Cory Bannister, vice president and chief lending officer at La Trobe Financial, explains how brokers can develop life-long customer relationships through diversification

Whether they are looking for commercial, residential or personal loans, there is no shortage of borrowers in Australia, and often, once a borrower has enjoyed the services of a broker, they rarely go back to doing things for themselves.

Onboarding a new client and becoming their broker for life requires extensive product knowledge, experience and a commitment to presenting new solutions.

That said, many brokers are already successfully embracing multiple business streams as a way to insulate their companies from negative market trends. For example, in the six months before royal commission hearings started, the MFAA’s Industry Intelligence (IIS) Survey confirmed the average value of a broker’s loan book had increased 6% when compared to the last period, to reach $38.1m, predominantly off the back of diversification.

“We have found over time that our purpose has driven us to cater for all areas of a customer’s life cycle,” says La Trobe Financial VP and chief lending officer Cory Bannister. “Our objective is to continually solve customers’ unmet financial needs through product innovation, and deliver one of Australia’s broadest loan and investment products in the market.”

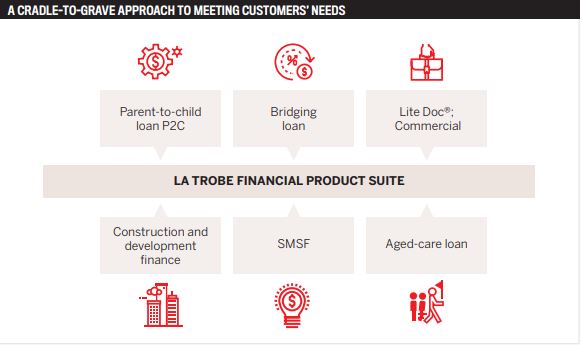

Taking a cradle-to-grave approach, La Trobe Financial’s product suite caters to the needs of first home buyers, upgraders, business owners, those looking to build a home, mum-and-dad investors, and borrowers looking to finance their aged-care transition (see box).

“Our customer life cycle approach suits the finance broker’s core value proposition. You see, consumers don’t want a residential broker, a commercial broker and an SMSF broker; they want to build a relationship with someone that they can go back to throughout their life for all their financial needs. Someone that knows their situation, knows where they’ve been and understands where they are going,” says Bannister.

“That is how brokers build clients for life.”

Real people, practical products

Each product in the range is founded on its own set of unique demand drivers, which themselves are closely tied to economic and social trends, such as employment, property and retirement.

For example, nationwide property values declined 2.4% in 2018, driving affordability up by 1.5%, according to the HIA Affordability Index. In many areas this has prompted people to snap up properties while the buyers’ market is strong. A credit fund is a capital-stable investment that can be leveraged over a fixed term to help a client achieve such financial goals.

For example, an individual investor who wants to save for a first home deposit, or even purchase a car, can use a product such as the 12-month Term Account to achieve the desired return on their savings. However, while affordability is improving many first home buyers still require support from the bank of mum and dad.

This has driven interest in P2C loans, which effectively allow first home buyers to borrow 100% of the purchase price without paying LMI premiums. Prior to the P2C loan, parents had only three ways to help their children secure a home, and few options were attractive: they could choose to act as a guarantor, gift a deposit, or buy the house with their children as co-purchasers. “P2C is a much better alternative as it does not require parents to enter into any guarantee or place their property at risk. We can take care of all the paperwork. and parents determine the loan term and interest rate charged,” says Bannister.

Further, the P2C loan addresses the issue of intergenerational wealth protection by safeguarding the parent’s investment. Research published by the Australian Financial Review estimates that the baby boomer generation holds $3trn in transferable wealth, which will be passed down over the coming two decades. This means there is additional opportunity to guide a client on how to best protect wealth held in property for the benefit of younger family members.

“The P2C loan is specifically designed to protect the parents’ investment without exposing their assets or credit profile to any risks associated with their child running into difficulty with repayments,” Bannister explains.

.jpg)

“Mum and dad’s house is not used as security for your P2C home loan, and the children still qualify for the First Home Owner Grant and applicable stamp duty concessions, if eligible.”

Life events also shape demand for finance, and retirement is just one of them. In 2016, 15% of the total population was aged 65 or older, and by 2056 the Australian Institute of Health and Welfare predicts the figure will reach 22%.

