Greg Woolley, director of Performance Finance Solutions, explains how believing in his client when no one else did sustained him through a series of rejections before ultimately securing a happy ending

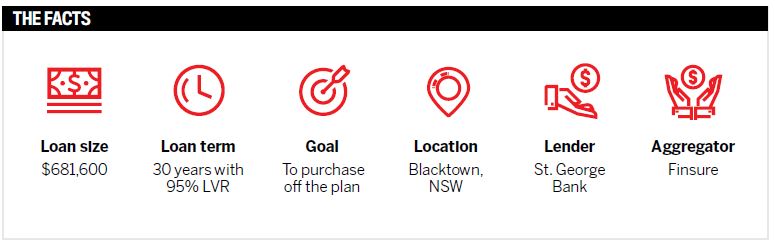

A client I had helped get into their first home years earlier recently contacted me, explaining that they had sold their previous property and bought another off the plan that was due for registration and settlement in the coming weeks. With no time to do a pre-approval, we discussed his options and decided to put an application through with a non-bank lender offering one of the better rates available at the time.

The application seemed to run through smoothly, but when it went for approval and sign-off by the mortgage insurers, there was a delay, and the lender was unable to explain why.

The lender then came back and asked for six months of bank statements to confirm income. By this time, the solicitor had advised that the property had been registered and settlement was due in the coming weeks. I contacted my BDM again and, after a few days of chasing, he eventually advised that the file had been declined. He was unable to help further and gave no explanation.

I was shocked and wanted to understand why this had happened. I dug deeper and found that the mortgage insurers had declined the file, but again no real explanation was provided.

Because of the short timeline, we promptly approached another lender, and the same thing happened: the file moved through the assessment process before it was again delayed, then knocked back. The client was quite frantic, with settlement just days away at this point.

My aggregator BDM thought the mortgage insurer’s issue with the income verification was due to the client’s employment letter not having an ABN, the payslips having no YTD, and the reference of bank statements differing. All of this together could have made it seem that he was staging his income.

At this point, the client decided to try to get finance through other avenues. After not hearing from him for a while, I reached out to make sure everything was OK. It wasn’t. He had been knocked back three more times with other lenders. He had an extended notice to complete and was on the verge of losing $72,500 – the 10% initial deposit.

Further, he had been told by another broker that he had a mark against his name with the mortgage insurer. He tried to contact the lenders and insurer directly to find out what the problem was, but with no success.

To me, it seemed that if this was someone dodgy he would have given up rather than making direct contact. I also knew the client from his previous application and had met up with him at his place of employment, so I believed he wasn’t doing anything wrong. I knew we had to give it one last try.

I did my homework and noticed that each lender he had tried was associated with one specific mortgage insurer, so I decided to seek one out that was aligned with a different insurer. But, based on the number of enquiries he had made, I knew that point-scoring might be an issue.

I remembered that St. George had its own sign-off with mortgage insurance, as well as 24-hour turnaround times. I spoke to my St. George BDM straight away. After explaining the situation in great detail, he told me he was confident and would support the deal as long as we had the supporting information to back everything up.

We immediately ordered the upfront valuation, submitting the deal the same day. We received the initial conditional approval within 24 hours, which was great, but we knew that we had more work to do.

The client was asked to visit a St. George branch to be formally identified and to provide further clarification of income, six months of bank statements for each of his accounts, and explanations of all large deposits and the previous applications that had been declined.

I worked with the client around the clock, and when we finally got through it all, the application went up to senior credit for sign-off . I passed an anxious 48 hours before being notified that the loan had gone formal. I let the client know, who immediately rang me up saying how appreciative he was for believing in him when no one else did. He also said St. George had a home loan client for life.

The bank organised the documents quickly and, even though the client had just under a month’s notice to complete, the other side waived the penalty interest – a great result following a process riddled with moments when the application seemed unlikely to ever be approved.

Greg Woolley

Director,

Performance Finance Solutions