By

Graeme Salt is director of The Futurus Group, which includes Origin Finance, Chan & Naylor Finance and Walker and Miller Training. Brokerage Origin Finance helped a couple who had moved their business from London back to Sydney and wanted to buy a property.

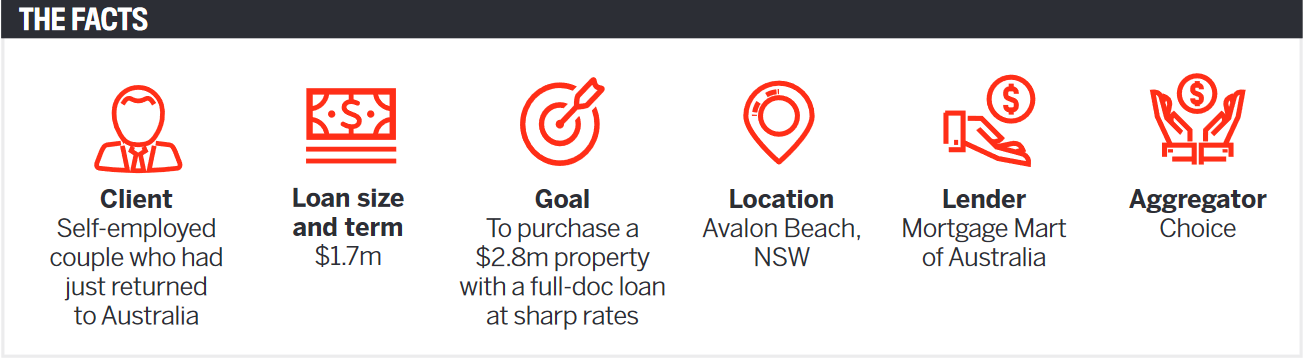

Origin Finance recently arranged a full-doc loan for a $2.8m purchase by clients who had only just returned to Australia and set up their new business. We wanted to ensure they got a good rate, rather than having to pay an expat rate.

This sounds like an impossible task, but a collaborative approach between Origin Finance and the clients, and an open-minded lender, made this a fairly straightforward deal.

The clients had noticed that in 2020 property prices were starting to take off. They had previously contacted another broker, from whom they never heard back – presumably because the scenario was too complicated.The clients were referred to us in November 2020. An initial consultation indicated that, to make this deal fly, we had to prove continuity of business income from their London to Sydney operations.

We workshopped the scenario with a few funders, and Mortgage Mart proved the most receptive. An initial briefing with a Mortgage Mart BDM also meant the funder would be receptive to the loan application.

We spoke to the clients in November 2020, and they moved into their home in May 2021. In between, we had to demonstrate that, although they had just returned to Sydney, their business was essentially the same as it was in London.

Our clients are business coaches, and their clients are often executives from blue-chip organisations all over the world. In 2020, they moved their business to Zoom and then realised they could still serve their clients from Sydney’s Northern Beaches rather than London’s grey. For Origin Finance, the trick was to demonstrate to a lender that the clients’ business was essentially the same, except that it was now a new Pty Ltd invoicing in Australian dollars, rather than a PLC invoicing in British pounds.

A meeting with the clients soon had us all on the same page. We needed to get UK financial statements and references from their clients confirming that they would still use the business’s services. We even submitted as evidence an article the clients had written in a quality Fleet Street newspaper on why they were returning to Australia and how their business could still be successful.

It took us a while to assemble the application for Mortgage Mart. It helped that the LVR was low, but we had to demonstrate that these were top-drawer clients. We provided:

»one BAS statement

»bank details

»MYOB statements

Pre-approval was arranged in February 2021, and the clients moved into their new home in May.

Mortgage Mart’s interest rates are good, maybe slightly higher than if the clients had gone with a bank lender. But that would have meant waiting for two years to get finance, and by then property would have been a few hundred thousand dollars more expensive.

The clients were ‘quids in’ with Mortgage Mart and happy in their home.

This was a deal that made sense, combined with strong servicing and a low LVR.

Most mortgage managers have the ability to look through standard policy to manage risk and approve sensible deals. Mortgage Mart proved this in spades: whoever heard of a full-doc loan with one BAS?

By working with the mortgage manager and the clients, we built up such a powerful application that the funder was keen for the business. This deal also proved stronger in a COVID world; we have all learnt to make our businesses run from home.

In our initial briefing to Mortgage Mart, we said of the clients: “They manage the same clients via Zoom, etc. In essence, nothing has changed except that they are now invoicing in dollars rather than pounds.” In a COVID world, our clients are offering the same service, whether in Sydney or London.

The other takeaway is to never stop talking to the universe. The clients were referred to me by an old swimming buddy who I now only interact with on Facebook. The clients have since referred other people to Origin Finance.