The property boom shows no signs of slowing down, with national housing values growing at the fastest rate for 17 years. Australian Broker asked two brokers, a real estate agent and a buyer’s agent for their insights.

Across Australia, the residential property market is defying all expectations and recording astounding price rises.

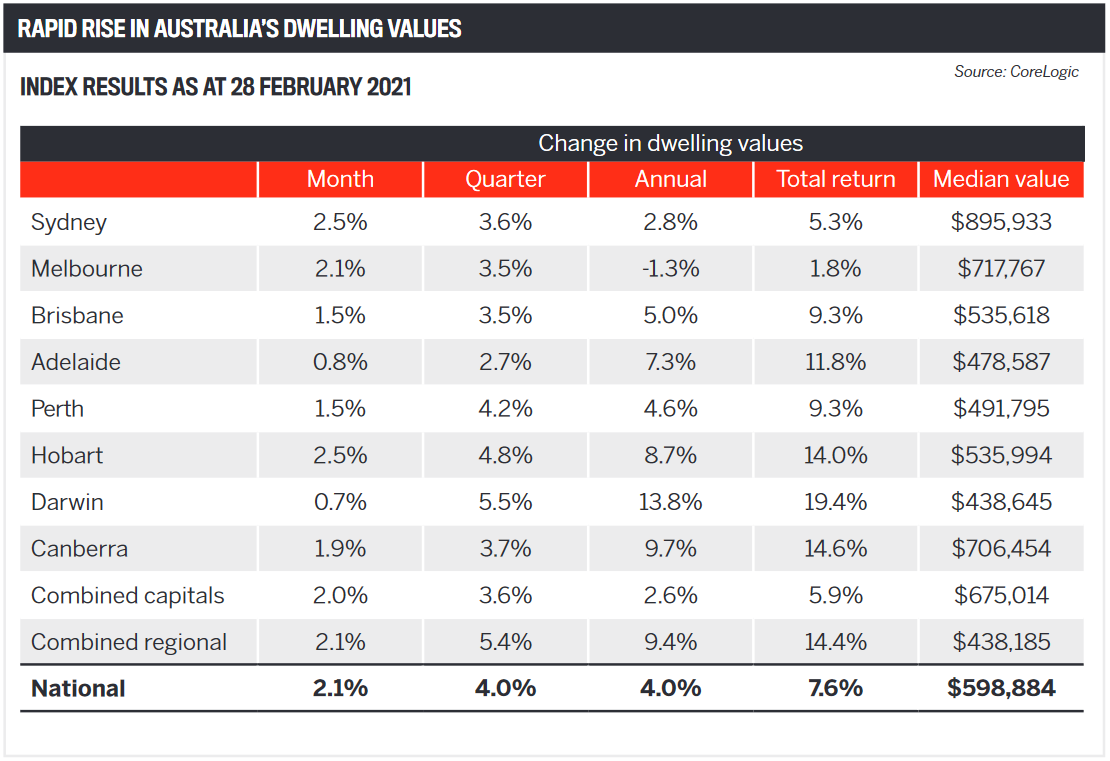

CoreLogic’s hedonic home value index shows values surged 2.1% nationally in February, the largest monthly change in the index since August 2003.

The real estate analytics company says the rise in housing values, which is occurring across all of the capital cities and regions, is being spurred on by record-low mortgage rates, improving economic conditions, government incentives and low housing supply levels.

The latest available CoreLogic figures, for the 28 days ending 4 April, show a monthly rise in housing values of 3.2% in Sydney and 2.1% in both Melbourne and Brisbane, as well as 1.4% in Adelaide and 1.6% in Perth. Even more incredible are the year-to-date increases, led by Sydney at 6.9% and Melbourne and Perth at 5.1%.

Australian Broker asked mortgage brokers Sofie Chapman of Buyers Choice in Sydney and Tom Uhlich of Brisbane’s Boss Money how the property boom was affecting them. McGrath real estate agent Simon Nolan and HighSpec Properties principal buyer’s agent Amanda Gould, both of Sydney, also shared their insights.

Sofie Chapman has been a broker for more than nine years but also has more than 22 years’ experience as a professional property investor and developer. She has a portfolio of 10 properties across Australia.

Sofie Chapman has been a broker for more than nine years but also has more than 22 years’ experience as a professional property investor and developer. She has a portfolio of 10 properties across Australia.

The Buyers Choice residential and commercial broker has offices in Sydney and Adelaide, with clients in both NSW and SA. She expects the house price increases to continue until at least October.

