ASIC’s latest report reveals concerning trends around the expectations placed on brokers, as well as the financial literacy of consumers. Australian Broker examines the findings and how they could influence future regulation of the industry

The last working week of August was another big one for the mortgage broking industry. Hot off the heels of the government’s draft NCCP amendment, ASIC released its landmark report Looking for a Mortgage: Consumer Experiences and Expectations in Getting a Home Loan.

According to ASIC commissioner Sean Hughes, the timing of the report is purely coincidental. However, over 77 pages, more than 2,000 customers told the regulator how their experience of dealing with a broker compared to dealing with their bank.

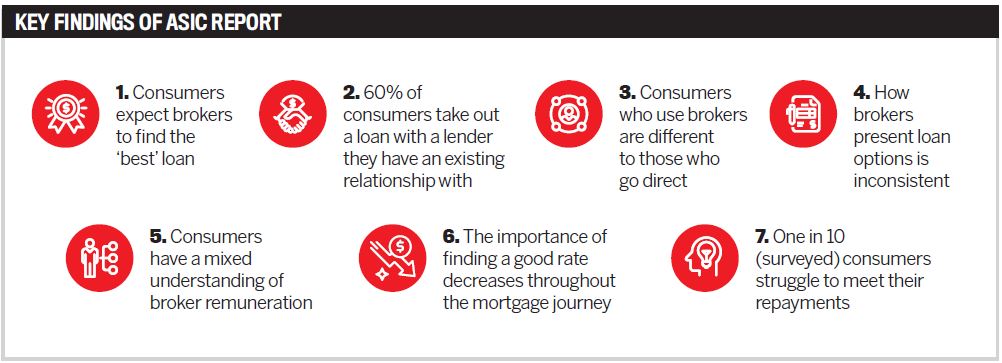

There were seven headline findings (see box), but ultimately what ASIC wants is for lenders, brokers and aggregators to make it easier for consumers to compare loans, while better communicating the loanselection process. It’s a topic on which Hughes doesn’t mince his words.

“My personal view on this is that if mortgage brokers want to be viewed by their customers as a profession, then, like any other professional group, it’s important they source the best information and present it objectively so all the cards are on the table and people understand what their various options are.”

Although ASIC says brokers need to be more consistent, little to no provision is made in the report for a consumer’s misaligned expectations or general lack of financial literacy. It’s merely the start of the catch 22s.

Further, ASIC takes issue with the fact that 33% of consumers receive only one loan option from their broker – apparent empirical evidence that brokers are slacking on the job. Yet direct customers came out with even fewer options, as 69% borrowed from an institution they already banked with.

Hughes maintains that ASIC is “not a black-letter regulator” and that the body has no interest in, for example, setting a minimum number of options to present to a customer. However, it is interested in tackling the “inconsistent” nature with which brokers present these options.

“What is clear from this consumer-driven report is that [consumers] were disappointed. There were quite a few stories where people thought they were going to be getting something better than they ultimately did,” says Hughes.

Consumer expectations aren’t unfounded; many are rooted in such things as the figures pumped out by online loan calculators, and picking up after this is already a major bugbear for brokers.

Consumers dislike it too, as detailed in the report, but ASIC plans to unveil its own interest rate comparison tool next year to “improve price transparency for consumers”. It will also collaborate with aggregators to standardise “what brokers do in terms of assessing the requirements and objectives of customers”.

The Financial Rights Legal Centre claims that ASIC’s research provides “further evidence the broking sector needs reform”; however, industry associations report that broker market share continues to climb, largely on the back of customer satisfaction.

The true picture likely lies somewhere in between, but unless moves are made to enhance the transparency of consumer surveys, brokers will remain vulnerable to the vested interests they can so easily promote.