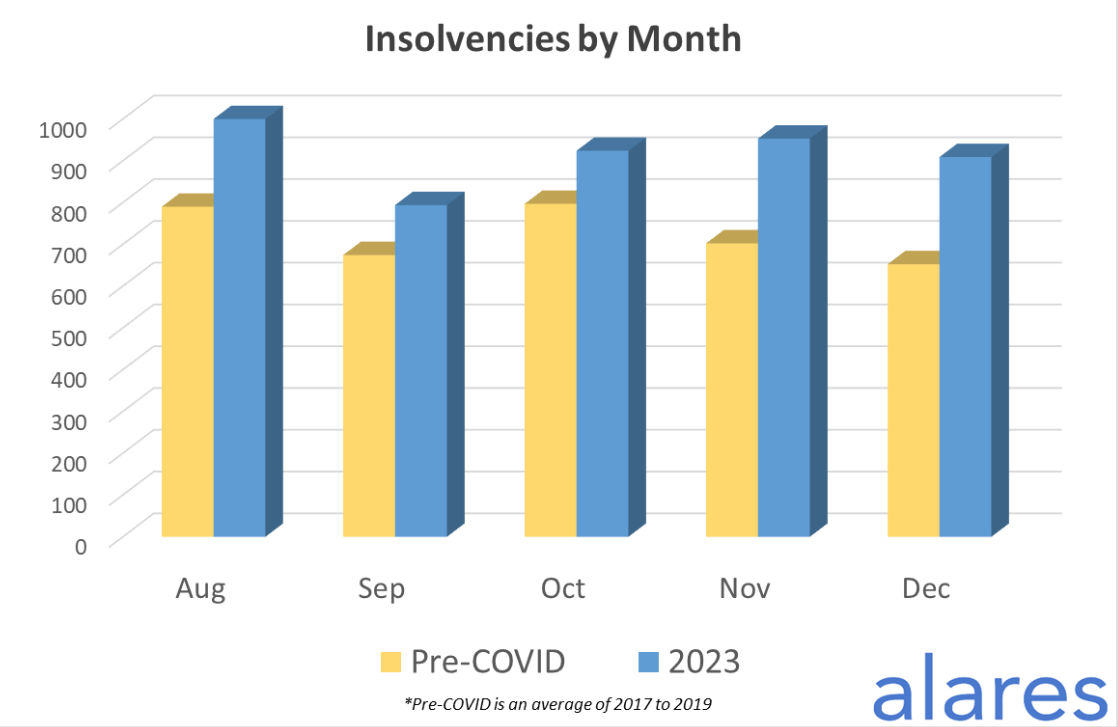

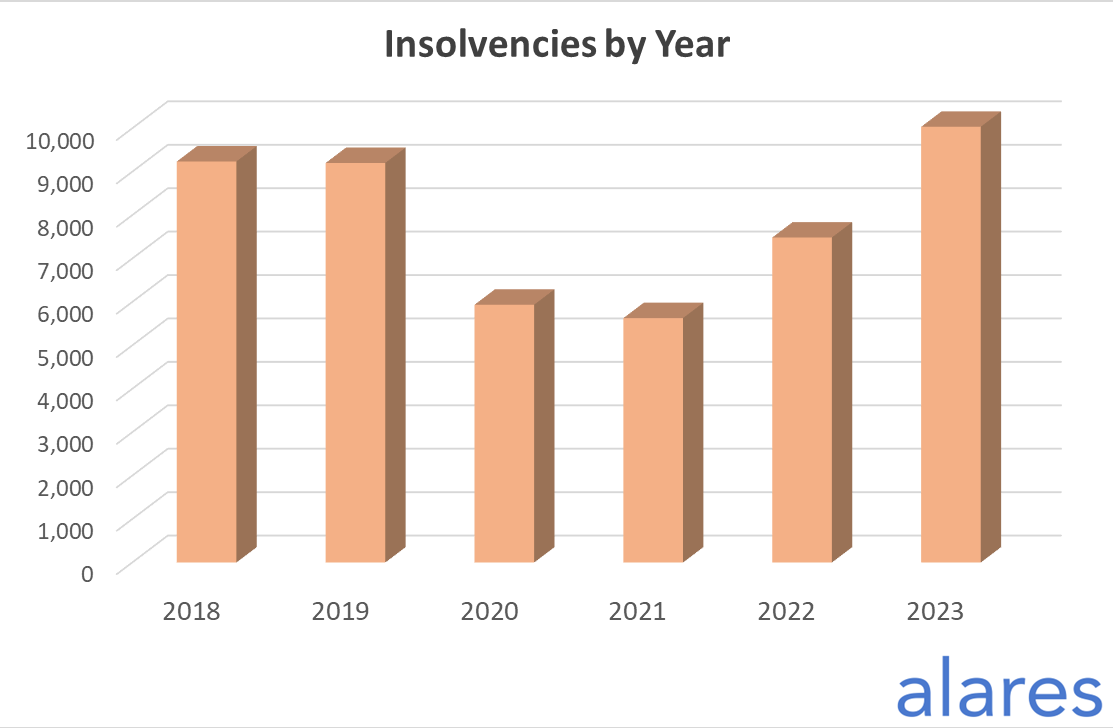

With insolvencies surging to 30% above pre-COVID levels, experts are advising business owners to proactively manage costs and financing while prioritising profit over margin squeeze to avoid a similar fate.

This advice follows the latest Alares Credit Risk Insights, revealing an increase in ATO tax debt recovery actions and court recoveries from major banks.

Andrew Spring (pictured above left), a partner with insolvency specialist Jirsch Sutherland, said too many businesses were being forced to chase sales instead of margins and “robbing the future to pay for the past”.

“This isn’t an uncommon pitfall for businesses, but the current market is forcing even experienced operators into making this mistake,” said Spring. “We often say that ‘chasing sales is vanity, chasing profit is sanity’.”

“However, in the current environment we know some business owners are feeling the pressure to maintain price points or even discount to maintain top line performance, while the costs of doing business continues to grow, strangling and suppressing their profit margin.”

Wayne Morris (pictured above right), CEO of small business lender Fifo Capital, said he had seen the same “misguided” pricing strategies lead to insolvencies.

“Some businesses, in an attempt to boost sales, offer discounts, but it's crucial to analyse how such decisions impact profitability,” said Morris. “A 10% discount might seem attractive for generating more business, but it's essential to consider how much additional sales are needed to compensate for the profit given away.”

Spring shared a case of an e-commerce retailer caught in a cycle of margin squeeze, leading to financial distress and voluntary administration. The struggle to play catch-up exacerbates the situation.

“The director has told me that he felt trapped in a cycle of loss-making decisions simply to keep the lights on. He couldn’t see the forest for the trees – and that’s when he knew he needed help.”

