A recent CBRE survey has found that lenders are increasingly investing in alternative Australian property assets, such as data centres, healthcare, childcare, and self-storage rather than traditional office and retail properties.

The H2 Lenders Sentiment Survey, which surveyed 40 domestic and international banks and non-bank commercial lenders, revealed there is “untapped investment potential” in the alternative assets sector and an $1.3 trillion opportunity for lenders.

For experienced commercial brokers, the opportunity is there to facilitate these deals as lenders aim to meet renewable energy targets and diversify their portfolios with many reducing their risk appetite.

“We have seen a significant uptick in the appetite to lend on alternative assets following a marked increase in sales volumes and equity side investment appetite to build exposure to these emerging asset classes,” said Andrew McCasker (pictured above left), CBRE’s managing director of debt and structured finance.

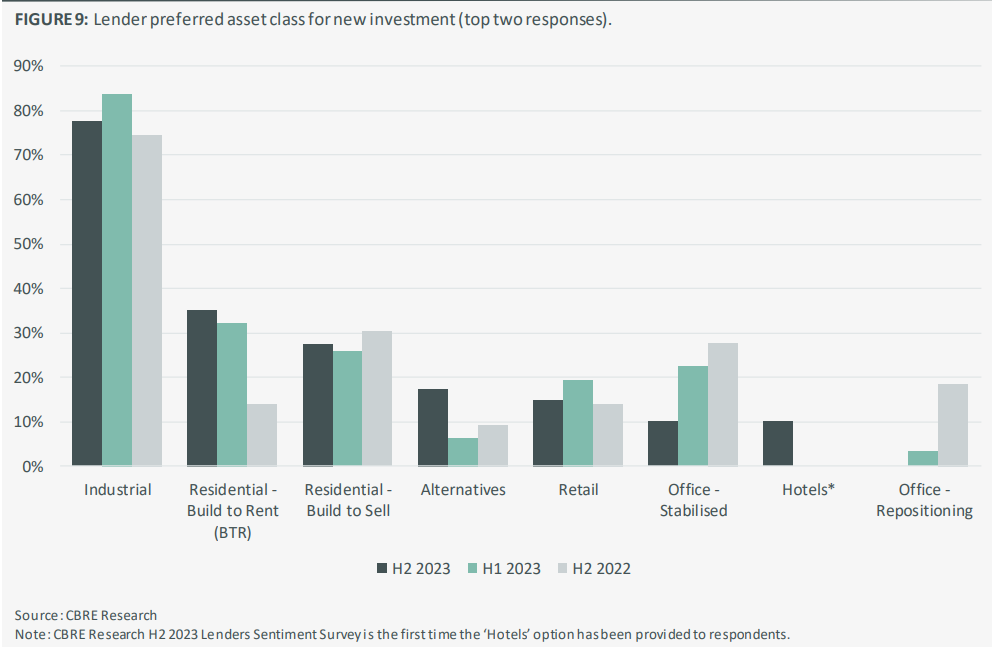

The industrial and logistics sector has retained the mantle as the most sought-after asset for debt investment, with over three-quarters of lenders calling it their most preferred asset class.

This has largely been driven by the lowest national vacancy rate globally, sitting at a significantly low 0.6% for the first half of the year, according to CBRE’s Australia Industrial & Logistics Vacancy Report.

To put this within a global context, cities that have recorded a sub-4% vacancy rate had recorded an average of 14.2% year-on-year growth over three years.

The report said the Australian market was unique given that it was shaped by a “chronic undersupply of industrial space”, which would likely keep the vacancy rate low for the foreseeable future.

Conversely, McCasker said the survey highlighted that the appetite to lend on office assets had continued to decline and now trailed retail for the first time since the survey’s inception at the start of 2022.

“Sentiment towards the office sector has been compounded by a lack of sales evidence in the market to demonstrate a softening in yields,” McCasker said. “Until lenders have certainty as to the impact on values, they will continue to have a conservative view on this sector.”

Lenders have also maintained their appetite for build to rent (BTR) assets across Australia, with BTR ranked second behind industrial on the list of preferred asset classes for new investment.

A relatively new asset class within the Australian housing landscape, build to rent is a type of housing development where properties are specifically designed and constructed for rental purposes rather than sale.

In the CBRE H1 Lenders Sentiment Survey, McCasker said the majority of lenders were “willing participants” in the BTR sector, with it picking up steam over 2023 and 2024.

The latest survey highlighted that more offshore banks and non-bank lenders have grown their appetite for this asset class, tripling its sentiment among lenders since the first half of the year.

“The underlying fundamentals of Australia’s housing economy is creating significant opportunities in the BTR sector and the desire by domestic and offshore financiers to fund projects will see this sector continue to grow in the coming years,” McCasker said.

Overall, the results highlight a flattish appetite for new Australian property loans over the next three months, with 37% of respondents wanting to grow their loan book and 10% wanting to decrease.

With 52% of lenders wanting to keep their commercial loan books flat, many are also opting for lower LVR requirements.

Nearly two thirds of the 40 banks and non-bank lenders said their preferred LVR requirement was below 50%.

However, the report said there should be increasing certainty as the macro-economic outlook

“should support the case for increasing loan appetite”.

Another concern for commercial lenders throughout the year was whether they would face a “debt maturity cliff”.

Approximately $370 billion of debt supports the Australian commercial real estate (CRE) sector.

With a large amount of loans refinancing from low pandemic rates into a high-rate environment, the possibility arose that a large number of debts was to be refinanced at the same time.

In this situation, borrowers might face difficulty refinancing their loans, as lenders may be less willing to lend money at higher interest rates. This could lead to defaults, where borrowers are unable to repay their loans.

However, CBRE research said the concern was “unwarranted”.

CBRE associate director, debt & structured finance, Will Edwards (pictured above right) said the results provided a level of reassurance around the availability of debt capital for pending refinances, noting that these will take place on revised metrics and the time to execute may be protracted.

“The survey responses indicate that more than half of lenders have less than 25% of their loan book maturing in any given year from 2024 to 2026, with no indications of a significant ‘debt-maturity cliff’ in Australia,” Edwards said.

The period from 2026 to 2028 indicate the highest concentration, however these figures remain relatively low.

What opportunities do you see in the alternative assets lending sector, especially in industrial? Share your comments below.