HSBC talks to Aussie Home Loan's franchisee brokers about the service proposition of non-major lenders

Among consumers, how strong is HSBC’s brand recognition for mortgage products?

Peter Corta: Where I am in Brisbane, it really depends on the demographic. People who don’t have a lot of experience with banking haven’t much recognition of HSBC, but for those who have travelled or lived overseas the brand is well and truly in their minds. Most people tend to know the big four and maybe one or two others.

Sana Hosseini: We are in inner Melbourne and find that our customers are mostly young professionals who are well travelled and know HSBC. In my regional store, we do more to introduce HSBC.

Olivia Lane: I’m based in Sydney and many of the people we deal with are professionals who travel often. The others are expatriates, are aware of HSBC and may even hold an account with them in their home country.

Reema Katrib: I have a lot of customers in Sydney’s eastern suburbs, and they are all savvy enough to do a lot of online research before meeting with me, so by the time I get there they often know what HSBC is offering. Those clients are rate driven because of the loan size. I also find a lot of my customers like the fact that, with HSBC, they can go to different countries and still use the same bank.

As brokers, how have you been able to leverage HSBC’s international brand presence to diversify from straightforward residential lending and work with foreign investors, visa holders, Australians with international jobs, etc?

As brokers, how have you been able to leverage HSBC’s international brand presence to diversify from straightforward residential lending and work with foreign investors, visa holders, Australians with international jobs, etc?

Peter: It has been phenomenal for me. I work with Australians living overseas, and having HSBC has just made that so much easier. Some bank with HSBC already as Premier account clients, so as soon as I mention the brand they’re on board. And aside from rate, their international reach is the biggest draw for my clients.

Reema: I have a few customers who hold a Premier account. It offers the full package – overseas branches, easy access to funds, and visas haven’t been a barrier.

“When things go wrong, it doesn’t matter who is actually at fault; in the eyes of the customer the broker gets the blame” Olivia Lane, Aussie broker, Sydney, NSW

Olivia: The brand recognition is really great. HSBC is familiar with foreign income and will work with us and our borrowers to ensure we’ve lent them all we can.

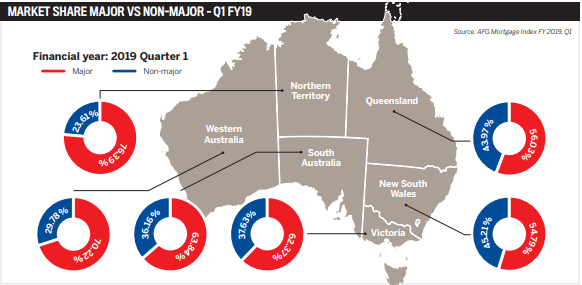

As the non-majors continue to enjoy a record market share, what do you consider to be their role in helping brokers to build their businesses?

Peter: It’s about proposition and service. Consistency between assessors is also vital. I guarantee that I can put a deal into As we have found regulators becoming more particular, lenders are moving into niches based on their risk appetite and how they want to do business, so a wider choice of lenders is even more important.

Reema: A non-major bank provides customers with more options.

The rate is important, too. Clients often show me a rate they found with an online comparison site and expect to be able to get it in real life.

Peter: Anyone can calculate their borrowing capacity online. They come to you with a number, and most of the time you have to disappoint them because that figure is so inflated. There will always be a place for brokers because of the personal touch, the thorough approach and the ease of what we offer. We are in a service industry and there will always be a place for that.

Reema: Also, with online and DIY loans, the customer speaks to someone different every time. Brokers come to know a lot about their customer over the course of the application – their work, family, dependants – and that’s where your word-of-mouth referrals come from.

When you build rapport, you become friends with clients. Sana: One thing I see frequently is clients calling me when they are about to change jobs, and they will say, “We’re looking to buy something in six months and I have been offered a better position with another company. This is the pay, but I’m a bit worried because I want to buy X. Can you run the figures for me and let me know?” So in a way we tell them yes, you can change jobs due to lender policies.

Because lending has tightened, it has now become a deciding factor for career opportunities, not just what kind of loan can I afford on this salary?

Reema: The services of a broker are comparable to those of a personal banker. Peter: Explaining to the customer that you aren’t affiliated to any lender also helps. A lot of people don’t understand the broker model, often questioning what our services cost them.

How can lenders with branch and broker distribution safeguard their broker partners against channel conflict?

Mark Brennan: At HSBC we’re about customer choice. The channel our customers choose to access their mortgage is largely determined by the service they get and the experience they have.

From our point of view, we don’t differentiate between channels, and we don’t want channel conflict. We have an established proprietary network, a call centre, and now we have brokers too.

The price we offer is available through each channel.

Sana: From a general industry view, when I first started broking the retail side was more protected, but now as the volumes are changing and brokers are driving more business to lenders, a lot of these conflicts are being smoothed over much quicker because the lenders realise the value of having brokers.

Alice Del Vecchio: It also helps that our broker support centre in Sydney acts like a virtual branch. That’s probably part of why the relationship between the channels we have works so well.

HSBC reduced its rates in 2018 at the same time that some of the majors were hiking theirs. What has this meant for market dynamics and competition?

Peter: The HSBC rates are unbeatable in the marketplace and the best on offer by far, so it’s a good product.

