By

Brokers are an integral part of MyState Bank’s drive for growth as the Tasmania-headquartered lender unveils exciting plans to boost technology, staff and its national footprint, led by its new leaders in the third party channel, Huw Bough and Blake Albones.

My state bank's general manager of banking, Hugh Bough, is excited by his new role and the opportunity to bring a sharp focus and energy to the organisation’s crucial partnership with brokers.

He was general manager of retail and business banking and broker at MyState for four years until 2019 when he left due to family wellbeing reasons. Following that he became a consultant to Avant on its lending strategy and identified a joint-venture opportunity, which led to him becoming chief operating officer at Kooyong Avant, providing specialist lending for medical professionals.

Now that he’s back at MyState, Bough has some unfinished business and is keen to use what he learnt at Avant to assist brokers going forward.

Now that he’s back at MyState, Bough has some unfinished business and is keen to use what he learnt at Avant to assist brokers going forward.

“Whilst I’d been a broker before, this gave me a really current, first-hand feel for the challenges that brokers face every day,” says Bough. “Having walked in our partners’ shoes, and I view our brokers as our partners, we have a much better understanding of what’s required.”

Bough says he knows brokers are small businesses that face many challenges away from the mortgage process, such as staff, revenue, marketing and customer experience. He says MyState is here to help, with a plan to provide better technology, faster turnaround time and more relationship managers, and to extend the bank’s reach across Australia.

“Technology and consumer behaviours have changed,” Bough says. “If I look to the broker industry, I think we’re going to find that lenders that have a deeper understanding of the channel and are closer to the customer are going to partner better.”

Bough says because MyState is a small organisation, everyone in the bank is talking either to a customer or to a broker.

Looking back at his prior MyState role when he started opening up the broker channel, he says this was informed by feedback from Tasmanian brokers.

“It’s that ability to listen and learn and partner at a deeper level that I think puts us in a pretty unique position.”

Bough says he’s passionate about the broker channel, and the biggest factor that drew him back to MyState was the people.

“It’s that human element to the channel that allows us to create a point of difference.

“We have a hugely talented group of people, and the appointment of Blake Albones is proof positive of our strategy of backing people who believe in the channel.”

Albones, MyState’s new head of home lending distribution, who will look after retail home lenders and brokers, has more than 20 years’ industry experience. He was previously the CEO of brokerage RateOne Financial Services, head of NAB Broker for Victoria and Tasmania, and a senior BDM at PLAN Australia.

Albones, MyState’s new head of home lending distribution, who will look after retail home lenders and brokers, has more than 20 years’ industry experience. He was previously the CEO of brokerage RateOne Financial Services, head of NAB Broker for Victoria and Tasmania, and a senior BDM at PLAN Australia.

“He understands credit, he understands product, he understands policy, but most of all he understands what partnerships stand for, and partnerships in the broker channel are what counts,” Bough says.

As for his own role, Bough says it presents a unique opportunity to be able to lead a bank that has an enormous appetite for growth and seize that growth through the broker channel.

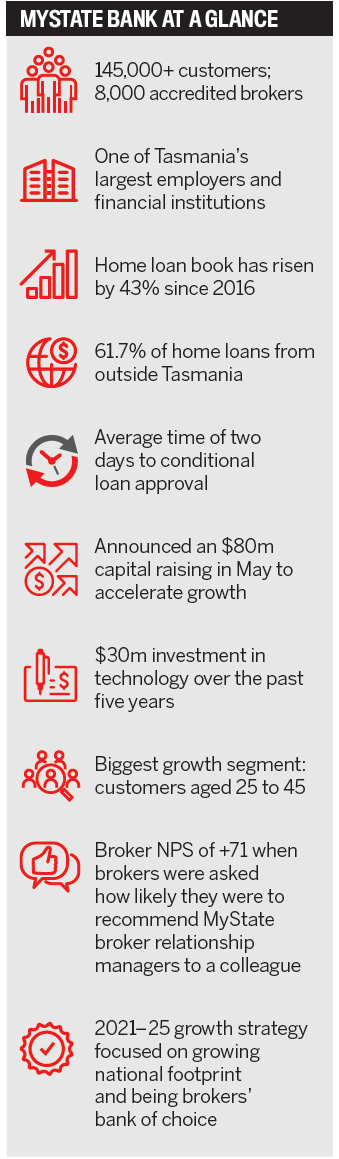

Since 2016, My State has increased its home loan book by 43%.

“We now see an opportunity to build on that success and substantially increase our growth trajectory.”

Brokers are an integral part of MyState Bank’s drive for growth as the Tasmania-headquartered lender unveils exciting plans to boost technology, staff and its national footprint, led by its new leaders in the third party channel, Huw Bough and Blake Albones.

Bough says MyState went to the market in May to undertake a $80m capital raising to rapidly accelerate its 2021–25 growth strategy, and a key part of this was dedicated to the broker channel: “We want to be a broker-led bank.”

Technology is also crucial. Bough says the bank’s ability to undergo digital transformation faster than its competitors means customers find MyState easier, more trustworthy and intuitive to deal with, and it ultimately attracts more customers.

“We’re respected as a digital challenger brand. I think we’ve got an enormous opportunity to be able to grow off the back of that, and that’s because we are a simpler, easier, more focused bank.”

Recent home loan growth has been partly driven by the First Home Loan Deposit Scheme, but the fixed rate market, owner-occupier refinances, and, in Tasmania, the property investment business, are all particularly strong.