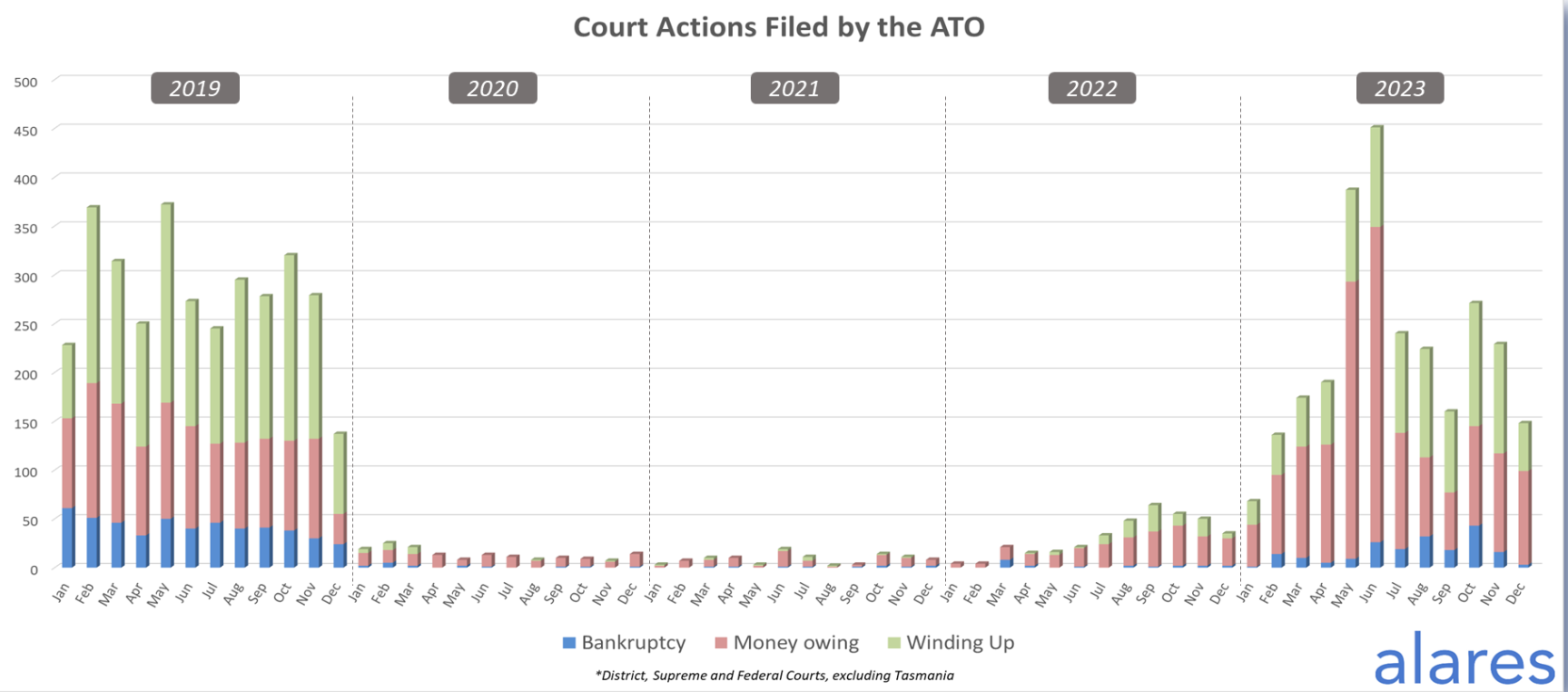

Tax debt also continues to loom large this year, with the ATO actively pursuing overdue tax debts.

This remains a “key challenge” for Australian businesses, according to Alares, after years of low ATO court activity between 2020-2022.

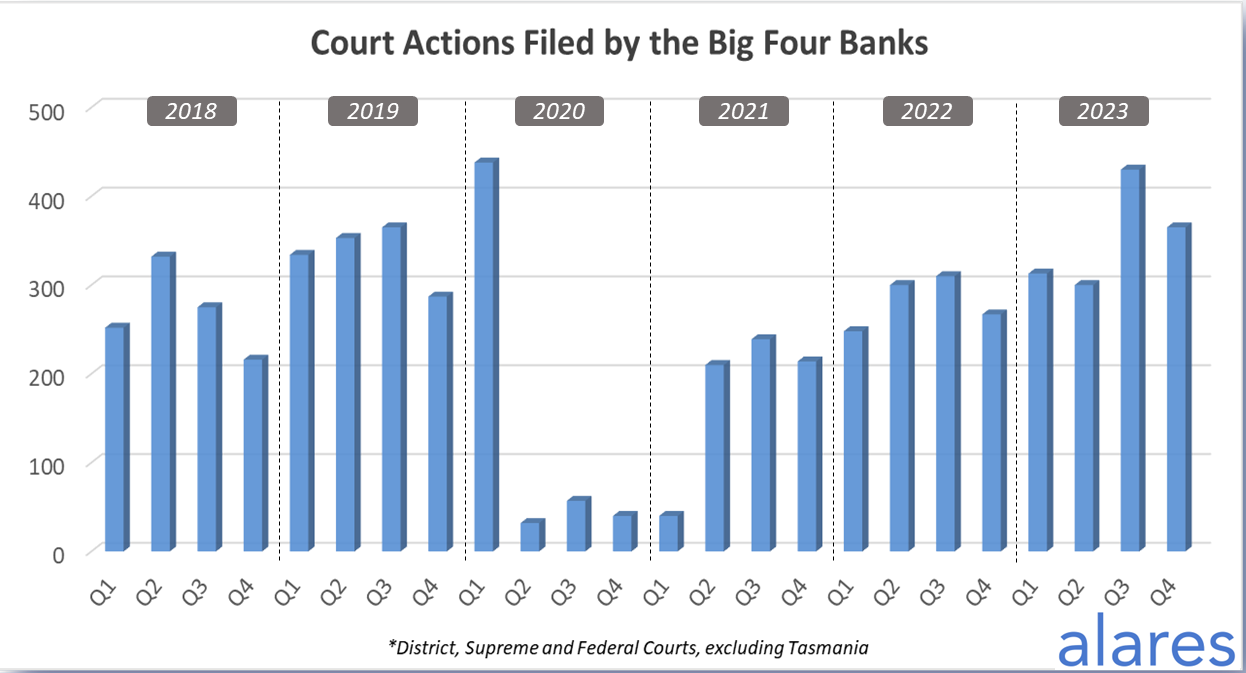

The big four banks are also continuing to ramp up their court recoveries.

