In the digital age of instant gratification, consumers are demanding quick and easy access to loans, and their needs are being increasingly served by fintechs using the latest technology.

The coronavirus pandemic has certainly accelerated the rise of fintechs and the creation of sophisticated technology to provide a multitude of lending solutions.

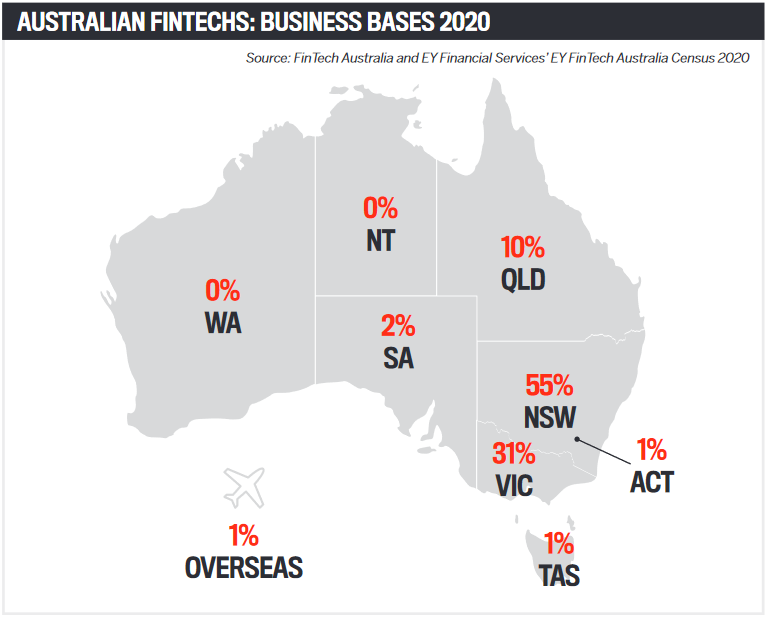

KPMG’s Fintech Landscape 2020 report released in December shows there are 733 active fintechs, up from 629 in September 2019. There has been particular growth in fintech lenders, especially those serving the consumer and SME markets, as well as neobanks. FinTech Australia, the peak body for fintechs, has released the EY FinTech Australia Census 2020 report, showing that fintech lenders and challenger/neobanks are on the rise.

The report, produced in conjunction with EY Financial Services, shows that lending makes up 29% of the sector, the second-biggest fintech type after payments, while challenger/neobanks comprise 14% of fintechs.There has also been strong investment in large scale-ups, including Athena Home Loans and Judo Bank, and ASX listings such as Plenti Group. More recently, there are plans to merge Lendi with Aussie Home Loans.

OnDeck

OnDeckCEO Cameron Poolman says OnDeck is highly focused on delivering rapid finance to small-to-medium enterprises and helping them reach their full potential.

“We know from OnDeck’s bespoke research that the SME market can be neglected by banks. As a result, one in four SMEs have been rejected by mainstream banks when it comes to securing commercial funding,” says Poolman. “Among those that do secure funding, the same proportion – one in four – face lengthy delays that have actually cost the business in terms of things like delivery of products or hiring new staff.”

Poolman says OnDeck, as a dedicated SME lender, is filling the gap with a truncated application process and rapid approval times.

SMEs have a strong reputation for embracing change, and this combined with COVID-19 is helping drive interest in fintechs such as OnDeck. The company’s own research shows growing awareness among SMEs of specialist online lenders such as OnDeck.

“They are eager to explore new lending options that cut red tape from the loan application process and deliver faster loan approval times and turbo-charged delivery of funds. The expression ‘time is money’ absolutely holds true for the SME sector,” Poolman says.

“They are eager to explore new lending options that cut red tape from the loan application process and deliver faster loan approval times and turbo-charged delivery of funds. The expression ‘time is money’ absolutely holds true for the SME sector,” Poolman says.

As a fintech, OnDeck takes a forward-looking approach to credit assessment, rather than the rear-vision view that traditional banks use, he says.

