By

Nathaniel Truong is the director of The Loan Lounge brokerage in Sydney. By delving into the detail of his client’s financial position, he helped structure a home loan for a woman in her late 50s who thought the dream of homeownership could never become a reality because of her age.

The Loan Lounge had recently assisted a client with refinancing a home loan to a lower and more competitive rate. After completing this transaction, the client had a conversation with her sister about buying her first home. The sister believed the client could never own her own home due to her age. However, she suggested she speak to someone at The Loan Lounge and give it a go.

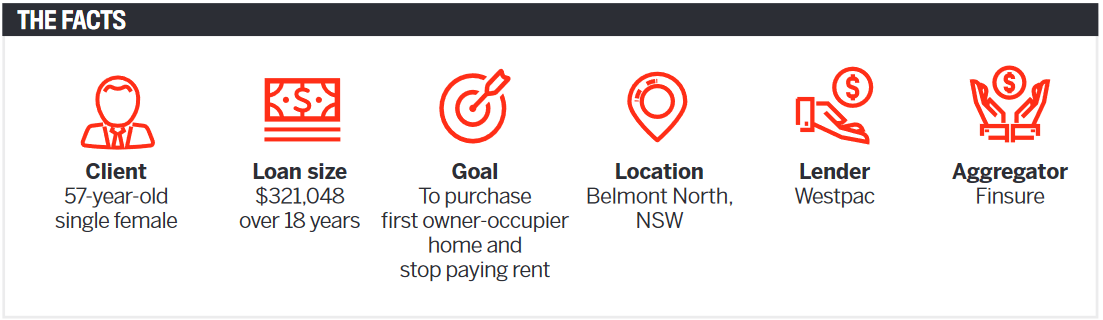

The client approached us and asked whether she was eligible to obtain a loan. She was 57 and working three jobs (one full-time job and two casual jobs) as a registered nurse. Her children had all grown up and moved out of home, and she was waiting for a payment related to her leave entitlements from a full-time role she had finished up. She had been working for this employer for over 26 years.

At the time, the client did not have the required three months of genuine savings to support a loan application, so we put together a strategy that would set her up to obtain a loan and purchase her first property over the following four to five months.

Over the next few months, we worked with the client to address two main concerns the lender would have: her genuine savings and an exit strategy.

The initial concern was easy to meet as we worked with the client from October to January to help her save up the necessary 5% deposit over a three-month period to show genuine savings.

We tackled the second concern by undertaking a detailed fact-find on the client’s income, expenses, assets and liabilities, with a special emphasis on her exit strategy. We asked about her health and her parents’ wellbeing – they were still alive and currently 86 years old. Her grandparents had five children who were still alive, and she expected to receive a small inheritance. We added this to the notes to the lender.

We spoke to the client about her retirement plans and when she wanted to stop working and retire. Most clients say they’ll continue to work indefinitely; however, the realistic retirement age in her role was 75 years old, which meant she had 18 years left to work.

We found out she had $180,000 in superannuation, which meant that she still had 18 years of superannuation contributions and earnings. We then used an online superannuation model to work out what her superannuation balance would be in 18 years, and this amount came to $286,000. (We used a conservative figure assuming 9.5% of superannuation contributions, which showed that she would accumulate an additional $106,000, and we did not add any investment returns.)

We proposed a loan term of 18 years. The client would pay down the loan over that period and have access to superannuation funds of $286,000 and $80,000 through an inheritance at retirement age. This was a clear and coherent exit strategy.

By providing clear notes around the exit strategy and meeting all the bank’s concerns, we were able to help the client purchase her first home at 57.

The application went through with barely any rework.

We believe that taking time out to care about the client and understand their position makes a broker’s job so much easier. This can be achieved through a good fact-find.

We ensure that we cover any potential risk the lender may see in the transaction. I feel that in the current environment, stating what the risks are and then addressing these risks avoids rework in the future. Someone once told me that if you receive a request for rework, you have failed. That has always stuck with me.

By taking this approach, we assisted the client in purchasing their own home when they thought they were too old. We turned a limiting belief into a possibility.

It was a win-win deal because the client had been paying $700 in rent per week, and the new loan repayments at that time were $689.68 per week. This meant that the repayments were lower and in 18 years she would own her own home.

The retirement income report released last year mentions “the importance of home ownership to the financial security and wellbeing of Australians in retirement”. I was reminded that what we do as brokers matters, as we assist Australians in owning their own homes.

A home for this woman means she can be empowered in her life and have security in retirement.