The number of Australian households who are struggling to refinance due to serviceability issues has surged from 15% to 30% in just less than six months, according to Compare Club.

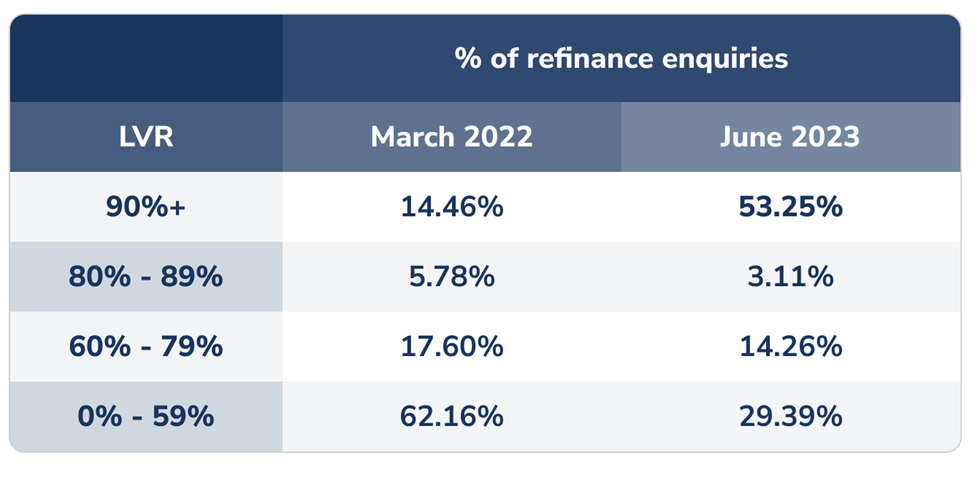

New data from the personal finance marketplace and advice company also showed a skyrocketing number of refinancing enquiries from mortgage holders with an LVR of 90%, which makes refinancing tough, if not impossible, and to a level not seen since interest rates began to rise.

In a statement, Compare Club explained that lenders are far less likely to offer competitive rates to borrowers with an LVR of 80% or higher and will often advise them to also fork out thousands more dollars to cover the cost of lenders mortgage insurance, which has the effect of locking people into mortgage prison, as they will be unable to access lower interest rates.

“The sharp spike in homeowners with a high loan-to-value ratio in just a few months really shows just how financially stretched many Aussie households are right now and even if we're close to the peak of cash rate rises, that’s cold comfort to the thousands of mortgage holders stuck on a rate of 7% or higher,” said Kate Browne (pictured above), Compare Club head of research and insights.

“It’s doubly disheartening for those people who see rates advertised at 1% or 2% lower than they’re currently paying, but their higher LVR or other serviceability issues are stopping them from lowering their home loan repayments…”

Compare Club’s analysis of more than 49,000 refinancing enquiries showed an alarming upward trend of 90% or higher LVRs since April. From 90+ LVRs making up 12% to 20% of all refinance enquiries up until the back of 2022, the number suddenly jumped to 38% of all refinance enquiries in July, before skyrocketing to nearly 60% of enquiries in July.

Comparing data between June 2023 and March 2022, prior to the cash rate hikes to 4%, showed that the number of refinance enquiries from homeowners with 90%+ LVR has more than tripled. See table below.

Compare Club said the data suggested that homeowners are being squeezed by several different pressure points on their mortgage. These included the following:

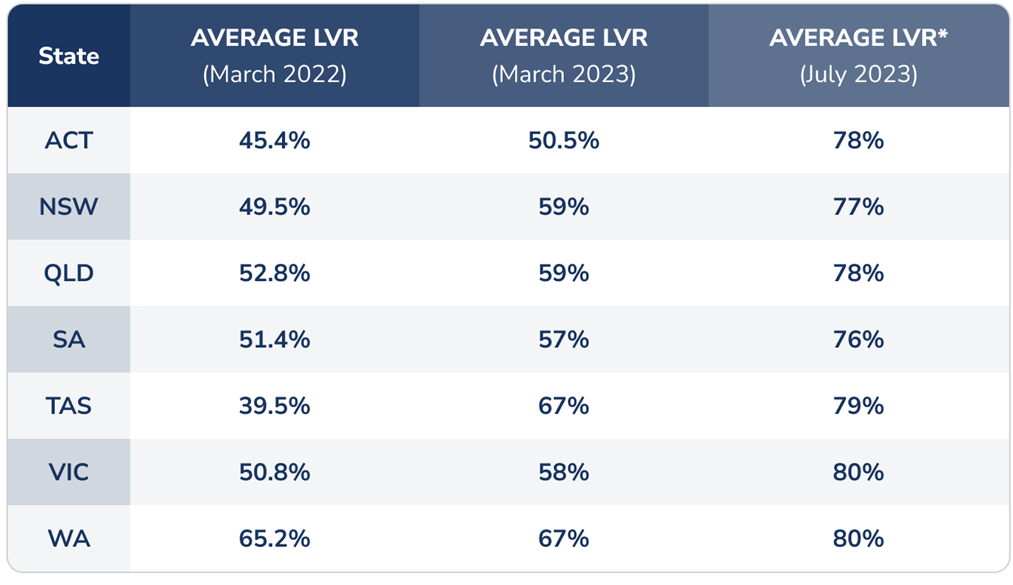

Across the states, residents in Victoria and WA were potentially struggling the most, with the average LVR for refinance enquiries now at 80%. The highest increase in LVR was in Victoria, where average LVR jumped from 58% in March to the current 80%.

Browne said borrowers with higher LVRs should not despair though. One thing borrowers can do to reduce some of the financial pain is to speak to their bank or broker, so they can access better rates.

“Banks really don’t want to have to repossess your house, so they may offer you a slightly lower rate that can give you a bit of breathing room,” she said. “It won’t be the best rate you can get, which is why engaging a broker as early as possible can really help. They’ll have access to lenders you won’t find on the high street and will know which lenders have a higher risk appetite or value properties differently from Australia’s big four banks.”

Use the comment section below to tell us how you felt about this.