COVID-19 may have battered the economy, but SMSFs have weathered the storm very well, according to lenders La Trobe Financial and Thinktank.

A combination of factors is driving demand for SMSFs, including a resilient property market, poor returns on cash deposits, the tax advantages of SMSFs, and the fact that if an SMSF loan default occurs all other fund assets are protected.

Cory Bannister, chief lending officer at La Trobe Financial, says many people are taking stock of their lives during the pandemic and re-evaluating their finances, particularly their super balances.

“Many Australians will be looking at their super returns and may question if they couldn’t do a better job. We believe this could lead to an increase in people setting up their own SMSF,” he says.

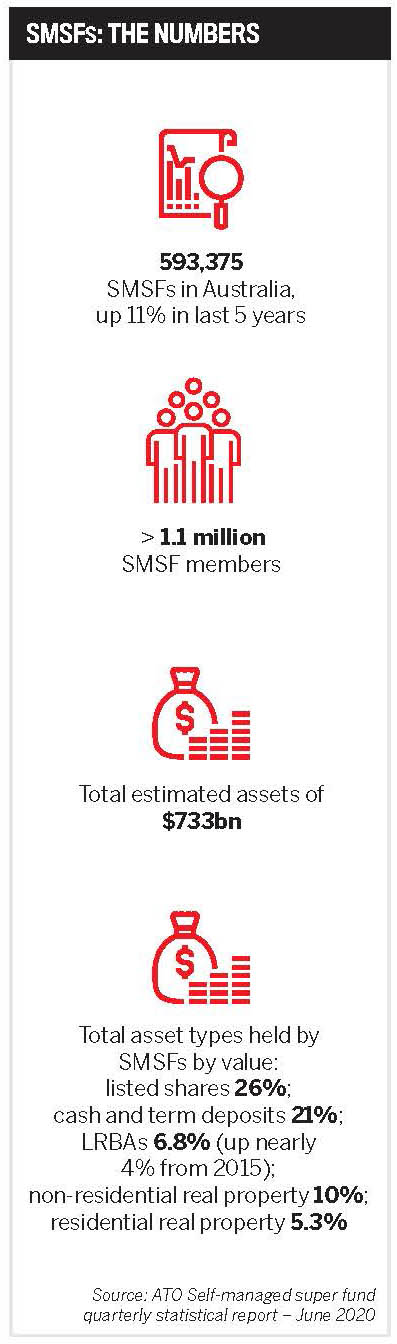

According to the ATO’s June 2020 figures, the number of SMSFs in Australia has increased 11% over the last five years.

Bannister says La Trobe Financial anticipates strong demand for light industrial property as e-commerce and data storage industries continue to grow, and for well-located suburban commercial properties to support workspace decentralisation.

“For residential assets ... we see potential for a growing demand for urban fringe property as buyers seek affordable family homes where they can work and live. These urban fringe areas have historically been very popular amongst SMSF investors.”

Per Amundsen, head of research at Thinktank, expects a continuation of the strong and increasing demand for SMSFs in the medium term.

Per Amundsen, head of research at Thinktank, expects a continuation of the strong and increasing demand for SMSFs in the medium term.

“With our leading experience in SMSF lending, Thinktank is well placed to help brokers take advantage of this expected demand,” he says.

The growth is largely driven by the lack of adequate yield-generating investments.

“With interest rates at record lows and dividends and distributions from listed securities falling, SMSF trustees are looking to alternatives in order to generate income.

“One such asset class is direct real property, and SMSFs provide a unique opportunity to make that sort of investment in the superannuation environment.”

“SMSF LRBAs are an excellent option for brokers to consider as they are one of the in-demand market segments in search of funding” Per Amundsen, head of research, Thinktank

Both La Trobe Financial and Thinktank are encouraging brokers to diversify into SMSFs via limited recourse borrowing arrangements (LRBAs), which allow borrowers to invest directly in residential or commercial property using funds accumulated in their super.

Amundsen says LRBAs are the only way SMSFs can borrow, and it must be for the purpose of acquiring a “single acquirable asset”, which is held in a separate trust (a bare trust).

Per Amundsen, head of research, Thinktank

Per Amundsen, head of research, Thinktank

“The key part, however, is in the name, being that the security relating to the loan only has limited recourse to the asset acquired by the SMSF and none of the other assets of the SMSF, so if things go wrong the superannuation savings apart from the ‘single acquirable asset’ are protected,” Amundsen says.

