Market-leading alternative lender Pepper Money knows brokers want intuitive and accessible technology to quickly find the right loan product for their clients. CEO Mario Rehayem explains how Pepper’s digital roadmap is achieving this.

There has probably been no greater catalyst for investing in technology than the COVID-19 pandemic.

With so many people working remotely, there has been a paradigm shift in the way lenders operate in terms of broker, customer and staff interactions, their websites, CRMs and systems for loan applications, credit policies, decisioning and more.

The companies that already had in place robust and innovative technology when COVID hit have performed the best – they have been able to scale up products and services to meet the huge demand for home loan finance in an era of record-low interest rates.

Non-bank lender Pepper Money is well ahead of the game when it comes to technology that ensures fast and efficient service for its brokers and customers.

“Technological innovation is key to delivering great outcomes for our broker partners, their customers, and the ongoing success of our business, ensuring we maintain our market-leading value proposition,” says Pepper Money CEO Mario Rehayem.

He says the social and economic impacts of the past 18 months have only accelerated broker and customer expectations that they can conduct business online.

“Now technology is front and centre of the broker and customer world – and that’s why we are investing in having the right tools and technology for today and the future.

“Pepper Money continues to transform and invest in new ways to improve the broker and customer experience through technology. So we’ll continue to evolve and listen to the market and understand the pain points that a broker/introducer faces in their interactions.”

Rehayem says ultimately it’s Pepper Money’s responsibility to remove those friction points in both the application and customer onboarding process.

“Our digital journey started several years ago as we redefined our strategic focus to be more responsive to customer and broker expectations. We strategically shifted to building our own Pepper-style technology and applications rather than opting for platforms that do not offer the same level of personalisation.”

Pepper isn’t interested in providing a generic digital offering, says Rehayem.

“We want to give our customers and partners the unique Pepper Money experience that complements and accelerates the great service our people give to brokers and their customers every day at scale. It is all aimed at making interactions as intuitive and easy as possible for our brokers and customers to deal with Pepper Money, however they choose to interact with us.”

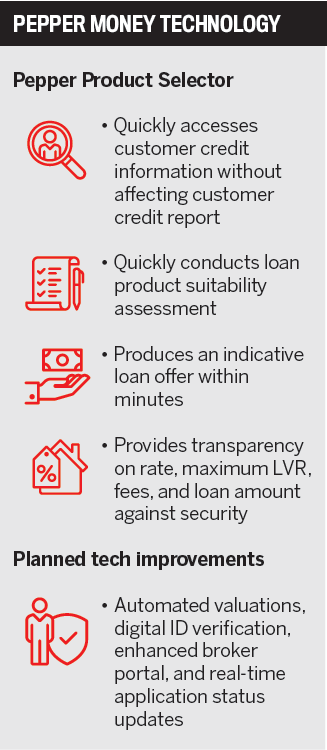

One of the key features of Pepper’s digital roadmap is the Pepper Product Selector (PPS) tool, which was launched in 2018, with new customers benefiting from changes to the origination process.

“Put simply, there is nothing like it in the industry. The innovative tool was designed to save brokers time and provide confidence that the Pepper Money recommendation given to the customer means no surprises post-submission,” says Rehayem.

PPS allows brokers to identify a Pepper Money home loan product, interest rate and fees for any customer efficiently.

“All they need to do is complete a series of questions about their customer’s loan scenario, and within minutes PPS accesses the customer’s credit information without leaving a credit enquiry footprint, conducts a product suitability assessment and presents an indicative offer that Pepper will honour subject to credit review.”

The advantages of PPS are numerous: in under five minutes (or as fast as a broker can type) the customer can have an indicative offer from Pepper Money.

“The customer will have transparency on the rate available to them, the maximum LVR, fees and the loan amount on offer against the security, without impacting the customer’s credit report – and there are no surprises.

“If they are happy with the indicative approval, the customer and broker can proceed the application with complete confidence.”