“Building approvals are at an all-time high, and the supply of materials such as timber is short,” says Chapman. “With the price of building set to go up 6% and not enough supply of established homes to meet the market demand, I believe the boom is sustainable for now. I think the slowdown will occur when people start travelling abroad and spending money overseas.”

Chapman says her broker business is busier than ever, and most of her applications are for pre-approval loans as customers want to be ready to make strong offers or bid at auction.

“Pre-approvals take time and have a lower conversion rate. Often the pre-approval lapses and we need to rewrite the entire application and go through the whole qualifying process again.

“There is a lot of time invested in writing applications, following up the client, assisting them with negotiation skills when making offers, and preparing property reports.”

Chapman says providing excellent customer service at every touchpoint is important to ensure loans are converted.

“Getting my processes tight and efficient has been a key focus during this boom season.”

In Sydney, low interest rates, cashed-up buyers, government incentives, pent-up buyer demand and a shortage of available housing have created the perfect mix to drive a booming property market, she says.

For brokers, the lack of housing stock on the market has been offset by refinances, renovations and new-home construction.

“I believe there is a great opportunity to focus on people wanting to renovate and refinance,” Chapman says. “I have clients who love where they live and don’t want to move. They are in a great position to borrow the funds needed to make their home a castle. There are also great refinance offers at the moment, and if it’s in your client’s best interest to do so they should consider refinancing.”

Regional Australia has experienced even higher property price growth than the capital cities, but Chapman says established city brokers should think twice about expanding into the regions.

“If you are going to expand to a regional area, be prepared for a lot of hard work networking. Regional customers tend to want to support local businesses, so if you are going to go into a regional area you should be prepared to go to the local football games, and support local initiatives, clubs and events. Unless you have a weekender in a regional area, I imagine it would a hard market to crack into.”

JobKeeper ended last month, but Chapman doesn’t believe it will affect the property market.

“If we were going to see an impact I think we would have seen it by now, with the media speculating doom and gloom with the ending of JobKeeper. Employment advertisements have increased strongly, indicating there are an increasing number of jobs available which will hopefully offset the removal of JobKeeper.”

Chapman predicts there will be a short-term cooling of the property market once Australia’s borders reopen to overseas travellers and Australians resume holidays abroad, but only until immigration picks up again.

Uhlich says he moved to Brisbane for a change of lifestyle and to run his own business.

“I started working for Aussie as a broker in 2004 and ended up having two franchises – Kenmore and Forest Lake. I sold them in 2015 and started Boss Money Mortgage Broking in 2016,” he says.

The property boom is having a positive effect on Boss Money.

“The last three months have been our biggest,” Uhlich says. “The enquiries are an interesting one, as all this hype and activity has brought out plenty of people who have FOMO but can’t really get into the market. Hence, enquiries to actual lodgement conversion is much lower than pre COVID.”

Uhlich says the data doesn’t really explain why the boom is happening, but he has own views.

“I think COVID gave people time, time to realise they don’t want to live in their home any more, time to realise they like their home but it needs some additions.

“More importantly, people who can now work from home going forward have thought to themselves, if I can work from home, why am I living in Sydney, Melbourne or even Brisbane? Why am I in a city when I can head up or down the coast or even go bush?

“We have seen 35% of our loans that fit this category. Looking at our business, we have our highest percentage of pre-approvals ever. So many buyers and so little houses have pushed prices north, way north.”

The conversion rate on pre-approvals isn’t high. Uhlich says 50% of people won’t buy anything.

“People go hard for four to six weeks then just fade away. And this market is so tough on buyers, I would get two to three calls per day from buyers saying they just missed out on this and that. Agents are telling me they have 50 groups through a property and 10 offers. My buyers are saying the same.”

In the last month, there’s been a push from buyers to opt for cash contracts with no finance clauses.

“Cash is really king now. Most agents are telling buyers that unless you offer cash you don’t stand a chance. It’s basically like buying at an auction; there’s no way of pulling out. If your finance is declined by the bank, you lose your deposit and could be sued by the seller.”

Uhlich says he recently sat down with three buyers and worked through their numbers as they wanted to offer cash, even though their loans were not approved.

“All three bought cash. I am lucky I have been a broker for 17 years as I know a deal, but still had to be sure so I ordered and paid for their credit files plus did desktop valuations on the properties they were interested in.”

The cash trend is also being driven by slow loan turnaround times.