“This matters because it’s rare for SMEs to face exactly the same market conditions in the future as they have in the past. And never has our forward-looking approach been more relevant than during the pandemic, when SMEs have faced exceptional circumstances that are not indicative of normal trading conditions.”

There is an increasing level of competition among fintechs, but Poolman says there are factors that set OnDeck apart from newcomers.

“OnDeck has the combined benefit of proven technology and a wealth of customer data built up over many years of being in operation. Rather than basing lending decisions on past business results, OnDeck is harnessing the power of our data to assess the credit risk that a business poses.”

The lender uses its proprietary credit scoring methodology – OnDeck Score® – drawing on thousands of data points to identify the financial health of a business based on cash flow, credit history and various business attributes. “This is a significant competitive advantage for OnDeck as it allows us to provide timely finance offers, often in just a couple of hours, that are within an SME’s capacity to repay.”

OnDeck’s “high-tech, high-touch” approach provides a team of skilled BDMs to help SME customers and brokers, Poolman says.

“Brokers love the fact that when they partner with OnDeck they benefit from the support of a dedicated BDM who is specifically trained to be part of our broker team. This training includes time working as a loans specialist in our direct channels to better understand our products, processes and credit decisioning.”

Poolman is encouraging brokers to consider OnDeck as a fintech solution for their SME clients, with in-house research showing that 50% of SMEs turn to a broker for their capital requirements.

“We don’t ask our customers for any upfront security on loans up to $250,000, so SMEs don’t have to nominate a house or another asset as security – we just ask for a director’s guarantee.”

OnDeck’s average loan size is double that of its nearest competitor, says Poolman.

“We’re able to do this because as a fintech we make smart use of data and modelling rather than relying on backward-looking financials. Our products are tailored to SME needs, and for us, transparency is the key feature that builds trust. We’re about clear and fair finance with no surprises, so neither brokers nor their customers will encounter any hidden fees or charges in our small print.”

The SME lender also champions the use of the SMARTBox loan comparison tool, which allows brokers and clients to understand the true cost of business finance, while brokers and SMEs are also encouraged to use OnDeck’s business credit score calculator, Know Your Customer.

OnDeck’s fast and efficient application process involves a one-page form and a maximum of six months of bank statements.

Poolman says fintechs have shown that the traditional, paperwork-heavy approach of mainstream banks is highly outdated in today’s digital world. As a founding member of FinTech Australia, OnDeck will continue to be part of a collective voice on industry developments such as open banking.

“Broadly speaking, fintechs are demonstrating that there is an easier, faster and more streamlined way to deliver the funds SMEs need to seize business opportunities,” says Poolman. “Collectively, we are making intelligent use of data to assess the credit risk a business poses. This has paved the way for bank lenders to rethink their SME lending processes, particularly against the backdrop of open banking.”

CarClarity

CarClarity CarClarity can be thought of as a fintech brokerage but for car loans, rather than residential homes or commercial lending. The Sydney-based business was established in March 2020 and has already grown from five staff to 15.

Founder Zaheer Jappie says CarClarity provides a simple-to-use platform that connects borrowers with more than 30 different car finance lenders.

“It matches each customer with lenders based on the optimal price and loan terms for that individual’s needs,” he says. “Once the best borrowing option is chosen, borrowers are guided through an online application process to secure their financing. We operate as a broker function but focus on the digital customer experience and have smart integrations.”

Consumer expectations of fast results are helping fintechs such as CarClarity make inroads into the lending market.

“We now buy everything online, and everything is instant. This customer expectation has moved to financial services, and each year different financial products start to innovate more. We are leading this innovation in Australia for car lending and giving customers an online, instant and transparent experience in car financing.”

Jappie says there are three factors that set CarClarity apart from its fintech competitors.

“Our first thing is our people. We believe we have built a strong, experienced team and all share the same values in our customer obsession.

“Our second thing is our overall customer experience. We want to ensure customers start digital and obtain 90% of what they need online and then speak to an experienced adviser to make an informed decision on car financing.

“Thirdly, we invest heavily in innovative technology and are leading the charge in fast, reliable and transparent car financing solutions that are transforming the way Australians shop for and finance cars.”