Reema: At the end of the day it is the customer’s choice which loan they take, but HSBC comes out on top every time because of their rate offers. I’m doing some good loan sizes, so customers want to fix their rates and the fixed rates are just as good.

Sana: Mix it with a low-value variable and no fees, or with the Premier pack for those that need it, and HSBC has become a great option for our customers.

Reema: I did an expo recently, and a lot of the people there were concerned about what the upcoming election would mean for rates.

They were asking me to show them the best rate for various outcomes, and when I did, they couldn’t believe the cost per month that was possible with HSBC.

It’s little things like that – the repayments, the ongoing cost of having the loan. Even if they have 27 years remaining, the HSBC rate is still lower.

For my clients it’s proven to be very competitive and often comes out on top.

Sana: Having non-major banks on our panel means the big banks need to work for the business they get, and consumers are the winners.

Peter: And when they can’t always compete on price they will give a rebate, or frequent flyer points. There is a major push on those soft benefits at the moment.

Reema: I see customers who aren’t interested in non-major banks from the outset, but I show them the figures and suddenly they can see the difference. With HSBC, the global presence gives them confidence.

Olivia: My customers are quite conservative when it comes to rates. They often have multiple direct debits and outgoings, so to come up with an attractive rate is a big advantage.

Additionally, many of my customers are expats or frequent business travellers, so they have heard of HSBC and have confidence in the brand.

Brennan, head of broker partnerships, HSBC Australia

Brennan, head of broker partnerships, HSBC AustraliaOften, I’ll do a comparison to demonstrate. For example, if you’re borrowing $100,000 to $200,000, the difference between five or 10 points is nominal, but if you’re talking $800,000 to $1m, that difference becomes huge.

As a product, it just makes sense, and it’s an easy application process, too.

How do HSBC’s BDMs support all of this?

Peter: When it comes to keeping brokers happy a good BDM makes a big difference.

They drive the business.

The BDM I work with is prompt, knows the business and how to source answers and is very proactive.

That’s what you want; when you are trying to grow a business that support is important.

Olivia: When things go wrong, it doesn’t matter who is actually at fault; in the eyes of the customer the broker gets the blame. So to have the support of a good BDM is brilliant. To have someone at the end of the phone, and to know you can get things done, makes a difference; just to be able to pull some strings and have support when you need something. Availability and assessment time are also important. People get excited, and they want their loan approved yesterday.

Sana: Having the assessors call you makes a difference, too. They quickly check an expense or a deposit, and the deal continues through the process. Some lenders are very protective of that direct contact with their assessors, so instead of a two-minute phone call it goes back in the queue and the process becomes longer.

Alice: As a brand, we pride ourselves on customer relationships and service.

From the partnership manager to the broker care team and the credit department, it’s all about how we make sure the customer is served. It was a conscious decision to recruit highly experienced people to our BDM roles.

We spent a lot of time recruiting and we interviewed a lot of people.

It’s really about overall credit knowledge, operations and end-to-end service, not just credit policy.

What traits did HSBC look for when recruiting its BDMs?

Alice: We looked for industry knowledge, and we believe that if someone is stepping into this role they need to understand what it’s like to be in the broker’s shoes, including the pressure and time constraints brokers work to. Experience, knowledge and being really good with people are all very important, and a good BDM also has to be firm but fair when required. If we really can’t do something or don’t have an appetite for it, they are encouraged to say that from the outset. They really go in hard to fight for the deal internally if they believe in it, and you may not always see that elsewhere. It’s a healthy conversation and it’s about the right decision and the right outcome. They know you, and they know the quality of the business being delivered.

Mark: A lot of people who applied for BDM roles wanted to be part of something new, and they demonstrated a great level of passion to be involved in HSBC’s journey. Another thing is that we look for people who can support the brokers. At the end of the day, brokers are running a business, and it’s about helping them to help their customers’ outcomes.

The broking industry is facing many changes at the moment. How should brokers continue to connect with their clients after settlement?

Olivia: It depends on the individual client. I deal with a lot of mums in my area, and they are very active on social media, so that’s one point of contact.

I also see them out and about, or our kids are at the same school, so we have a strong rapport there, too. Then there are the traditional follow-ups.

We always keep in contact to make sure they can’t get a better deal elsewhere.

“Experience, knowledge and being really good with people are all very important, and a good BDM also has to be firm but fair when required” Alice Del Vecchio, head of mortgages and third party distribution, HSBC Australia

Mark: Brokers play many roles, but one is to disseminate lender information to the community, and no level of branding, advertising or marketing could ever do that as effectively.

Regardless of what happens in terms of the industry, the rise in online lenders, or digital broker tools, there will always be an appetite from people who just want someone to hold their hand.

It all comes back to the original proposition: why do we have brokers? Because a lot of organisations have lost that personal element, and there was a gap in the market between the borrowing public and the lenders.

Reema: I like to educate my customers. I find that when you do that they really appreciate the difference a broker can bring, and they trust you. I explain the servicing rate; I show them the impact of adding an extra $500 per month to their repayments. When you take time to explain and demonstrate that you’re showing a bit of compassion, they connect with you and they know that you’re genuine and you want to help them.

Sana: It all feeds into how we generate repeat business. We keep in touch with their first loan, then after a few years when they have built up some equity, they come back and want to do it all again.