There are a few trends that have emerged out of the coronavirus pandemic which, at first glance, may seem a little surprising. Take Google search trends, for instance. There is some anecdotal evidence to suggest that, after this period of lockdowns and quarantines, the number of search queries for terms like ‘divorce’, ‘sell my property’, ‘how to split assets’ and ‘how to start over’ could surge.

“The unfortunate reality is that there will be many Australians who suff er as a result of the pandemic, whether due to loss of job, small business failure, relationship breakdown or divorce. These types of stressors can mean some bills go unpaid, which can impact their credit rating. But that doesn’t automatically make them a high-risk or non-conforming borrower – it just means they’ve gone through a tough time,” says Daniel Carde, general manager distribution at Resimac.

This is one of the many misconceptions of specialist lending that Carde is keen to stamp out.

In the past, it may have been the case that the only borrowers who sought out specialist lenders were those who were high-risk, with dodgy credit profiles, a poor history of managing money, some financial firestorms in their past and little documentary evidence to back up their application stories.

Today, that’s far from the truth for the average non-conforming loan applicant, Carde says.

Daniel Carde, general manager distribution, Resimac

Daniel Carde, general manager distribution, Resimac

“Specialist lending today is very different to what is was pre-GFC.We’re a lot smarter about it these days, and there’s a lot more science behind it. We all know someone who has lost their job or who has been divorced. We may know someone who has had a small business that hasn’t taken off . They’re not necessarily poor money managers; they’ve just been caught in poor money circumstances,” he explains.

“Specialist lending today is very different to what it was pre-GFC. We’re a lot smarter about it these days, and there’s a lot more science behind it”

“Specialist lending is really no different to traditional lending; it’s about getting down to what actually happened, and most importantly, whether the borrower is now in a better situation. We don’t want to shift borrowers from one lender to another and transfer the pain of the situation over – we actually want to help put customers on the pathway back to recovery.”

Specialist loans also don’t differ from more traditional loans in terms of features.

“Our specialist loans are fully featured, with 100% offset, choice of repayment frequency and repayment type, and free access to redraw facilities via our online platform and through our Visa loan access card. Our focus is on providing the Australian consumer with flexibility and choice, and this includes both prime and specialist borrowers, and whether they are owner-occupiers or investors,” Carde says.

“Our specialist loans are fully featured, with 100% offset, choice of repayment frequency and repayment type, and free access to redraw facilities via our online platform and through our Visa loan access card. Our focus is on providing the Australian consumer with flexibility and choice, and this includes both prime and specialist borrowers, and whether they are owner-occupiers or investors,” Carde says.

Specialist lending, Carde adds, is “countercyclical”, and as we continue to experience a downturn in the economy, “the opportunities within this type of lending increase”.

“When you have a major life event – divorce, illness, small business failure, loss of job – that’s when we can help. As long as the borrower is over that situation and on the road to recovery, then we will try to assist – we may be able help people get out of that situation too,” Carde says.

“If brokers aren’t familiar with our specialist lending products, now is a good time to reach out to Resimac BDMs and have a chat about how you could incorporate these offerings into your business.”

“Often it’s a case of, they’re good borrowers that have potentially come across a not-so-good situation”

Carde, who looks after all of Resimac’s distribution, wholesale and broker direct channels, explains that “everything has evolved with COVID-19”.

Resimac reviews every single loan application on its individual merits, and it’s this bespoke, personalised approach that gives it the flexibility and agility to approve loans that some of the more traditional lenders may pass on.

“The only difference with specialty lending is that there is often a back story. As long as you can provide those details, it’s not that different to a traditional loan”

“There’s a misconception that specialist loans are harder for the broker, or that the borrowers are not of the same quality as those eligible for traditional loans. The reality is that the lending principles are the same, irrespective of the type of loan. Whether it’s full-doc, alt-doc, impaired credit or not, it all boils down to serviceability, security and suitability,” Carde adds.

