ANZ, the only big four bank still offering a cashback deal to refinancers, has announced it will be halving its offer from August 26.

The offer will reduce from $4,000 to $2,000 on eligible loans over $250,000 with a deposit of 20% or more. Loans with less than a 20% deposit will no longer be eligible for cashback.

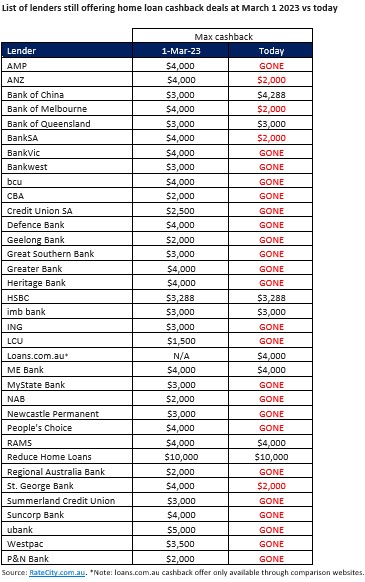

The highest cashback offer currently available for refinancing, from Reduce Home Loans ($10,000), stays unchanged, according to RateCity.com.au. However, this amount is only for loans of over $2 million and not available on the lender’s lowest rate.

RateCity.com.au research director Sally Tindall (pictured above) said ANZ was still on the hunt for new customers, but in a marketplace where cashback sweeteners were dropping like flies, there was no need to splash quite as much cash.

“ANZ’s rates aren’t the most competitive in the market, but some customers will still be drawn to an offer of $2,000 in cold hard cash,” Tindall said.

In terms of the other major banks, both Westpac and NAB scrapped their home loan refinance offers on 30 June while Commonwealth Bank (CBA) removed its cash handout on 31 May.

In a NAB Broker webinar yesterday, Nicole Triandos, NAB’s head of strategic partnerships, broker distribution, said the major bank was “happy” it had pulled its cashback offer out of the market.

“We prefer to compete on service and other components of the proposition,” Triandos said.

What do mortgage brokers think about cashbacks?

The number of lenders offering cash incentives to borrowers has dropped considerably in recent months.

The RateCity.com.au database shows there are now just 12 lenders left in the cashback game, almost one third of the 35 there were in March 2023.

“While there’s still a handful of banks holding on to these sweeteners, customers can’t expect them to last forever. Borrowers hoping to maximise a refinancing deal with a cashback hit should consider making the move soon – but be smart about it,” Tindall said.

“Households looking for long term relief are likely to be better off looking for an ultra-low rate and haggling with their new bank to waive any associated fees.”

Cashbacks have long been contentious among brokers.

In a 2021 article, Sarah Eifermann, a long-time broker and finance coach at SFE Loans, told Australian Broker of the problems that many within the broker channel saw in cashback deals.

“Cashbacks are seen to clog the service levels of lenders,” she said. “They drive business to a particular lender for one metric alone, that being the cashback. They can be seen to be in conflict with BID.”

More recently, brokers had expressed their approval about cashback offers ending with many smaller lenders offering products that instead incentivise brokers rather than encourage clawback.

What do you think about ANZ’s reduced cashback offer? Comment below.