By

Award-winning finance broker and real estate agent Chris Brown is the founder and managing director of Sydney brokerage. He helped a young self-employed couple who had been rejected for a property loan by two lenders.

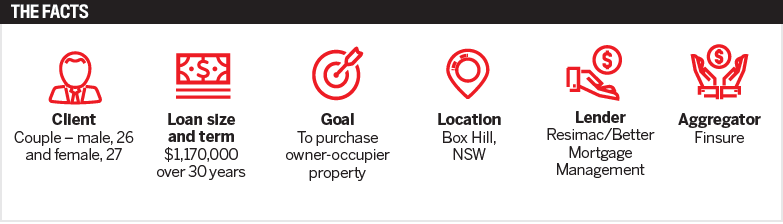

I was approached in late March 2021 by a husband and wife who were selling their existing owner-occupied property and buying a new property that they had paid a deposit for in Box Hill, Sydney.

The clients were very stressed and had been referred to me by a past client who we had assisted with a similar scenario. The clients were self-employed in the building/construction industry and had been in business for the last four years.

Despite COVID, the business had continued to grow, and they had made large investments in staff and equipment. The clients approached their current bank (where their home loan and personal and business accounts are held) but after two weeks of waiting were declined due to servicing. They approached another lender, which declined them due to servicing. By this stage the clients were very upset and concerned they would lose their deposit.

I met with the clients on a Sunday night, and the wife was crying due to the stress. They had sold their current property, put a deposit on a new one, and had no loan. We completed a fact-find and reviewed their scenario, along with all supporting documents, including a few years’ personal and company financials and their current YTD financials. It was clear that a mainstream lender would not have been able to assist the clients as in the first couple of years, like most new businesses, they had run at a loss, so were carrying over losses, not to mention the significant investments they had made in the business in FY20. With the funds from the sale of their current property, along with their savings, the LVR was just under 70%, including stamp duty.

We approached our BDM at Better Mortgage Management (BMM) and discussed the deal in detail. The YTD turnover and profit for the business for FY21 was fantastic, and after speaking with the client and their accountant we were confident servicing would not be an issue with Resimac. The accountant was as frustrated as the clients about the restrictions placed on self-employed borrowers when, in his words, “they can afford this more comfortably than most PAYG clients I see”.

We spoke with the clients and the accountant about the solution, and both were extremely happy with the option we had secured. We prepared the required documentation for the loan and submitted it to Resimac, securing the clients an amazing rate due to the low LVR, while only requiring a self-declaration and accountant’s declaration to confirm the income. The solution from Resimac allowed us to use a range of alternative methods to support income. For example, we could have chosen to use BAS or bank statements instead of the accountant’s declaration.

The valuation was ordered, and the property came back at contract price; the loan was assessed with only one small question raised by the assessor. The loan was approved, and the solution allowed the clients to commit to the new purchase, securing their new family home. The teams at BMM and Resimac were fantastic, and the clients were absolutely ecstatic at the result.

No one client is the same; you need to complete a detailed fact-find, review all documentation, and understand lender policies to ensure you find the right solution.

Unfortunately, self-employed clients can struggle with mainstream lenders due to the servicing requirements, and although self-employed clients think they make a lot of ‘profit’, once financials are completed it does not always work out on paper.

Accountants are great at reducing tax payable, but this does not always translate into financials that will support a loan, especially with a mainstream lender.

We work with clients to find a solution, and thankfully the industry has some amazing lenders who understand the requirements and challenges self-employed clients face, and can provide alternative options.

Had the clients used a broker in the first place, they would have saved a significant amount of stress and time, not to mention the added enquiries on their credit fi les. For anyone doing self-employed loans for clients, be prepared to look outside the box. If the scenario won’t work with a mainstream lender, do some research. There are other solutions for your clients, and in my experience these are very good long-term clients who continue to grow and refer a lot of new business.