By

The scenario

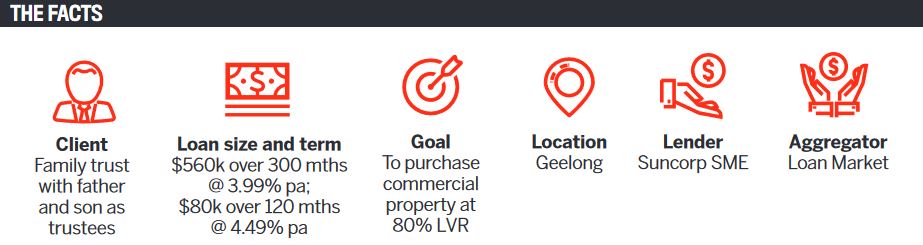

I had originally helped one of the two borrowers in this deal with his first home purchase nearly two years earlier; he had found me via my Google reviews. Subsequently, when he wanted to buy a commercial property, which his father’s business would be operated out of, he contacted me to see if I could assist. The goal was for the father and son to purchase the commercial property for $875,000, using an equity release from the son’s existing home to help fund the purchase.

Based on legal advice that the pair had sought out independently, the finance structure that they desired required a family trust to purchase the commercial property.

To add a little bit more complexity to the deal, we were aiming to complete and settle this transaction during COVID-19, as the developer had offered the borrowers a substantial rebate worth $75,000 for purchasing during the pandemic.

We required an 80% lend, based on the deposit of $175,000, which had been pooled by the father and son. The son’s portion was due to come out of the equity release from his home.

During normal lending conditions, this would have been quite a complex deal. However, because of all of the uncertainty driven by COVID-19, it became much more difficult as we saw some commercial lenders who were originally very active in the commercial space limit their LVRs – or in some cases pull out of the market completely.

The solution

We reviewed a number of different lenders in order to find the right fit for these borrowers’ particular circumstances. As each lender assesses income differently, it was a matter of finding a bank or lender that would take into account the particular requirements of this loan and the borrowers’ unique situation.

For instance, there were many lenders that wouldn’t look at the application because of the accumulated losses sitting in the balance sheet, even though the business had shown highly profitable trading over the previous three years.

Due to all of the uncertainty driven by COVID-19, the deal became much more difficult as we saw some commercial lenders ... limit their LVRs – or in some cases pull out of the market completely

We had also started the conversation about a commercial purchase and loan structure with this client prior to COVID-19. Back then, there were multiple options available, so initially it wasn’t a challenging placement.

When the situation changed and we were strategising a lending solution, we began talking to Suncorp and discovered that the client had the ability to borrow at up to 80% LVR on the commercial purchase.

The way Suncorp structures this type of transaction is to hedge its risks by splitting the loan into two loan terms with different terms and conditions: the 70% LVR loan was set up as one loan amount amortised over 25 years, while the remaining portion at 10% LVR was amortised over a much shorter term of 10 years.

We split the loan as follows:

Suncorp issued conditional approval within five days, and we are expecting the property to settle in late July.

The takeaways

Every bank and lender has its own unique policies and procedures, so no matter how complex the loan, the borrower’s situation or their ultimate end goal, there is always a way forward, even in the middle of a pandemic.

Originally, I had been advised that the maximum loan term for this transaction with Suncorp would be 10 years for the full loan amount. Having the ability to lean on an experienced commercial broker enabled me to challenge this and seek a policy exception based on the owner-occupied nature and loan size.

This resulted in a fantastic outcome for our borrowers and the bank, which now has a secure, low-risk and long-term customer in place, and proves just how valuable it can be to have a mortgage broker advocating for you rather than approaching the bank directly.

Nicola Tucker

Nicola Tucker

Director and finance broker

at Surf Coast Finance