The December quarter saw these actions above historical levels due to higher interest rates affecting loan serviceability, the Alares report showed. Meanwhile, both ATO and non ATO-initiated winding-up applications continued apace.

Patrick Schweizer, director of credit risk analytics company Alares, said while insolvencies in December were again well above pre-COVID levels, January was historically a low month for insolvencies.

“It won’t be until February or March before we get a clearer idea whether the trend from the end of 2023 continues into 2024,” said Schweizer.

However, Spring said the year had started “with a bang”.

“Usually, January is a quiet month due to the holiday season and court closures, but we’ve rolled into 2024 with insolvency enquiries and appointments coming thick and fast.”

Morris echoed these concerns about businesses ignoring issues pre-Christmas, leading to collapses even before the holidays.

“Many business owners that stuck their head in the sand in December face a reality check post-Christmas, realising they can't sustain their operations.”

Morris said payment terms for customers often tightened in January, leading to potential insolvency increases across our network during January and February.

“Outside the COVID era, January has consistently been a challenging period due to delayed payments,” he said. “For some, it becomes the tipping point where non-payment by customers leads to an inability to meet their own financial obligations. It's a somewhat typical scenario this time of year.”

“Additionally, factors like rising supply costs and interest rates are pushing businesses that were already on the edge over the brink.”

According to Morris, the situation for business owners will get worse before it gets better.

“With increased scrutiny from the ATO, tougher times are likely in the coming months. By the end of this financial year, I hope to see signs of improvement.

Compounding the problem, Morris said widespread insolvencies could also create a domino effect.

“Unfortunately, we've observed instances where extended terms and customer insolvencies led to the downfall of some clients last year,” Morris said. “It's undeniably going to be a period of challenging times ahead.”

In the realm of business resilience amid tough conditions, the role of working capital becomes paramount.

Morris shed light on how strategic financial approaches can help businesses steer clear of insolvency and the pitfalls of long-term business loans.

“I’m a massive advocate against businesses taking out business loans. For many time-poor SMEs, they have a problem today that they want to solve today, whether that be purchasing something or an ATO bill,” Morris said.

Instead, Morris said Fifo Capital encouraged their clients to steer clear of business loans and adopt a “more sophisticated and smart solution”.

“One approach we recommend is a method to accelerate payments in or decelerate payments out without disrupting relationships with customers and suppliers,” Morris said.

For example, if a business is struggling to get paid for an invoice, Fifo Capital offer financing for that specific invoice. “When your customer pays, you repay us,” Morris said.

“We monitor businesses closely and can confidently assess the likelihood of failure. This way, we can assure clients that certain businesses may be slow but won't collapse,” Morris said.

On the other hand, if suppliers need shorter terms, Fifo Capital will let them keep those terms, and extend it on their end.

“This continuous cycle allows businesses to remain profitable and manage their cost of capital effectively,” Morris said. Our approach ensures that businesses don't end up with a large lump sum that needs to be managed over an extended period.”

“It's always linked to the invoice, and when payment comes in, the finance is cleared, creating a sustainable business cycle. This approach helps businesses avoid surprises from unknown factors.”

As business landscapes evolve and challenges arise, seeking expert advice becomes essential for business owners looking to survive.

Spring has a word of advice for business owners in 2024: “Address any legacy debt positions in your business as soon as possible by seeking independent expert advice.”

“Some holes are too deep to fill, you need someone to throw you a rope to help you climb out,” Spring said.

Morris agreed, saying the role of commercial brokers and financial advisors had become increasingly imperative.

“Don't hesitate to reach out for assistance. If you find yourself in a tight spot, talk to your finance team. Let them know you need some help and breathing space,” Morris said, who also urged brokers and advisers to also be proactive.

“It’s the perfect opportunity for SME brokers and advisers to show true value by identifying the aspects of their business that can be addressed,” Morris said.

“Help them avoid making radical decisions like offering discounts without fully understanding the true cost. Take the time to assess their suppliers and explore alternatives. If needed, discuss the situation with us.

“We are not fair-weather friends at Fifo Capital. When times get tough, we are always here to help.”