By

Gordon MacVicar runs the Mortgage Choice Peregian Beach brokerage on Queensland’s Sunshine Coast. He assisted a couple who wanted to buy an investment property but had been told by their bank that their loan application was outside policy.

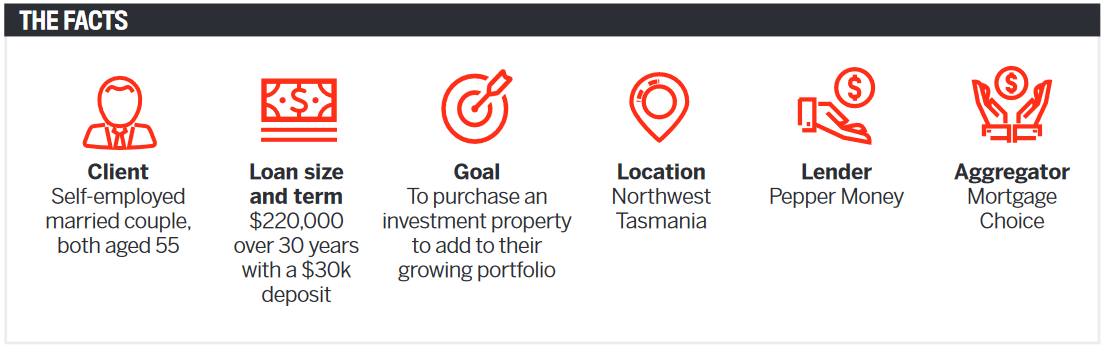

I recently helped a married couple, both self-employed, who own a medical equipment business in Queensland.

They wanted to purchase another investment property in their favoured location in the northwest region of Tasmania. Demand for rental properties in this area has increased strongly in 2021, and the region is seeing some of the best rental yields in Tasmania at the moment. My clients wanted to take advantage of this trend as part of their long-term wealth-building strategy.

Thinking it might be more convenient and simpler, the couple approached their existing big four bank for finance, but they were then made to jump through hoops for several months without success. At the eleventh hour, and after three finance extensions, the bank told them their loan application was outside policy.

In desperation, at 3pm on the day of the last finance extension the bank had offered them, the couple called me to see if I could help them get a loan for their desired investment property purchase.

I had assisted this couple in the past with another loan for their business and, knowing their employment circumstances, I knew that they needed an alt-doc loan.

As the clients were self-employed borrowers who had been in business for a couple of years, I asked them to supply a couple of forms of evidence so they could prove their income and satisfy Pepper Money’s credit assessment criteria. This included their ABN registration details, their GST registration, and six months’ worth of business activity statements. I also worked with their accountant to get a signed declaration of their financial position. Luckily I already had some of this information to hand, which sped things up significantly.

Using all this information, we were able to rely on more recent income verification documents to prove my clients’ current and sustainable income levels for loan serviceability. This was a more accurate reflection of their income as opposed to averaging their business financials across the last two financial years.

Looking at their most recent financials, I could see the couple’s business was in a strong position, having weathered the COVID-19 pandemic, and that their income from their medical equipment business was up considerably since an understandable drop in 2020.

Recognising that they needed a fast turnaround time on the loan and knowing Pepper Money could deliver on that, given its reputation and ability to offer fast service level agreements, the couple chose Pepper Money on my recommendation.

I quickly reached out to my Pepper Money BDM, Stefan Heather, who to the couple’s delight got straight onto the transaction for them. He was able to get my clients conditional approval in two days, and the entire deal was sorted out in seven days, allowing them to make an immediate offer on their chosen property.

When I gave them the good news that Pepper Money had approved the loan, the wife started crying in genuine relief. They had become so frustrated by the long, drawn-out process and feared they would miss out on the property purchase if it was delayed any further.

What lessons were learnt from this situation? Judging by this couple’s experience, it is clear that banks are making it harder for Australians to get a loan – even if they already have an existing banking relationship.

Having tried to go it alone, my customers came to realise the valuable role a good mortgage broker could play in getting the outcome they needed. They really appreciated how quickly I was able to come up with a solution when they thought all was lost.

So, how would I approach these types of deals in the future?

I’m quite comfortable writing and recommending alt-doc loans as I’ve helped quite a few self-employed customers in the past.

It is clear there is a growing appetite for self-employed customers wanting to get into the home loan market, and my customers’ experience has highlighted to me how rewarding it can be to be able to off er outside-the-box solutions for this particular customer segment.

I am already having active discussions now with some of my existing self-employed customers who may have previously thought they had to wait a lot longer before they could realise their financial goals. Customers should always be aware of the options available to them through non-bank lender alternatives.