By

Property buyers looking to secure a home during the housing market slowdown are being urged to carefully consider their employment status before they sign on the dotted line.

Banks and lenders have always had a policy of checking employment status at any stage during a loan application. However, historically, after confirming employment status and income to satisfy the finance clause, they would not have typically checked a second time after the finance clause had passed.

But this is becoming standard practice, and there is now a higher risk that previously approved loans could be withdrawn as late as on the day of settlement.

“Most, if not all, lenders will be doing rigorous checks on all applications, even if the application was previously approved, and there will be a number of people in a world of pain if they have already exchanged [contracts] and now have issues with employment,” says Raj Ladher, home loan specialist at Your Mortgage Broker.

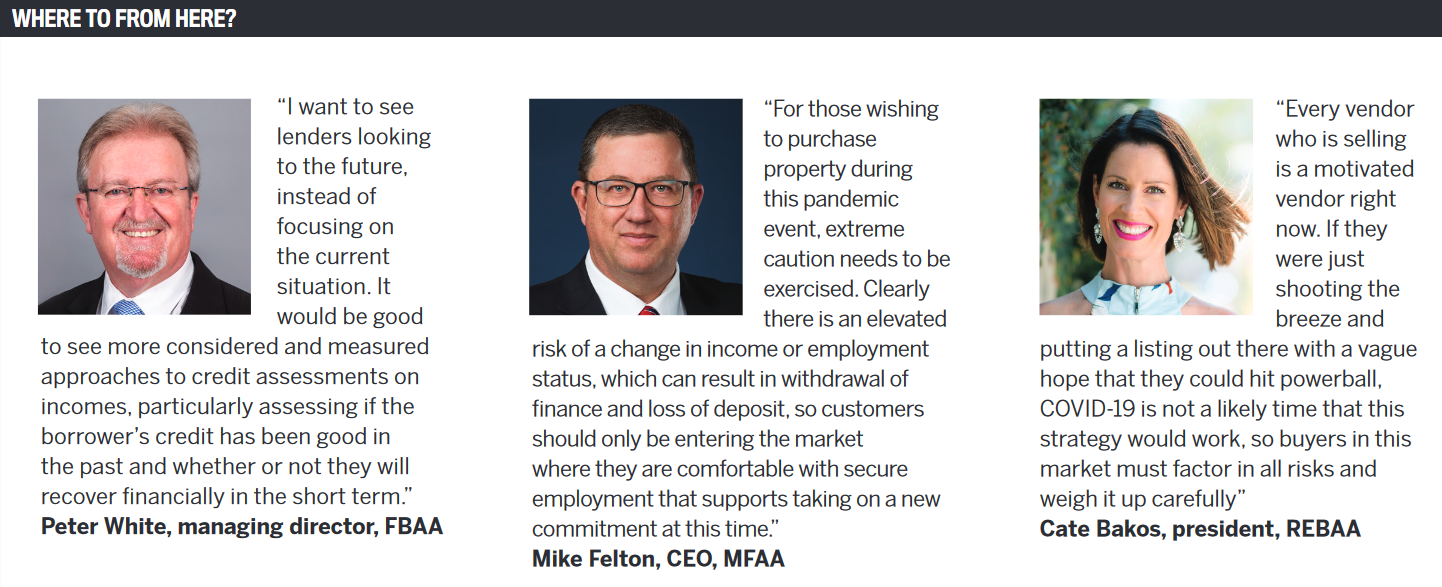

“Most, if not all, lenders will be doing rigorous checks on all applications, even if the application was previously approved” Raj Ladher, home loan specialist, Your Mortgage Broker

“I would imagine banks’ credit teams will be extremely cautious with some industries, such as hospitality, airline, tourism and retail (non-grocery).”

This puts some buyers at risk of losing their deposit if they are unable to settle the loan.

Mike Felton, CEO of the MFAA, confirms that even those borrowers who have an unconditional finance approval could be at risk.

“There are certainly risks where the customer has an enforceable contract to purchase and they experience a material change in circumstances before settlement occurs. Where the customer has unconditional finance approval, most lender contracts have clauses that allow the lender to withdraw if there has been a material change in circumstances between unconditional approval and settlement,” Felton says.

“When COVID-19 first appeared there were a number of deals in the pipeline, and whilst the lenders have not been obliged to settle these, it is the MFAA’s view that this is just another form of COVID-19-related hardship and should ideally be approached by lenders by having a conversation with the customer as to what is in the customer’s best interests.”

The process of rechecking employment status as late as on the day of settlement may not have been standard practice; however, FBAA managing director Peter White points out that when markets are impacted by abnormalities, such as the GFC or COVID-19, increased credit investigations always rise to the forefront of attention.

“Over the decades, lenders have regularly checked the employment status of borrowers post the finance clause if they knew or felt they needed to. I’ve seen and experienced this over the 42 years I have been in this industry, through the many recessions we’ve had, since the 1980s and through the GFC in 2008,” he says.

“In today’s COVID-19 period it is very obvious that some employment markets have suffered far more than others. This means people’s future employment and their incomes are in question, so this is a normal and prudent credit risk profiling measure.”

For borrowers who find themselves in this situation, White says brokers are “undoubtedly the most suited to assist [them]” in the current environment.

“There are always solutions available to some degree, but this is highly subjective to the person or business’s specific needs. Borrowers need to seek tailored guidance to help them navigate through this time,” White says.

“Real estate agents and their respective associations need to be cognisant of the current environment. They need to be flexible and understanding that things are not the norm, and work together for the desired outcomes.”

Cate Bakos, president of the Real Estate Buyers Agents Association of Australia (REBAA), agrees, saying this economic shift has the potential to impact a huge number of potential property buyers.

“We are taking the approach that any client who has concerns about their job security needs to carefully consider whether now is the right time for them to be purchasing a property. Examples include employment risk, limited ‘Plan B’ risk, such as if they have tight borrowings, or single-lender eligibility, or no buffer funds,” Bakos says.

“Any client who has concerns about their job security needs to carefully consider whether now is the right time to be purchasing a property” Cate Bakos, president, Real Estate Buyers Agents Association of Australia

At the same time, she believes that in the current market it’s an ideal time to buy for those who have a deposit and a solid income. If every potential buyer decided to sit on the sidelines and heed the careful, protective advice that encourages them not to buy in this market, Bakos says low-risk applicants would pass up a great opportunity to get into a market that is much easier to buy in than in recent times.

“Brokers should offer helpful, pragmatic advice. The buying conditions are softer and more opportunistic for their clients, so if the clients can move forward with a low-risk purchase, they should be encouraged,” Bakos says.

“Brokers need to help buyers weigh up the risk, the reward, the mitigants and the Plan B (and C, if they can). And they should call out the risk-takers and remind them of the magnitude and likelihood of the risk, if they have genuine concerns about a cavalier purchaser.”

From this point onwards, all applications being approved “should be fairly safe”, Ladher adds, as the majority of job losses flowing through as a result of the pandemic have already occurred.

“These loan applications will be assessed with the impacts of COVID-19 already factored in; however, as it’s an ever-changing beast, purchasers need to have contingencies such as cooling-off periods and get-out clauses. More than ever, potential borrowers need a mortgage professional to help them through the mortgage maze,” he says.