The COVID-19 pandemic was unexpected and unfortunate but has created opportunities in car financing and purchasing, Jappie says. “It has favoured a more online digital approach, which puts CarClarity in a great position.

“Due to travel restrictions and social distancing laws, we have seen an increase in private sales, particularly of larger four-wheel drives, with customers doing more local travel and camping. Our demand actually went up as people focused on near-new used cars as new-car stock intake dropped due to COVID.”

With tech evolving there is also more data available from industry sources to help make data-driven products accessible to customers.

“Open banking will open a lot of doors, but we still rely on larger institutions to improve their technology stack/APIs [application programming interfaces],” Jappie says.

Technology has already changed since CarClarity began a year ago, and new innovations are on their way.

“We are always working on simplifying the opaque process that is applying for car finance, and had multi-variations over the last year,” Jappie says.

“In terms of what’s to come, we are implementing digital ID/biometrics validation and integrating an open banking platform to assist customers in completing an online application. We are also launching a dealer finance solution to assist with regulatory changes towards the end of the year.”

Jappie says CarClarity is pro open banking.

“Our financial health does mostly sit within our bank accounts, and utilising this data for finance applications will make it simple for customers to obtain, move and grow their financial needs with ease.

“This will allow smaller institutions like CarClarity to compete with large incumbents because we will have a very big picture of the customer’s financial position.”

“This will allow smaller institutions like CarClarity to compete with large incumbents because we will have a very big picture of the customer’s financial position.”

There are plenty of reasons why brokers should use CarClarity.

“Our ambitions are to provide tools for anyone. CarClarity’s platform is partner-friendly, and if a non-asset-finance broker has a client we would happily assist,” Jappie says.

“I think we are bringing more awareness to customers about brokers. We have a very firm stance on the disadvantages of not going to a broker, which we advise the customer on. Our main goal is seeing a customer get the right information to make an informed decision, whether with us or with another broker.”

The fintech sector is growing in Australia, Jappie says.

“We will see a lot of players locally become global businesses as there is more venture capital flowing into Australia. However, there will be a huge shortage of tech talent due to COVID and visa implications.

“Globally, more and more fintechs are becoming bigger than traditional incumbents, and in 2020 alone we saw a lot of public listing activity.”

ANZ

ANZBig four bank ANZ has been using the latest digital technology to simplify its home loan process. Simone Tilley, general manager retail broker, says the two key technological tools the lender delivered in the early days of the pandemic were ANZ eSign and ANZ eVerify. These were designed to support ANZ brokers and customers with simple, digital approaches to managing their identification and signing requirements, endeavouring to save time and paper.

“And in September we launched Illion Access Seeker to enable all ANZ brokers to undertake credit checks on customers,” Tilley says.

ANZ eVerify is focused on a digital ID process for the bank’s home loan customers satisfying Know Your Customer and verification of identity requirements electronically.

“This seeks to significantly reduce the need for most customers to attend an ANZ branch, which saves them time and is convenient,” Tilley says.

ANZ eSign is a customer-focused digital signature and document execution process. It has been enabled in LoanApp and ApplyOnline to save significant time for both brokers and customers.

“With more of everyday life becoming digital, we are striving to continually provide helpful, easy-to-use and convenient solutions.”

Illion Access Seeker is a free service for all ANZ brokers. Brokers are able to credit-check customers and are provided with a report of a consumer’s comprehensive credit history information that is fully aligned with ANZ’s credit assessment process.

Tilley says the bank offers a range of training resources and support for its broker partners who wish to use these tools, including a broker portal that has content and process guides.

“The absolute backbone of our support is formed by our award-winning national BDM team. We also run both a fortnightly broker webinar series and a point-in-time update via webinar and BDM.”

As well as offering eVerify, eSign and Illion Access Seeker, ANZ is also building its broker operations team in size and capability.

“This is to improve our application assessment times and protect our SLAs across all channels,” Tilley says.

When it comes to future tech developments in the mortgage space, she says ANZ expects to see continued automation across the industry, for the benefit of lenders as well as brokers and aggregators.

