Ashleigh Aulsebrook and Richard Aulsebrook of Melbourne brokerage Morgan Brooks outline how they saved the day for an older couple who had contracted to purchase a warehouse and found their financial approvals had been denied.

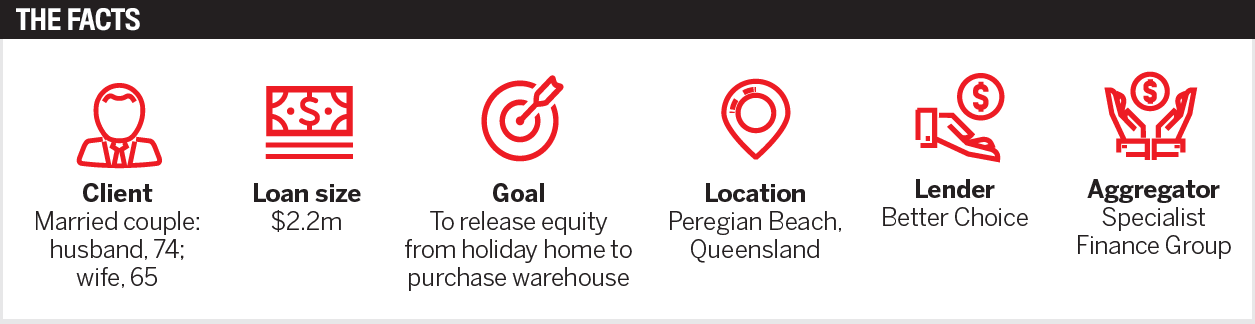

Last year, we were introduced to a delightful older couple who had unconditionally contracted to purchase a warehouse in order to expand the wife’s business premises from what she currently owned to an adjoining warehouse that her business of 15 years was currently renting.

Like many high-net-worth clients with no business debt facilities and an unencumbered home in Brisbane worth $1.5m, they thought they could settle with little red tape and well within the now fast-approaching settlement date. In addition to the wife’s business, the husband had enjoyed year-on-year increasing profits from his steel fabrication business.

But sadly, this was not to be the case. Not only were the couple without any credit facilities, but the responsible lending obligations, combined with their ages

(74 and 65 years old respectively), meant they had not yet been able to secure approval, nor was approval on the horizon.

To add further stress, they had paid a large deposit of $200,000 on the warehouse purchase, and the vendor was unwilling to offer extensions to the settlement date, so they had to get the deal done as soon as possible.

Naturally, we were excited at the chance to help these wonderful people and had no reservations about extending assistance. We realised time was of the essence and quickly refined our product search with the help of our aggregator partner, SFG.

After searching through our product options to find the one that was in the best interest of our client, we identified three lenders that were likely to be suitable for their particular situation. Following discussions with our contacts at the respective lenders, including Graeme Norris of Better Choice, we talked through the options with our client and gathered any additional information to refine the search further.

After getting feedback from the client and having a further discussion with Graeme Norris, it became apparent that Better Choice offered the most competitive rate, along with flexible terms and policies; and, importantly, in our educated view we could secure an approval and settlement within our client’s time constraints – a significant hurdle to overcome and something the client was adamant should be a priority when selecting a lender.

The first task after acceptance of our recommendation was to order a valuation and have our client execute discharge authorities of their mortgagee, as most require 30 days’ notice to prepare their discharge and accept a PEXA invitation.

So it was that within days of fielding the referral we were able to lodge our client’s application on 24 August, and Better Choice provided conditional approval six days later – no small feat given that it had only recently launched this home loan range.

It was happy days all round when we shared confirmation from the credit team at Better Choice as well as Galilee Solicitors. Settlement was inked and the purchase confirmed on 9 September, two days before the contract stipulated.

Some of the hurdles this application presented:

As all mortgage brokers are aware, once an application is lodged it’s up to the lender to liaise with its solicitor to ensure loan and mortgage documents are prepared, returned and checked and a settlement invitation issued.

Building relations with referrers, aggregators and lenders is as important today as it has ever been, and, in that regard, we were delighted that Graeme at Better Choice took up the challenge, escalating the application with assistance from his settlements team, with docs out on 3 September.

To be able to work with our partners to deliver such a positive outcome is incredibly gratifying and reaffirms why we love what we do. We now have some very satisfied customers and strengthened relationships with all the parties involved.