Our industry is on the cusp of radical change – not incremental or step change. Where we once disrupted the might and heft of the big banks, we’re now staring down the barrel of change ourselves. Let me be blunt: it’s a case of adapt or die. The best way to predict the future is to create it now. Don’t wait.

When brokers were the disruptors

When brokers were the disruptors

By way of an analogy, when brokers first emerged 30 years ago they were in a sense the ‘fintechs’ – or financial technology outfits – of that era. They were the new disruptors on the block. For those of you who’ve been around for a while, back in the 1980s brokers wore out a lot of shoe leather meeting face-to-face with clients. When they returned to the office to finish loan applications, they spent a good chunk of their day using the new-fangled fax machine that retired some of the former pen and paper working ways that saddled our industry with manual processes – the days when

Aussie and Wizard had a sizeable market share. Stay with me, Gen Y folks! A fax machine was a past tool of the trade that transferred documents by sending a signal down a telephone line to another receiving machine.

Will the new fintechs drive out existing players?

A new breed of digital disruptors is once again overhauling our home lending market – leapfrogging the computer era and catapulting us into the digital age, whether we like it or not. Put simply, those who fail to grasp how to use high-tech smarts to get closer to customers will quickly fail.

The fintechs are coming. They’re pushing forward fast and moving well ahead of the regulatory world. They disrupt quickly while legislation is belatedly changed. Much later. So it’s incumbent on us to better educate clients about the benefits ahead of this sea change. Now. Not in one year or 18 months and certainly not in three or five years’ time.

I tell all my mentees who we train through our learning academy to position themselves as trusted advisers – pivoting quickly and nimbly, second-guessing what homebuyers want. This agility has been our silver bullet for capturing about 60% of the total home lending market share to date. Quite simply, we do it better than the banks.

Once again, if we get the settings right by getting closer to our customers and embracing the latest tech know-how in the market, we’ll come out on top.

Worst-case scenario: loans through Amazon or Google

A classic example of the picture I’m painting here has been seen in the arrival of UBER. A few short years ago it was just a blip on the radar. When it burst out of the starting blocks onto our roads, no one knew how to deal with it.

Fintech aims to be consumer focused. On the one hand we all know that banking is moving into a new world. We know it will be different, but we’re not exactly sure what it will look like. On the other hand, the worst-case scenario is that Amazon or Google will offer loans in the next five years. This is why brokers have to understand that the world has changed, otherwise they’ll be out of business.

The good news is that electronic property transactions are now here. Let’s embrace the high-tech expertise this is promising. We know we can often close home sales faster and more efficiently than banks can. And let’s be honest, broking moved into the fintech space a few years ago now. But many brokers are nervous and don’t know what it means.

"We know we can often close home sales faster and more efficiently than banks can. And let’s be honest, broking moved into the fintech space a few years ago now." - Graeme Salt, director, Futurus Group

One way we can step up to this challenge is by explaining to homebuyers how technology is their best friend. Our customers are already using really cool toys at home with smartphones and tablets. They’re now demanding these high-tech innovations – it’s what they expect. The banks are increasingly realising that customers want more than to settle their properties using relic quill and ink methods that have held this industry back for so long.

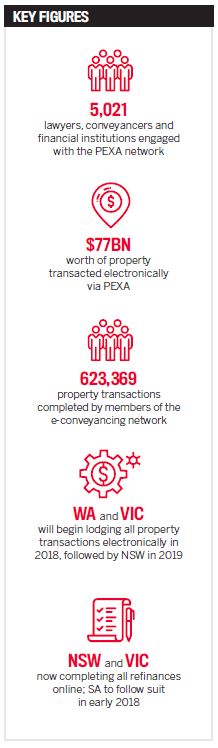

PEXA soon to hit milestone: $100bn in online transactions

If brokers haven’t heard about Property Exchange Australia – or PEXA – they need to quickly get up to speed with this innovation. Let me explain what I mean in the context of refinancing a mortgage. This is relevant as some commentators are forecasting that interest rates will move upwards in the near future, bringing more business our way.

In the past, the simple task of changing lenders took more than a month and involved cumbersome manual paper exchange in the back offices of mortgage lenders. Today, with PEXA, that all happens online, and the time from start to finish has been cut in half.

PEXA was launched a few years ago. It was a niche player then as the banks continued to muddle and slog their way through archaic paper transactions. Customers hated the delays that this imposed on them. In the course of the next few months, PEXA will pass its next milestone by transacting a massive $100bn worth of property online.

PEXA is changing the face of broking. It’s already here and can be used – harnessed – to get you closer to your clients. Brokers need to get on board or they’ll be left behind. If you’re a broker and can’t work in a PEXA environment, how will you work with paperless mortgages?

Rising interest rates – where we can really make a difference

The Futurus group of companies is increasingly seeing its property settlements finalised through PEXA now that the state governments are mandating electronic property transactions. Pin these deadlines on your office wall or put them in your calendar: In Western Australia, all property transactions will be lodged electronically from May 2018, followed by Victoria in October and NSW in June 2019. Refinances went digital in Victoria and NSW on 1 August this year.

My advice is, get to know what PEXA is all about. Get comfortable with it. There’s an app that PEXA offers lawyers and conveyancers called SettleMe, and we’re really excited by it. Through our training company, Walker & Miller, we explain that where brokers can really excel is in explaining to their clients exactly what happens during the settlement phase. I use the example of being a midwife who delivers our clients their dream home. The PEXA SettleMe app makes that happen. It’s a real-time tracking app that puts buyers and sellers in the picture so that they know at each stage exactly what’s happening as properties change hands. In the past when we settled through the banks we heard nothing. But with PEXA the end customer is fully in the picture all the way through the final home sale process.

Refinancing is a good note to finish on. Over the course of the next few years that’s where much of the broking business will come from. The commentators and market watchers are forecasting that interest rates will trend upwards in 2018. I predict at least one rise – and possibly two next year. That’s where we can really make a difference with our clients when they come to us asking for a better rate. Get comfortable with the uncomfortable now before it’s too late.

Graeme Salt is a director of the Futurus Group, which oversees a $60m monthly loan book through Origin Finance, Walker & Miller Training, Realestate.com.au Home Loans and Chan & Naylor Finance.