of testing alongside the banks, we’re in a position to educate and guide other businesses looking to comply, compete, innovate and leverage the opportunities available under the system,” said Gumbley.

“Once these organisations become new ADRs, we’re also in a unique position to help them actually collect the CDR data through our SaaS technology solutions. We’re currently one of the only organisations to have technology built specifically for open banking in Australia, which makes it incredibly valuable for new ADRs who don’t have the resources to invest in their own solutions.”

Gumbley added that open banking had triggered a massive shift in the way organisations think about consumer data, which would benefit Australians.

“The Consumer Data Right system gives organisations the ability to be faster, more transparent and more secure. We’re moving into a world where we can give users a real-time view of their money and will soon be able to confidently move them to the best products available with a couple of clicks,” Gumbley said.

The four major banks have confirmed their commitment to the initiative, with Westpac announcing that eligible customers of the bank are now able to share their credit and debit card data, as well as deposit and transaction account data, with accredited third parties.

Westpac acting chief executive, consumer, Richard Burton said Westpac was proud to be able to switch on open banking for customers.

“This marks an important milestone for open banking, with customers now having the ability to share their data. Westpac supports enhanced data sharing in banking as it will help drive competition and customer choice,” Burton said.

“We have been working hard throughout the entire process to ensure the system is robust and secure for customers. Enhanced data sharing will give customers more confidence they are getting the best deal, and help make it easier to find the best-value service that meets their needs.”

Lenders and banks have invested significant resources in getting open banking ready. Rachel Slade, group executive, personal banking at NAB, confirmed the bank had “invested heavily in our technology foundations and in our people” to build a customer experience that focuses on ensuring the safety and security of customer information.

“A competitive and innovative financial services industry is critical to ensuring great customer outcomes and the growth of the economy more broadly, with opportunities for further innovation and new business models to be established,” Slade said.

“It will take time for customers to develop familiarity, trust and understanding in using open banking. We’re continuing to prepare for future phases that will allow our customers to share more of their data, should they choose to do so, and we will continue to invest in the open banking regime as future phases are developed, while ensuring that speed is not prioritised over safety. This is critical to building confidence in the system.”

Angus Sullivan, group executive of retail banking services, CBA

Angus Sullivan, group executive of retail banking services, CBA

Angus Sullivan, CBA’s group executive of retail banking services, added that with cyber security becoming a growing, significant issue, the constant threat of online fraud underpins the need for consumers, organisations and government to take data and account security seriously. CBA is “continuing to invest more than $5bn in technology in the next five years” to fight this battle, he added.

While just the four major banks will be part of the system initially, other banks are scheduled to join within the next 12 months.