By

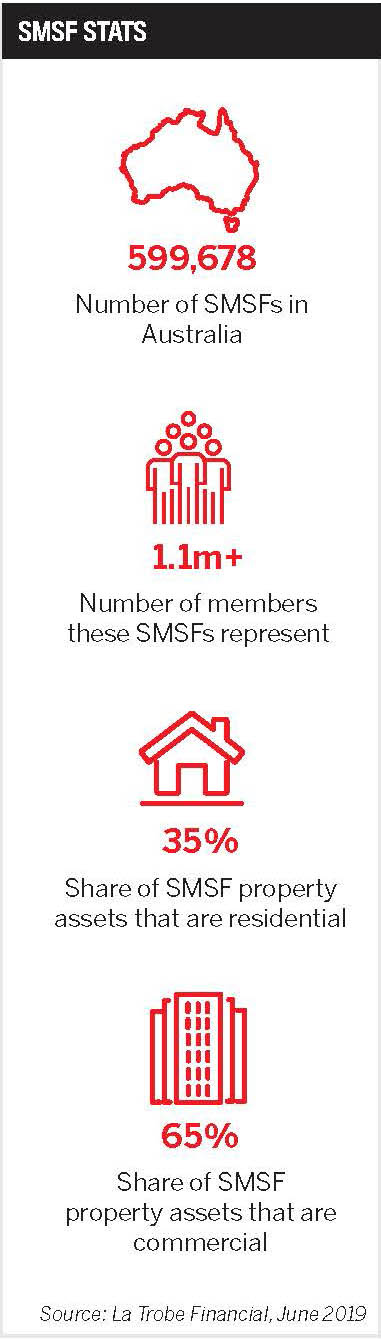

The proportion of SMSF lending-based property assets has increased over the last decade, growing from under 5% in 2012 to over 20% of total assets today.

But while all sectors of the mortgage and finance market have been impacted by what Cory Bannister, chief lending officer at La Trobe Financial, describes as the GVC, SMSF lending has shown its resilience.

“Without doubt, the biggest impact on the SMSF lending space has been the outbreak of COVID-19, which has been labelled the ‘global virus crisis’, or GVC. We expect the ripple effects from the GVC to be felt well into the year ahead, which will produce a heightened sense of caution amongst property investors generally,” Bannister says.

“The pandemic has impacted demand for housing finance generally, and SMSF lending demand is not immune from this impact. However, in terms of product performance, our experience is that SMSF loans have shown a greater resilience to the impact of COVID-19, which is no surprise given the steady and reliable performance of the product over time, thanks to the product’s unique mechanics.”

Bannister points to some of the risk mitigation factors, such as the fact that SMSFs often hold a substantial portion of their assets in cash, as being key to this sector’s resilience in trying times.

“This effectively provides a liquidity buffer for when asset returns – rental income, in the case of property – are delayed or outstanding for a short period,” he explains.

“For PAYG members, contributions to the SMSF are regular and consistent, providing there is no disruption to their employment situation. This provides the fund with an increasing level of available assets, subject to the performance of the fund, to be used where required to meet fund liabilities.”

Unlike standard loans, the discretionary expenditure of the SMSF members also has no impact on the borrower’s ability to meet loan repayments, as the assets cannot be drawn upon unless they are in the pension phase – which also mitigates the risk of repayment default, Bannister adds.

Cory Bannister, chief lending officer, La Trobe Financial

Cory Bannister, chief lending officer, La Trobe Financial

“Brokers should consider offering SMSF loan products as part of their overall diversification strategy ... Unless brokers cater for their clients’ full finance needs, there is an increasing risk that clients will look elsewhere for a one-stop shop”

Moving forward, he suggests that brokers who are interested in diversifying into the SMSF lending space could forge a solid path forward as we progress into the second half of 2020.

Historically, commercial lending through SMSFs has been where the biggest opportunity has existed for brokers, as it’s represented a much greater share of portfolios than residential. Bannister says commercial property will remain an attractive proposition for SMSFs, particularly for self-employed individuals looking to acquire a site from which to operate their business.

“For investors looking to add commercial property to their SMSF portfolio, we believe there will continue to be considerable opportunity for potential investments. However, there is an elevated level of risk to this strategy, and we would encourage any investor to seek professional advice, particularly during this time of uncertainty and volatility,” he says.

“Looking ahead, we anticipate strong demand for light industrial property as the e-commerce and data storage industries continue to grow. Turning to residential assets, with work from home capability on the rise, we see potential for growing demand for urban-fringe property as buyers seek affordable family homes where they can work and live. These urban-fringe areas have historically been very popular amongst SMSF investors.”

For brokers who are yet to get involved in commercial transactions, there are a number of considerations they should weigh up before moving forward. First and foremost is the fact that, within the current finance market for SMSF loans, brokers who have always relied on the banks for their lending needs will now have to think about looking at non-banks in the market to meet their clients’ needs, Bannister says.

“At La Trobe Financial we have one of Australia’s broadest product ranges. For our SMSF loan product, we can lend up to an LVR of 80% for residential-type properties and up to 70% for commercial-type properties,” he says.

“At La Trobe Financial we have one of Australia’s broadest product ranges. For our SMSF loan product, we can lend up to an LVR of 80% for residential-type properties and up to 70% for commercial-type properties,” he says.

“Our product specifications and processes are simple for brokers to understand, and our credit team is very experienced in these types of loans. Our team is always available at the end of the telephone to assist finance brokers in the process.”

Those brokers who have an appetite for introducing SMSF lending into their business may find value in reaching out to their referral partners, such as accountants and financial planners, to let them know they have diversified into this space, Bannister suggests.

“Not only can this help to establish a steady and sustainable supply of regular quality clients, but brokers can also work with these people to ascertain whether borrowing through an SMSF structure is appropriate for the clients,” he explains.

“We would recommend that clients have an SMSF in place already, unless they are coming to a broker with advice from an adviser and are in the process of establishing an SMSF. We do not recommend that clients be encouraged to establish an SMSF unless they receive independent advice from a financial adviser.”

One example of where it may be appropriate for a broker to recommend seeking advice about setting up an SMSF is when the client is self-employed and currently leasing their place of business.

“In terms of product performance, our experience is that SMSF loans have shown a greater resilience to the impact of COVID-19”

“If they hold adequate funds in their superannuation fund, it can often make good commercial sense for them to purchase their business premises through an SMSF. Through this structure, they can use cash flows from their business to pay their mortgage, instead of paying someone else’s by way of rent. It is a discussion your client might wish to have with their financial adviser,” Bannister says.

“Broadly, brokers should consider offering SMSF loan products as part of their overall diversification strategy as it is a significant growth area that is likely to include a number of their current and future clients. Unless brokers cater for their clients’ full finance needs, there is an increasing risk that clients will look elsewhere for a one-stop shop.”