“Some of the larger lenders are taking 20 days just to pick up an application, let alone approve it, so clients are having to make offers with no finance clause in the hope they are approved. I haven’t had a loan declined for two years, and given my 17 years’ experience I know if it’s a deal or not.

The lack of housing stock is also affecting Uhlich’s clients, whether they are buyers or sellers.

“We are at a crossroads in the market at the moment,” says Uhlich. “Plenty of buyers and a booming market normally would bring more sellers to the market, but my clients who are looking to sell (and buy) like the sell part but are scared to hit the market because they can see there isn’t much stock to buy, and even if there is, it’s going so quick. They fear selling and being homeless, plus rental vacancies are also so low. I would say a third of these have decided to take advantage of the HomeBuilder grant and renovate their home.”

Uhlich doesn’t believe the end of JobKeeper will have much impact, as most businesses are back to normal trade, but he is concerned about how small tourism, retail and food businesses will cope.

“I thought the mortgage deferrals may have forced people to sell, but they came and went in September, and now at the end of March there are only a very small percentage of people of repayment holidays. Low interest rates have also helped.”

“The other smoking gun is interest rates and lending restrictions. Rates will rise; it’s just a matter of when. The RBA is saying it won’t lift rates till 2024, but the markets have priced one into 2022. Watch this space.

“With lender restrictions, I see in New Zealand they have reduced the LVR on investment purchases to 70%, which has slowed their property somewhat. Maybe similar restrictions will happen here.”

Simon Nolan has more than 20 years’ experience as a real estate agent in Sydney’s eastern suburbs. He currently works at McGrath’s Maroubra office. The award-winning agent has racked up 950 sales totalling $900m.

Simon Nolan has more than 20 years’ experience as a real estate agent in Sydney’s eastern suburbs. He currently works at McGrath’s Maroubra office. The award-winning agent has racked up 950 sales totalling $900m.

He says recent home value increases of more than 3% in Sydney are impressive.“

Sometimes the media and other interest groups can latch on to and promote eye-catching figures that are more hype than reality. But not in this case,” Nolan says.

“I think statistics can often be playing catch-up with reality in any rapidly moving market, and this market we find ourselves in now is unlike any I have experienced in my 21 years as an agent.”

Nolan says the good prices and reasonable competition of December continued when his team started back in mid-January and flowed into February with a 90% auction clearance rate.

“At the time of writing we just had a ‘Super Saturday’, but even that larger stock level day resulted in yet another 90% clearance rate. These figures tell the story of a skyrocketing selling market.”

There are two submarkets – properties with land and properties without, Nolan says.

“Properties with land kept us uber busy, with most properties receiving hundreds of enquiries and 75 to 150 through the door in a typical campaign.”

However, he says apartments were more subdued, with numbers half those of houses.

“But now in early April we are already seeing buyers downshift as their aspirations of buying a property with land evaporate and they focus on apartments, which is helping the apartment market to gather speed too. There are numerous examples of spectacular prices being paid across the country, with some properties selling for 10% to 30% more than they would have achieved in most of 2020.”

Nolan says the rapidly rising price rises aren’t sustainable.

“I do believe there is room for further price growth but not at the current pace. All markets are cyclical, so either predictable or unforeseen factors will come into play and cool the market mania down. The big question is when.

“I do feel the market has reset at a new ‘normal’ level, and if history is any guide we will see a flattening of prices and a more stable market further ahead.”

Two of the “counter-intuitive” hallmarks of a hot selling market are off-market sales and seller hesitance to list, says Nolan.

“My team made four off-market sales in February and two in March, and the reason for choosing this approach was often similar: ‘If we could get X amount of dollars and not have to tidy up, pay for marketing/styling, avoid open for inspections and just be done with it, we’d sell’.

“In all cases, it was a very high price, but in all cases our buyer work produced the buyers who could deliver.”

Nolan says seller hesitance is down to one sticking point: “If we sell we then have to buy, and there’s nothing on the market”.

As for the boom in regional areas, he says the most noticeable movement for his clients has been unit sellers leaving Sydney and heading north, south and west for a house and land.

“But I have not seen many house owners doing this. Working from home seems here to stay, so house owners have more ability to modify their home to enable this.”

The end of JobKeeper and other support measures could negatively affect some employees or business owners who own property.

“It would be sad if that forced the sale of property, but if it did then it may lead to more selling stock, but it’s too early to say.”

Nolan says he has an active two-way referral relationship with a few mortgage brokers.