Rehayem says the probability of conversion is significantly increased, which means PPS is the most efficient way for a broker and their customer to apply for a Pepper loan.

“Since then, we’ve continually optimised the platform and consulted with brokers, who regularly use the tool to meet their expectations.

“We’re also integrating tools to assist with digital verification of identity and income, as well as electronic signatures.”

Existing Pepper customers are benefiting from the lender’s digital innovation as much as its broker partners, with the introduction of online mortgage statements last year.

“By the end of 2021, both our asset finance and mortgage customers will have an enhanced online experience that will allow them to transact and manage their loans in an intuitive and convenient way.”

Comprehensive credit reporting has also provided Pepper with more opportunities to help brokers and customers access the right loans for them. It adopted CCR two years ago and hasn’t looked back.

Rehayem says when applying for a loan a lender might consider, among other information, a customer’s credit report.

“In the past, the report may have shown applications for credit products and any defaults. Under CCR this has expanded to include up to 24 months of the customer’s repayment history, when they opened and closed credit accounts, and how much debt they have overall.

“This means a lender now has a more comprehensive picture of the customer’s financial situation and can off er a loan tailored to their circumstances.”

Pepper Money has fully incorporated CCR into its credit decisioning processes in a way that supports its commitment to fast turnaround times.

“We have eliminated the need for loan statements up front to refinance a home or consumer loan where a customer’s current lender is participating in CCR and the data is available. And if a customer already knows their credit score before meeting their broker, it potentially makes positioning a non-conforming loan an easier conversation to have.

“Using their score as evidence, it may help them understand why they’re not going to be able to get the interest rate they’ve seen advertised, and allow the broker to identify a more appropriate lender for them.”

Rehayem says it can also mean a broker might be able to off er a customer a better outcome, if their score is better than expected.

“With 50 lenders today now opted into the regime, awareness of CCR amongst brokers is much greater than when Pepper Money first adopted CCR two years ago.

At the time, we saw an opportunity to educate the industry on the benefits that CCR would bring to lending, running roadshows, webinars and BDM presentations.”

Pepper’s digital innovation is paying off, and the feedback from brokers has been positive.

“I have no doubt that our technological capabilities, in conjunction with our market-leading customer service delivered by our BDMs, credit team and operations staff, have underpinned the growth we’ve enjoyed over the past three years. Brokers who regularly use our digital tools tell us how much they enjoy the consistency of outcomes, speed of turnaround time, and overall experience they deliver.”

Rehayem says a broker recently told him how they use PPS for every single Pepper Money application and wouldn’t submit a loan without checking PPS first.

Rehayem says a broker recently told him how they use PPS for every single Pepper Money application and wouldn’t submit a loan without checking PPS first.

“They loved how it helps to save them time with phone calls and emails, when they can get a fast answer any time of the day and submit the loan with confidence.”

But Pepper is not resting on its laurels when it comes to investing in technology.

“Pepper Money is continually looking for new ways to simplify the lending process, and we have already been leveraging our long-term investments in data, analytics and AI to create better outcomes and experiences for brokers and customers.”

In New Zealand, Pepper’s originations platform can already identify the different types of documents collected by mortgage advisers, assess what is required, then automatically extract data from items such as application forms, driver’s licences and passports to streamline what is traditionally a very lengthy process.

In Australia, Sage is a platform designed in-house by Pepper to deliver a fully integrated cloud-based originations platform that has the broker, customer and employee’s needs at the centre of its design.

“For our credit officers it brings the latest technology to their fingertips, which significantly reduces the time to assess a loan,” says Rehayem.

Other improvements brokers can look forward to include automated valuations, digital ID verification, an enhanced broker portal and real-time application status updates for the broker and customer.

“All of these enhancements are aimed at improving our already market-leading turnaround times to unconditional approval, and a more advanced seamless, effortless, precise and consistent service.

“We are in an ever-evolving industry, and the ability to adapt and invest in our technological capabilities is paramount to our ongoing success and commitment.”