“[We’re] using data and analytics to reduce the number of steps we ask brokers and assessors to complete to improve our time to first decision and significantly reduce rework, shortening our time to final decision, and to better understand our customers to ensure we are providing good outcomes for brokers and customers.”

Tilley says ANZ is hoping for a return to “a bit more stability and normalcy following COVID”.

“In ANZ Broker, our plan is to focus on the continuation of our automation and digitisation agenda to enhance our home loan processes so we can provide a smoother experience for customers and brokers.”

Over the next 18 months, ANZ also wants to continue to support the professionalisation of the broking industry by delivering a first-class education and training program for brokers and bankers, Tilley says.

“And of course data – we’ll continue to lead with data and insights so we can share data that is both quantitative and qualitative in nature.”

FinTech Australia

FinTech AustraliaThe peak body for fintechs has more than 300 members, a big leap from the 50 members it had when it launched in 2016.

Measuring the growth of the fintech ecosystem has been a focus of FinTech Australia, says CEO Rebecca Schot-Guppy.

“We know the sector is growing ... however, counting the precise total number of companies in Australia is difficult. Many of these studies are self-reporting, and founders are incredibly busy people. Others rely on the business needing to raise funds before being counted as an active company,” she says.

But thanks to the EY Fintech Census 2020, the group has a sense of the sector’s maturity.

“More than 78% of companies in it are post-revenue, and the majority, 61%, have been in business for over three years,” Schot-Guppy says.

There are plenty of good reasons why fintechs are having such an impact on residential, personal and commercial lending.

“Fintechs are incredibly customer-centric,” Schot-Guppy says. “Products are only launched where there is demand. Many fintech founders are former bank or financial services company employees. In their roles, they spotted ways that their company could improve their service and have ported this experience to their own company.”

She says home loan lending plays a huge role in Australian culture, and the sector has a history of disruption, with companies like Aussie and Wizard leading the charge.

“The difference now is that new innovations are being driven by new technology. Fintechs are finding ways to operate on leaner margins and provide superior customer service while still being fully compliant lenders.”

While COVID-19 has driven changes in technology, Schot-Guppy argues that for fintech lenders change has happened in spite of the pandemic rather than as a result of it.

“The biggest technological advancement we saw last year for the sector was the introduction of open banking. This could have easily been delayed due to the global pandemic but was pushed through by the government. Services harnessing open banking in lending are being developed as we speak.”

Open banking will bring a huge shift to the lending sector.

“Consumers often sit on a loan and don’t refinance due to the hassle of it. Open banking, however, promises to make this process as simple as clicking a few buttons. It’s going to make the sector hyper-competitive.

“Admittedly, change due to open banking will be slow, but I believe we’ll start to see signs of it this year,” Schot-Guppy says.

Consolidation is already occurring among neobanks, for example with NAB moving to acquire 86 400, but she says this will strengthen the remaining neobanks, and the same trend has happened in the UK.

Fintechs are also putting pressure on traditional banks to improve their services and rates by educating Australians on how to find better deals for their loans. Athena Home Loans is one example.

“For years, major banks have tried to build their brand around being a life partner for the consumer, supporting them on their journey to buy a house and then retire. There are countless ads depicting this,” Schot-Guppy says. “Athena, however, ran a counter-message as an advertising campaign: Take out a loan with us, and it’s our goal to help you shed your debt as quickly as possible. Love us and leave us.”

She says fintechs are changing the dynamic of lending and using technology and innovation to back up that shift. “That education piece is crucial and is what is ultimately leading to better competition for consumers and also a more robust sector.”

There are also actions the government could take to create a stronger, more competitive fintech market. Schot-Guppy says last year it introduced a Term Funding Facility giving ADIs access to the cheapest debt on record.

“The effect of this is the big four banks have been able to draw down on this and give fixed loans at rates that non-bank lenders or smaller ADIs can’t compete with. To maintain competition in the sector, we recommend the government allow greater access to the AOFM funding facility to allow fintechs to compete on rates.”

FinTech Australia is also calling on the government to better standardise the discharge process for loans in anticipation of further competition, and to waive discharge fees.