“I believe a good agent and a good mortgage broker can make a real difference when it comes to helping clients get what they want.

“I know that they will look out for the best interests of the people I refer and make me look good. I would assume the boom could potentially have brokers very ‘busy’ getting pre-approvals but possibly having to be selective to some extent with their time allocation to each client, as many will not win the bidding wars, and as we all know or learn the hard way, ‘busyness’ is not necessarily good business.”

Amanda Gould is director of HighSpec Properties Buyer’s Agents in Sydney. Its core areas are the Eastern Suburbs, the Inner West, the North Shore and the Northern Beaches.

Amanda Gould is director of HighSpec Properties Buyer’s Agents in Sydney. Its core areas are the Eastern Suburbs, the Inner West, the North Shore and the Northern Beaches.

“I started the business 10 years ago, but I have been buying properties since 1988, so I’ve got a really good cross-section of what’s been going on in the market, what’s happened in 2017 when we had a peak, and right across the board since the ’80s really.”

Gould says at present 70% of her clients are owner-occupier and 30% are investors.

“Last year we didn’t have many investors at all, but that doesn’t surprise me with COVID; it was more owner-occupiers.”

Client demand for property is really strong, says Gould.

“But the stocks are down 30% from last year, which is driving a lot of what’s happening. The fear of missing out is driving people to overspend way above the guides. The reason stock levels are down is that people are too scared to sell their house in case they can’t find another.”

There is a lack of housing stock across Sydney, but the work-from-home phenomenon is leading to more people wanting to upsize. Gould says.

“This is great for us because we’re getting more clients wanting to upsize, whether it’s a unit going from a one-bedroom to a two-bedroom, or a house going from a two- or three- to a five-bedroom.

“A lot of people are thinking ‘we’re going to need a designated area to work in’, so a lot of people are upsizing, which is great, but the lack of stock is still apparent, and it’s right across the city.”

Gould says affordability is at a record low, unlike last year during COVID when homes became slightly more affordable.

“A lot more first home buyers were able to get into the market during COVID – those that still had jobs of course. But we’ve found prices rising at two and a half per cent in February. If we look at extrapolating that out, it’s a significant increase over the year, and if they don’t buy in the next couple of months they’re going to be priced out again.”

Gould doesn’t see a rise in housing stock in the near future, and auctions are achieving record prices.

She says she went to a recent auction for an unrenovated home in Waverton on behalf of a client, and there were 19 registered bidders but only three actually made bids because the auction moved so quickly.

“It had already gone away over the guide where most people were obviously sitting, and they didn’t even get to bid.

“I ended up buying that for my client, which was great, but it was way above the guide,” says Gould. “But that’s why clients have got us on their side to give them a true indication of what’s happening in the market and what value a property is worth in this current market.”

Gould says if current price rises continue for the next few years, people in Sydney are going be paying $2m for a one-bedroom apartment.

“It’s actually got to level out, but it’s not happening any time soon unless the stock levels start rising in the immediate future.”

Fear of missing out on property is driving both buyers and sellers.

“The cash rate’s not moving, and experts are saying it’s forecast to stay like this till 2024. So people are saying another $100,000 really isn’t as much as it would have been a year ago. People justify going up a little bit just to get into where they want to be because the money is so cheap.”

The media plays a big part in the fear factor for property sellers, says Gould.

“People are hearing there’s hardly any properties so they won’t put theirs on the market, but what they’re not realising is that this is the best time to put it on the market because there’s barely any properties so they are going to get a record price.

“If they’re buying and selling in the same market, yes, OK, there’s less stock, but they’re already in the driver’s seat to able to get the best price and have more money to go buy the next place.

“This is the time to sell – that would be the message I’d be getting out there. Why are you hanging on? You can’t get better than this market to be selling.”

Record numbers of people are applying for home loans or refinancing, and Gould is urging her clients to use a broker so they can save thousands of dollars.

“We are very big supporters of the broking community; ever since I started the business, brokers have been my number one strategic partner and referral base.

“We refer a lot of business. Even if clients have bank finance we try to push them to a broker to help them really get an understanding of what other finance options they’ve got rather than just going to a bank.”

Buyers’ agents also speed up the process for buyers.

“The average buyer takes six months to a year to buy a house if they don’t have a buyer’s agent,” Gould says. “With us, we accelerate that process to four to 26 weeks, so it’s a massive difference in time frame.”

Tom Uhlich has been a mortgage broker for 17 years. He worked at

Tom Uhlich has been a mortgage broker for 17 years. He worked at