“The only difference with specialty lending is that there is often a back story. As long as you can provide those details, it’s not that different to a traditional loan. It’s a risk-based approach, and the only way we can make those lending decisions is if we have the full picture.”

Getting that background story and as much information as possible so the lender can clearly assess the risk is crucial to the process, which is why Resimac places so much emphasis on the value added by the broker community, who play an important role in communicating the borrower’s situation and requirements.

“Every loan is assessed on its individual merits by a specialist underwriter, and the more information we get, the better we’re able to process the application. We rely on the broker to articulate the borrower’s information and make sure the story carries over to us, and we place a lot of value in the conversations that our BDMs and brokers have; you can’t really beat a one-on-one conversation,” Carde says.

“Once you’ve lodged a loan, the digital process takes over. We have the tools to allow for non-face-to-face interviews, and we also do digital IDs and digital signatures, but it always starts with a personal conversation.”

For Resimac, which transitioned to a full working-from-home model when the pandemic first hit, ensuring that it is able to communicate with brokers and customers in the most timely and convenient manner is a key priority, whether that’s via phone, video call or, where socially distanced and appropriate, face-to-face meetings.

Right now, staff in Resimac’s Melbourne office are still working remotely, while team members in Sydney and Perth have transitioned back to working in the office on a rotational roster.

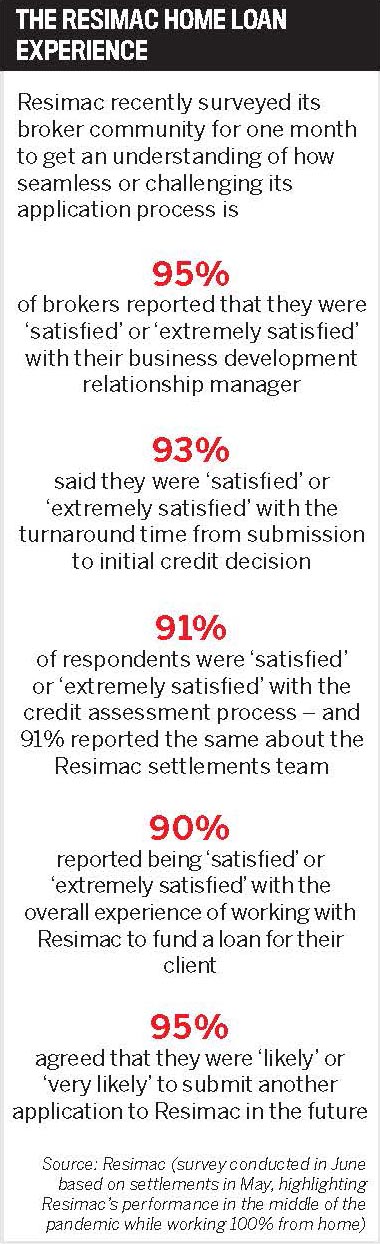

“We brought forward a technology rollout that was scheduled for later in the year to enable us to work remotely, and the process has been quite seamless for us. Importantly, our customers haven’t been impacted. Our SLAs are currently at one day across the board. We’ve been improving our back end to further improve our efficiencies to give us the scale we’re looking for and to maintain those SLAs, which in general have remained fairly consistent over the lockdown period,” Carde says.

For brokers who are considering introducing these types of loans in their businesses, this may be the ideal time to take advantage of opportunities in the market, he adds.

“If a borrower starts a conversation with you by saying, ‘I’ve been to my bank and I’ve been knocked back’, don’t switch off because they don’t conform to the traditional loan. Rather, ask a few questions around their situation. What are they looking to do and why wasn’t their bank able to help them? You can then look at what solutions are available, which might include Resimac,” Carde says.

“Often it’s a case of, they’re good borrowers that have potentially come across a not-so-good situation. You can package the loan up like you would any other loan, then add in the notes about the unique factors of their specific situation, and that’s it. There will be many borrowers looking for that road to recovery in the not-too-distant future – who want to get back into the property market, or tidy up their finances – and the opportunities for brokers to assist will abound.”