Ongoing COVID lockdowns would cause a blip in the economy, Bough says, but he believes there’ll be a speedy recovery.

“One thing that’s happened that’s of use is that we’re able to do things digitally, and there’s been more change in that space by banks across the board, so brokers are able to change how they operate.”

“One thing that’s happened that’s of use is that we’re able to do things digitally, and there’s been more change in that space by banks across the board, so brokers are able to change how they operate.”

MyState has invested in a new technology stack, built over the past five years at a cost of $30m, which will help reduce IT costs and improve the personalisation of services to the bank’s 145,000 customers and 8,000 brokers across Australia.

In the last 12 months, MyState has launched a market-leading AI-based solution to provide customers with insights on spending, bills and savings as well as auto-savings capability.

Bough says better technology allows the bank to scale more efficiently as competition for lending products intensifies.

“Our biggest growth segment is now customers aged 25 to 45 – that just says how well we’re doing in the digital space. Customers are starting to see us as a neobank.”

For brokers, Bough says lending processes and policies have been streamlined and supporting documentation reduced to make it easier for brokers to do business with MyState.

“Where possible, MyState Bank also relies on AVEs [Automated Valuation Estimates] saving time with property valuation and speeding up the time to assess the loan.”

Bough says new features will be added to MyState’s broker portal, which includes ApplyOnline for loan applications.

Unlike many other banks that have offshored back-office services, Bough says MyState’s residential mortgage broking credit decisioning and processing teams remain in Tasmania, which provides easy access to decision-makers.

“We’re really proud of the fact that we’re close to our customers, that we collaborate to win, that we are always chasing the better … and that really means having people onshore,” he says.

“We had a customer that had an urgent settlement – the broker called me up and it was the same day. He’d been given my name by a friend, and I was able to walk downstairs and ensure we met that customer’s needs.

“That ‘moment of truth’ really makes a difference for our partners and customers.”

A recent MyState survey of brokers revealed that 75% of respondents said turnaround times had worsened since the end of 2020.

Bough says he wants to maintain and improve on the bank’s consistently fast conditional and unconditional turnaround times.

“We’ve been essentially at two days for conditional approval for the last year. Despite [loan] volumes going up quite dramatically, we’ve held to that.”

Turnaround times and customer satisfaction are measured “every minute of every day” to ensure MyState is delivering for its customers and partners.

While vastly different turnaround times between branch and broker have been a major frustration for brokers when dealing with some banks, Bough says MyState doesn’t diff erentiate between channels.

“If a customer comes to one of our retail lenders or they come through the broker, they get the exact same delivery in terms

of service. You can’t penalise a customer’s choice of channel – we are channel agnostic, and the majors should be too.”

Bough says the core advantage of MyState over other banks is the customer experience.

“I’m a big believer that if we delight customers they will advocate for the bank and the brand, and they’ll give brokers referrals. A happy customer is likely to give brokers extra business and stay with us longer.”

Bough says one of MyState’s goals is to be the number one bank in its heartland of Tasmania.

“We’re very close to being the biggest bank in Tassie; we’ll do that ff the back of the strong broker business and support and learnings we get from there.”

This would then provide a platform to increase MyState’s presence across Australia, particularly in Victoria, NSW and Queensland, and help it become “the broker’s bank of choice”.

While MyState has bank branches in Tasmania, Bough says these are not necessary on the mainland.

“Every broker for us is a branch, because they’re talking and dealing with a customer; everything else

is digital.”

He says it’s important to maintain and improve on MyState’s net promoter scores from brokers.

In a recent broker NPS survey, the bank received an exceptional score of +71 when brokers were asked how likely they were to recommend their MyState broker relationship managers (BRMs) to a colleague.

When asked why brokers should recommend MyState to their clients, Bough says: “You know that when you make a recommendation, the people that we have will treat it respectfully and treat it as a genuine partnership, because we are reliant on each other to deliver the best experience we can for the customer.”

MyState’s growth plan extends to its staff , with three new BRMs being hired in Victoria, as well as recruitments in NSW. It recently appointed Neville Anitelea as senior manager for broker marketing and communications to boost engagement with brokers.

Bough says the bank’s broker portal provides everything a broker needs to know about working

with MyState.

Other activities planned over the next year to increase broker and customer awareness of the bank include advertising, PR, new sales support collateral, virtual and face-to-face events, and aggregator and broker education programs such as lunch and learns, roundtable discussions and Webex masterclasses.

Albones is looking forward to his new broker-facing role at MyState.

“My time at RateOne allowed me to see what brokers deal with daily: the frustrations from poor service standards by mainstream lenders, the inconsistency in credit decisions, and even simple tasks becoming too complicated,” says Albones.

“My vision for MyState is to be the broker’s bank which makes things simple again and supports the broker’s own business to thrive.”

Albones says the bank has ambitious and audacious growth targets.

“To achieve them, we need to be a lot more aggressive in the bigger markets of Victoria and NSW. We need a salesforce that is committed to providing a great broker experience and therefore great customer outcomes.”

MyState has invested heavily in its digital experience, which will complement the bank’s market-leading service.

While COVID restrictions have meant fewer opportunities to meet brokers in person, this has taught the MyState team to be a lot more efficient when it comes to communication.

“Brokers have become time-poor as a result of complexity creeping into this industry, and therefore shorter, sharper and more precise conversations are preferred,” Albones says. “Using data to drive conversations is paramount.”

More brokers are turning to MyState because it is broker-friendly, he says. “It has award-winning products, NPS results that other lenders are envious of, and a compelling service proposition.”