A new bankless overdraft is about to shake up the SME funding market – while paying an effective trail commission to the arranging broker. GetCapital CEO Jamie Osborn shares the details

For ease, simplicity and familiarity, few financial products beat the overdraft. The UK’s Royal Bank of Scotland takes the credit for creating the first overdraft in the 1720s, when it crafted a facility at the request of merchant William Hog, who was experiencing cash flow issues in an otherwise strong business.

Not only did the solution address Hog’s ongoing cash flow headache, but RBS had a new revenue stream that would soon become a globally recognised financial product. Fast forward to today: the Australian Banking Association lists the overdraft as the second most popular lending product for businesses after the credit card.

However, as endeared as borrowers are to the humble overdraft, its connection to a transaction account has traditionally limited the choice of provider.

“The nice thing about an overdraft is that everybody knows what it is,” says GetCapital CEO Jamie Osborn.

“The biggest innovation in the last couple of decades has been the launch of non-bank products like debtor finance and instalment loans that try to mimic an overdraft – but they don’t quite get there because the lender wants to control risk by limiting the use cases and the customer’s control of the account. We have tried to leapfrog away from that to deliver exactly what the customer wants, which is a true revolving facility.”

As the comparison sites confirm, the GetCapital Business Overdraft isn’t the first commercial overdraft to launch in the Australian market, and it won’t be the last. However, there is one big difference.

“Ours is a pretty traditional overdraft product in that it is fully revolving. A customer can draw and repay as they see fit, but the one key difference is the customer can choose whatever bank transaction account they want to attach it to, which I think has great appeal,” Osborn explains.

It’s even possible for a GetCapital Business Overdraft customer to attach multiple bank accounts to the facility to provide even greater flexibility, which is only possible due to the advent of open banking and the completion of key legislation earlier this year. As Osborn explains, this is the real game-changer.

“With open banking, there is this fantastic opportunity to unshackle from your transaction banking provider and access other financial services. That’s what our overdraft does,” he says.

That an alternative lender is innovating a traditionally mainstream product in such a disruptive way is no surprise in the current climate. But there’s more to the strategy than meets the eye.

“We wanted products and a service offering that play to that mainstream SME market at a price point that resonates with them, too,” Osborn says.

“Business owners want a fast and efficient application process, a credit decision based on the strength of their business rather than the size of their family home, lending products that fit their specific requirements, and a high level of service. In the last 12 to 18 months, in fulfilling those objectives, we have focused on technology, product innovation and bringing a high-quality service offering to market.”

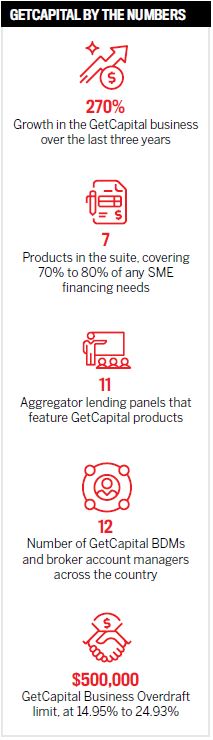

Soft-launched in April, the GetCapital Business Overdraft officially entered the market on 2 September, and Osborn reports that early feedback from both brokers and customers has been strong. In fact, the overdraft is now GetCapital’s core proposition, promoted in the market by a team of BDMs and offered through all accredited brokers. For brokers who aren’t yet accredited, the process can be completed within 24 hours.

Soft-launched in April, the GetCapital Business Overdraft officially entered the market on 2 September, and Osborn reports that early feedback from both brokers and customers has been strong. In fact, the overdraft is now GetCapital’s core proposition, promoted in the market by a team of BDMs and offered through all accredited brokers. For brokers who aren’t yet accredited, the process can be completed within 24 hours.

Non-resi trail

Given the low levels of product literacy and awareness among SME owners, attaching a transaction account at one bank to a revolving overdraft facility with an alternative lender sounds like a complicated deal – but it doesn’t have to be.

First, there aren’t any specific scenarios the product addresses. The reality is, almost any business with a working capital cycle can use an overdraft to bridge a working capital gap. Now there’s simply more competition and choice in who provides that facility.

“We talk about scenarios for our instalment loan and trade finance product, but for the overdraft, we have moved away from that. It has incredibly broad appeal across the vast majority of the SME market,” Osborn says.

That isn’t to say the facility is without requirements; SMEs that apply must have been trading for three years and be able to demonstrate growth.

“If you compare the overdraft to debtor finance or an instalment loan offering, this is more flexible. You draw down on it when you want, you don’t pay any line fees on the facility, you only pay interest on what you have used, and you can pay it back whenever you want,” Osborn explains.

For brokers, the benefits continue – just as the overdraft is ongoing, so too is the commission, essentially providing a trail income for a nonresi loan.

“This is a great opportunity for brokers to build real equity in their business by having that consistency of revenue stream coming in year in, year out,” Osborn says.

Brokers receive an upfront commission on the first draw-down, followed by a monthly service payment based on the outstanding balance on the facility.

“Brokers can now generate a really good revenue steam over the life of their customer. The really good brokers, the ones who can build a book of business and build the revenue stream on their key commercial accounts, are finding this really powerful,” Osborn says.

The start of things to come

Open banking puts customers in the driving seat, changing everything about the finance industry’s traditional power dynamic. As Osborn explains, the GetCapital Business Overdraft is the first generation of that change, launching at a time before open banking is even fully live in the commercial space.

“On the commercial side, there is very, very low awareness, and I think rightly so, because commercial open banking legislation will lag the consumer side of things, but when that does get implemented, it will have significant ramifications,” he says.

“It will make it a lot easier for non-bank providers to innovate, and it is going to increase choice for both customers and brokers in terms of the products offered in the market.”

Osborn compares open banking to the dawn of mobile number portability in the 1990s, which exponentially opened up the telecoms sector, boosting choice and competition as a result. But the world has changed in the last 20 years, and today, choice and competition are second to speed and service – a point on which Osborn sees further change in the coming months and years.

“I think, over time, one of the key things for everyone operating in this space, including ourselves and the banks, is to be conscious of the ‘Uberisation’ of the customer experience. Customer expectations have changed significantly in the last three years and will continue to do so. One of the challenges is how do we stay ahead of the curve as lenders?”

It’s a big question, and one that no doubt has more than one answer, but with a high-tech and high-touch philosophy, GetCapital’s approach to intuitive and transparent service is on track to truly disrupt how businesses bank.