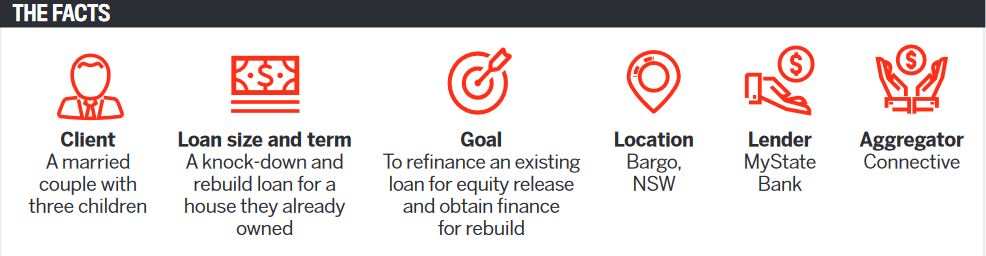

The scenario

I had previously helped this couple finance the purchase of their property many years earlier. They already owned the property and had a mortgage against it, which we had originally assisted with.

When they contacted me again, the husband had recently changed jobs and his income had increased by $60,000. They were hoping to obtain a knock-down, rebuild, refinance and construction loan. At the time of the application, he was still on probation in his new job – and that was the first of many hurdles to overcome.

The client lives in Bargo in NSW but works in Queensland in a fly-in, fly-out role as a technician in the energy industry. He flies up for three weeks, stays on site and works, then comes home and has the week off. During that week off, his income is zero. This was the second part to the complexity of this deal.

Every fourth week, the client’s payslip was empty. To get around this, we created a spreadsheet covering three months’ worth of income to get an average weekly figure.

Before submitting the loan application, I did some research on land values, because once you knock a house down you’re basing the property’s value on the land value only. The value came in a little lower than expected, but it was still good enough to avoid LMI, based on the clients’ financials.

The solution

We sent off a number of emails about these borrowers to various BDMs for consideration.

One particular lender said it would consider the deal. We prepared all the paperwork, sent off the application, and then heard back – they said they wouldn’t look at it. When I got a hold of the credit officer for more information, he said the empty payslips every four weeks were a big concern.

The other concern was the fact that the application relied on the client’s income from overtime, which was a condition of employment. As his income had increased by over $60,000 since his previous job, the credit officer said he could see that the client would earn the money, but as he was still on probation the lender was not willing to consider the application at that time.

This happened even though we had checked this beforehand with the BDM.

The client asked: ‘Can we knock the house down?’ I came back with a resounding ‘No! Not until we have an approval!’

We withdrew the application and went to another lender. When I approached this second lender, the BDM said it all looked good and they were happy to consider the loan. And as far as I knew they had confirmed this with their credit team.

But the same thing happened again!

At this point, timing was becoming crucial. The borrowers had negotiated a very competitive contract with their builder, but the agreement was that if they didn’t get started by a certain date, the price would go up $30,000.

We were running out of options. The deal we had prepared was based on an LVR of just under 80%; however, it was looking like we might have to go to over 80% just to get the deal done.

There was pressure from all ends, with the builder threatening to put the price up and the clients having already booked in the demolition of the property. The client asked me: “Can we knock the house down?” I came back with a resounding “No! Not until we have an approval!”

I then approached a third lender. This time, when I sent in the details, it was like writing I my email was so long – but I needed to ensure every aspect of the deal was explained. We submitted the application, and it was approved! We got it in at 79% LVR, just narrowly avoiding LMI.

It had been a bit of a journey, and the client was very stressed along the way, particularly when he was in Brisbane and his wife was in NSW.

But with the deal approved, their existing house was demolished, they moved into a rental, and the new construction got underway. And that’s when we ran into a bit of trouble again: at the third drawdown, the lender wouldn’t approve the release of funds, citing a shortfall in funds. At this stage the loan was sitting at just under 80%, but the lender’s policy was that at this particular drawdown stage, the client couldn’t exceed a certain LVR.

Fortunately, the borrowers had cash reserves and were able to contribute the funds, knowing they would get the money back at the end when the last part of the loan was drawn down. Finally, the loan settled on time.

The takeaway

My approach to every loan and client is that it’s all about reverse engineering. I first consider what the client wants, then we can then work backwards to help them achieve that goal. If this is where you want to be and this is where you are right now, and these are all the moving parts, then what do we need to do to make it happen?

I always tell my clients: “I’m pretty sure this is going to work, but if it doesn’t, here is Plan B and C. In every deal, I’m always thinking of where else I can go and what I can do next. The last thing I ever want to say is, “It can’t happen”. Hopefully it works on the first attempt, but that’s not always the case.

Alex Sperling

Alex Sperling

MFAA-accredited finance broker,

Our Mortgage Options