By

With the significant focus on household debt and regulators on a knife edge when it comes to the property market, brokers need to assert the critical role they play in the credit chain

The dramatically named ‘Liar Loans’ report from UBS is one more shot across the bow at the mortgage broking profession.

It’s not the first, nor will it be the last. It follows a line of scrutiny – and sometimes criticism – of the profession in recent times.

The ASIC Review of Mortgage Broker Remuneration was a major piece of the puzzle. It was the continuation of a review of all the players involved in providing credit. Alarmed by the high level of household debt Australians are carrying, ASIC decided to take a preemptive approach to regulation.

This is certainly better than responding to a crisis once the damage is done, as with the Future of Financial Advice reforms.

ASIC decided that it’s better to take the car in for a service and make small repairs, rather than wait for an engine failure on the side of the highway.

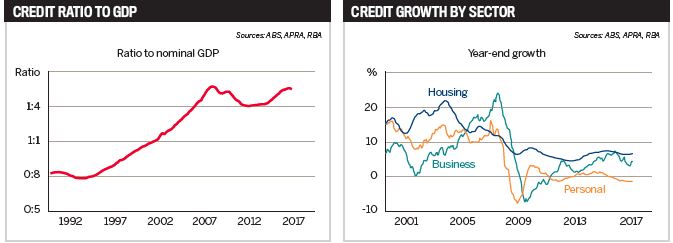

The level of household debt in Australia certainly warrants attention, but if we look at the numbers, credit growth has moderated in the housing sector.

As a ratio to GDP, credit is at historically high levels – more than 1:4. The explosion in credit pre-GFC saw housing debt balloon to an unprecedented size. Credit growth exceeded 20% in that era, whereas it now tracks at around 6–7%, albeit from a bigger base.

Victims of our own success?

In addition to the macroeconomic factors, the broking sector is attracting attention due to its success. A true alternative to the first-party lending model, brokers provide flexibility, choice and specialist credit skills and knowledge. Our remuneration models are disclosed and transparent, and our first responsibility is to the customer.

Customers like this, and that’s why brokers have captured more than half of the market. But like any sector facing disruption, some parties are nervous about change or have interests to protect.

Why detractors such as UBS are taking aim at the profession is not immediately apparent, but in any debate like this we should look carefully at the motives of those taking a stand – who owns what, and how competition affects their interests.

With household debt finely balanced, and regulators holding their breath in case any shocks hit the market, brokers are seen as a critical link in the chain because they help consumers access some of this debt.

So, our challenge – as aggregators and individual brokers – is to demonstrate that we take this responsibility seriously.

For Vow Financial and the Yellow Brick Road Group, there are two key planks to achieving this:

Individual brokers have a role to play too, by taking advantage of the tools that aggregators provide. In today’s market, processes and standards are always changing, so we need to invest time in staying up to date.

When I was teaching my daughters to drive, I noticed that some road rules had changed since I got my licence many moons ago. But there is nothing in place to keep drivers updated.

By contrast, our profession has plenty of channels to stay current. If everyone does this, and we have a high level of continuous learning, then the outcomes for our clients will be better.

Moreover, our profession will be able to refute these criticisms and know that our own houses are in order. It’s neither an easy nor a quick process, but it’s worth doing, and it’s what we are committed to achieving.