Bannister says LRBAs are a positive mechanism that enables consumers to accumulate wealth for their retirement.

“We expect the number of SMSF participants will continue to grow and pay dividends. Brokers should consider offering SMSF loan products as part of their overall diversification strategies, as they offer such significant growth potential.”

LRBAs provide a number of benefits, Bannister says.

“There may be some tax advantages, as interest and borrowing expenses are generally tax deductible, which can reduce the tax payable within the fund.”

They also allow SME owners to acquire or transfer their business premises into their SMSFs to take advantage of potential concessional tax benefits.

However, both Bannister and Amundsen recommend that licensed professional finance advice is sought prior to committing to an LRBA.

Amundsen says diversification is a great way for brokers to spread their risk profile and open up new growth opportunities.“That’s why SMSF LRBAs are an excellent option for brokers to consider as they are one of the in-demand market segments in search of funding,” he says. “At Thinktank we are highly experienced in helping brokers become accredited to write SMSF LRBAs.”Amundsen says Thinktank’s workshops provide an easy-to-follow, hands-on approach to ensure each broker is well prepared for the high level of compliance and discipline needed for SMSFs.

“Due to COVID these have more recently been run online, but we hope to be opening up the doors shortly to resume in person at our offices in North Sydney, Melbourne and Brisbane.”

La Trobe Financial also recommends brokers undertake training that covers the basics of SMSF lending, although it is not as complex as some think.

“Any broker who has done a trust loan will find that an SMSF loan is very similar – an LRBA simply involves a trust within a trust,” Bannister says. “A broker’s aggregator may also offer training and education, and it’s a good idea to partner with a lender like La Trobe Financial that offers direct access to credit staff willing to educate and assist brokers throughout the process.”

He says accountants and financial advisers are the best source of SMSF referrals for brokers, who can take comfort in knowing that the clients have been qualified and deemed appropriate to undertake borrowings under an SMSF structure.

Both lenders offer residential and commercial property LRBAs.

Thinktank’s move into residential SMSF lending is a natural extension for the business, designed to broaden its product offering from strictly commercial and meet the residential borrowing needs of SMEs and brokers, Amundsen says.

“It has been an easy transition, building on our existing strengths in commercial SMSF lending.”

Amundsen says residential property has great appeal – it is less complex and better understood by most people.

“It is interesting to note, however, that according to ATO statistics more money is invested in commercial property via SMSFs than residential property by a ratio of about two to one.

“Commercial property will remain an attractive proposition for SMSFs, particularly for self-employed people looking to acquire a site from which to operate their business” Cory Bannister, chief lending officer, La Trobe Financial

Cory Bannister, chief lending officer, La Trobe Financial

Cory Bannister, chief lending officer, La Trobe Financial

“Whether it’s residential or commercial, LRBAs present a unique opportunity for people to invest their superannuation savings in direct property as a tax-effective vehicle to build a nest egg for retirement.”

At La Trobe Financial, Bannister says many people are keen to use their super guarantee (SG) contributions to invest in something they understand better than the share market or managed investments.

“Purchasing a residential security in your SMSF is all about using the combination of rental income and SG contributions to result in owning the asset outright by the time you retire,” he says. “When it is sold during the retirement phase, the sale is capital gains tax free.

“Commercial property will remain an attractive proposition for SMSFs, particularly for self-employed people looking to acquire a site from which to operate their business.”

There is also a planned change in legislation governing SMSF trusts, which, if accepted by the Federal Parliament, would increase the maximum number of SMSF members allowed to six. The current limit is four.

Amundsen says there are several detailed legal issues, such as whether trustees will now have to be corporate rather than have the option to be individual trustees.

“Families beyond four members are often mentioned as potentially benefiting, and personally we can see business partnerships at the SME level perhaps finding this structure attractive,” he says.

“As contributions can now increase by up to 50%, we may see more partnerships forming new SMSFs as there is no limit to the number of funds one individual can be a member of.”

Bannister says the trust change will create an opportunity for intergenerational SMSFs and bigger loans.

“It will mean lenders will need to look carefully at servicing and how to ensure that a loan is going to be serviced with some members drawing a pension from the fund and some paying down a loan.”

For commercial SMSF loans, he says it could open up opportunities for multiple business partners, allowing them to increase SG contributions from most commonly $50,000 to potentially $150,000. For residential loans, it will increase the number of guarantors required.