That means that over the coming years more retirees will need more ways to fund their retirement and, eventually, aged care. Loans and reverse mortgages are often the most suitable solution.

“Most people will know someone who has or is going into an aged-care home. A broker adding this product into their portfolio adds value to their clients indirectly and in times of emotional stress,” says Bannister.

Meanwhile, other factors are driving a surge in interest in lite-doc loans, including the rise in gig economy workers – people who tap their entrepreneurial spirit to draw an income from a variety of sources.

Figures released in January by the ABS confirm that sole-proprietor businesses showed the largest annual increase in the number of active enterprises in 2018, up 7.3% over the year. Today, 62.1% of registered businesses in Australia don’t employ staff.

Despite the strength of the sector, the mainstream financial market is not geared up to accept low and lite-doc loan applications, and these borrowers can often find themselves with limited options, despite their seemingly strong financial position. “Brokers today more than ever should maintain regular ongoing contact with their clients to ensure they are not missing opportunities and are acting in the best interests of their clients,” says Bannister.

“Not only are an individual’s circumstances likely to change over time; we are seeing regular changes in the finance, economic and regulatory environments that could mean that the plans and pathways you discussed with your clients 12 months ago are likely to have changed and may not even be viable any more.”

Tapping the CRM

In almost all circumstances, these opportunities can be found in the broker’s CRM, which is one of the most valuable resources at their fingertips.

But every interaction counts, and often the clients with the most comprehensive requirements can be identified during their first broker meeting.

“Identify and map out as many future requirements as you can, record them in the CRM and set reminders and alerts to follow up. In addition to these specific checkpoints, a biannual personal check-in along with automated touchpoints might be an appropriate strategy,” says Bannister. During this stage, he advises that it is essential to gather a summary of the client’s borrowing history, as this often reveals who they are, what they do and what their likely objectives are in the future. “Listen intently and take plenty of notes,” says Bannister.

“Once a broker has the full history and roadmap, they should explain how they can help the customer reach their financial goals, undertaking to put a written proposal in place that demonstrates how they can help them over time.”

Partnerships can also bring new opportunities. Thousands of brokers collaborate with real estate agents, accountants and other referral partners, and such relationships are particularly useful when dealing with the more complex products, such as commercial or SMSF lending, from the perspective of both generating new business and sourcing support.

“We would suggest brokers align themselves with complementary partners, such as financial planners or accountants, who can be a good source of referral for these types of transactions. In addition, they should make themselves known to their aggregator BDM or state manager,” says Bannister.

The last piece of the puzzle is language: Bannister advises that brokers should take the valueadding approach, rather than referring to meeting the client’s lifetime needs as ‘cross-selling’. With all these factors in place, it is then possible to measure the customer lifetime value (CLV) by refining the approach and analysing its effectiveness.

“CLV is the prediction of total value that a customer brings to your business over the entire life cycle of the relationship. This not only helps with budgeting but can increase the value of your business, which is obviously important as you move through your own life journey into retirement,” says Bannister.

Specialist or generalist?

At various points throughout their career, many business leaders are forced to decide whether they will be a specialist or generalist – a person who can answer almost any query, or a niche operator with an expert skill set. There are pros and cons on both sides of the debate.

Client retention is essential to support a thriving and diversified broker business, and the latest IIS figures indicate that many brokers are already moving in this direction.

.jpg)

.jpg)

Regulatory and market changes also place downward pressure on profit margins, again increasing the need to protect and grow income streams through diversification.

“Our purpose has driven us to cater for all areas of a customer’s life cycle [and] solve customers’ unmet financial needs through product innovation” Cory Bannister, VP chief lending officer, La Trobe Financial

In the new lending environment – in which banks, non-banks, fintechs and neobanks compete to offer ever more comprehensive products – the ability of the broker to provide new solutions that support a client at every stage of their life is only heightened.

However, in broking – a space in which the trends of the business world and lending environment converge – the choice between specialist and generalist takes on a different meaning. Ultimately the broker becomes both – offering a wide range of services while specialising in the client’s best interests and lifetime needs. For Bannister, the bottom line is clear: “In order to build ongoing and lasting relationships with customers, you need to be able to provide a solution when they need it, he says.”