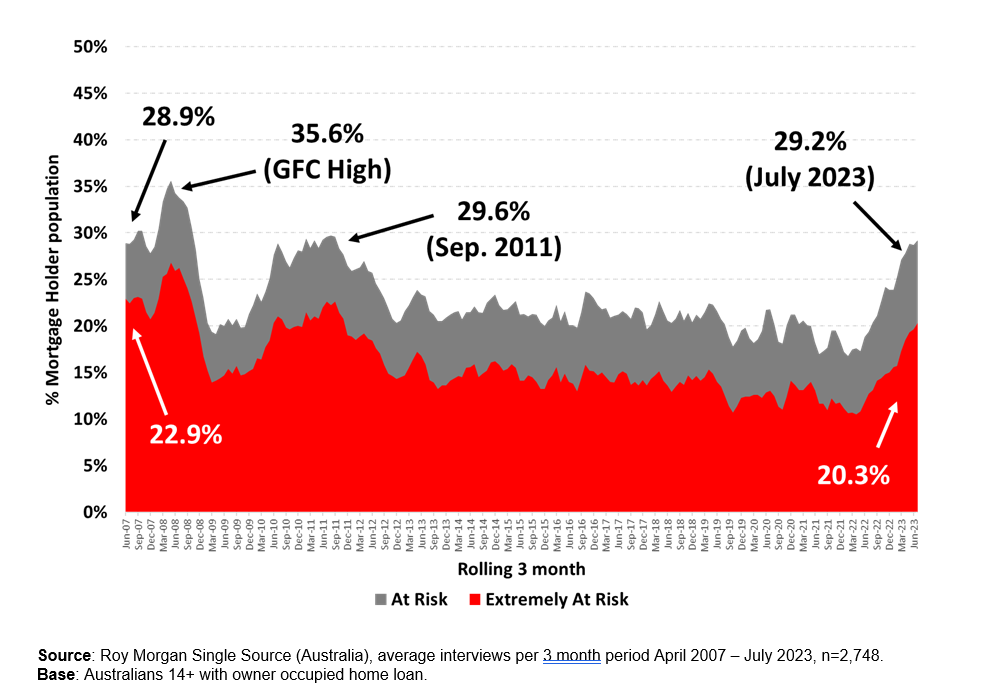

A record 1.5 million Australian home loan borrowers are now “at risk” of mortgage stress in the three months to July, representing 29.2% of mortgage holders, as the Reserve Bank’s interest rate increases early this year flowed through to the wider mortgage market, new research from Roy Morgan has revealed.

The July figures – which were the highest since May 2008, when there were 1.46 million mortgage holders “at risk – covered a period of two interest rate increases of 0.25%, taking the OCR to 4.1% in June.

After a year of aggressive interest rate hikes, 12 times in the last 15-monthly meetings, the number of households at risk of mortgage stress increased by 642,000.

“The latest figures on mortgage stress show that rising interest rates are causing a large increase in the number of mortgage holders considered ‘at risk’ and further increases will spike these numbers even further,” said Michele Levine (pictured above), CEO Roy Morgan.

“If there is a sharp rise in unemployment, mortgage stress is set to increase towards the record high of 35.6% of mortgage holders considered ‘at risk’ in May 2008 during the GFC.”

Even though the number of Australians at risk of mortgage stress was at a record high, given that the size of the Australian mortgage market today was larger, the proportion of 29.2% remained well below the record highs reached during the Global Financial Crisis of 10 to 15 years ago. In mid-2008, mortgage holders in mortgage stress hit a record high of 35.6%.

More concerning was that the number of mortgage holders considered “extremely at risk,” which has now surged to 1,017,000 (20.3%), significantly above the long-term average over the last 15 years of 15.4%. This was an increase of more than 470,000 mortgage holders from a year ago (+7.6% points).

Roy Morgan said mortgage holders are considered “at risk” if their mortgage repayments were greater than a certain percentage of household income – depending on income and spending. They are considered “extremely at risk,” on the other hand, if even the “interest only” is over a certain proportion of household income.

Mortgage Stress – Owner-Occupied Mortgage-Holders

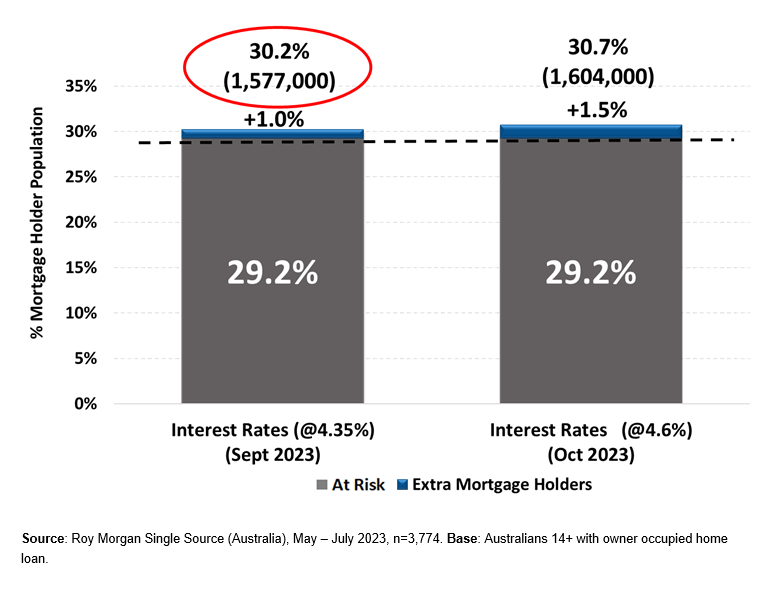

Roy Morgan has modelled the impact of two potential RBA hikes of +0.25% in both September (+0.25% to 4.35%) and October (+0.25% to 4.6%).

From the 29.2% of mortgage holders (1,496,000) “at risk” in July, this was forecast to increase to 30.2% by September if RBA lifts interest rates by +0.25% next month to 4.35%. That’s 1,577,000 mortgage holders considered “at risk” – an increase of 81,000.

Another +0.25% interest rate rise in October to 4.6% would likely raise mortgage stress to 30.7% (up 1.5% points) of mortgage holders, or 1,604,000 considered “at risk” – an increase of 108,000.

Mortgage Risk at different level of interest rate increases in September & October 2023

Despite the spotlight on interest rates, Roy Morgan said it’s an individual, or household’s, ability to pay their mortgage that has the greatest impact on mortgage stress.

“When considering the data on mortgage stress it is always important to appreciate [that] interest rates are only one of the variables that determines whether a mortgage holder is considered ‘at risk,’” Levine said. “The variable that has the largest impact on whether a borrower falls into the ‘At Risk’ category is related to household income – which is directly related to employment.”

Roy Morgan estimated unemployment to show a monthly decline but nearly one-in-five Australian workers were either unemployed or under-employed – 2,815,000 (18.6% of the workforce).

Use the comment section below to tell us how you felt about this.