By

Strong growth in home values has made Australians ‘relatively wealthy’ – but Aussies hold a dangerously disproportionate share of their wealth in housing, warns Macrobusiness’ chief economist, Leith van Onselen.

Van Onselen tells Australian Broker mortgage affordability is improving, but remains poor on an overall level, while the proportion of household income ‘chewed-up’ by mortgage interest payments is 34% higher than in 1989, when mortgage rates peaked at 17%.

“Virtually all growth in housing values has come from land price appreciation, with land prices roughly doubling relative to GDP since the late-1980’s.”

Furthermore, argues van Onselen, Australia’s vacant land has become ‘prohibitively’ expensive, with all markets experiencing rapid price appreciation.

So how did we get here?

#pb#

The ratio of Australian mortgage debt to GDP has risen four-fold since 1990, following deregulation of the financial sector, while the share of loans channelled into housing has increased from 24% of total loans in 1990 to 59% currently.

“The rapid expansion of mortgage debt and housing values has been funded, to a large extent, by heavy offshore borrowings by Australia’s banks and is represented by a massive expansion in bank assets – mainly mortgages.”

Strongly rising commodity prices have also played a role in increasing housing values since 2004, says van Onselen, via their positive impact on incomes.

“The Australian Treasury estimates that 50% of Australia’s income growth over the 2000’s came from the one-off terms-of-trade boom, whereas McKinsey estimates that 90% of Australian income growth since 2005 came from the mining boom.”

#pb# The number of property investors has also surged – from 696,000 in 1990 to 1.75 million in 2010 – and nearly 60% of investors are baby boomers.

“Two-thirds of investors were negatively geared in 2010, losing on average $2,750 per year, or a total of -$4.8 billion. Three quarters of negatively geared investors earned less than $80,000.”

Van Onselen says the country’s ‘rigid’ urban planning system has ensured that the increased demand has manifested in rising prices rather than increased dwelling construction.

“Empirical evidence from the US and elsewhere shows that markets with responsive land-use regulations have more affordable housing markets and experience less price volatility, as changes in demand manifest more in new construction rather than prices – growth in US house prices bore little relation to income and population growth.”

#pb# He says US markets with responsive land-use regulation remained affordable and experienced relatively low house price volatility throughout the bubble/bust period.

“In Georgia [USA], policies mandating lending to the poor and under-privileged resulted in massive subprime lending, yet, Georgia’s delinquencies never reached the levels of the supply-restricted bubble states. Big demand ‘shock’ from the GFC caused rate of household formation to plummet as individuals increasingly opted for group housing.”

This, in effect, turned a perceived housing shortage into a glut.

But could the group housing option viable in Australia? Yes, says van Onselen – and it’s actually already started to grow in popularity.

#pb#

“According to the 2011 census, the percentage of group households increased to 4.1% from 3.9% in 2006, whereas the percentage of single (lone person) households declined to 24.3% from 24.4%.”

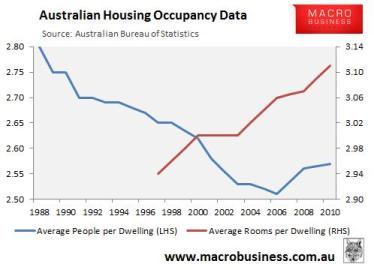

ABS data confirms this trend, with the number of people per dwelling rising since 2006, while the number of bedrooms per dwelling has also been trending upwards.

“There is significant latent capacity (excess bedrooms) in the pre-existing housing stock. Should economic conditions deteriorate materially, the number of Australians opting for group accommodation would likely rise significantly, just as it did in the USA, which could potentially turn a perceived housing shortage into a surplus.”

While Australia’s restrictive urban planning regime has helped drive prices higher during the boom, van Onselen says it’s unlikely to save the country from price falls in the event of a major shock to demand.

“A perceived housing shortage could easily turn into an oversupply, just like it did in the supply-restricted states of the USA.”

#pb# Factors including a 2011 peak in commodity prices (and subsequent decline) and an aging population could further reduce the economy’s potential demand for housing.

“Severe housing correction is an outside chance if Australia experiences a mining bust – i.e. sharply lower commodity prices combined with a big reduction in mining investment. This combination would cause sharp falls in incomes, a big increase in unemployment and potentially a credit squeeze.”

In order to free up the supply of housing, van Onselen says the government needs to do the following:

1. Ensure an adequate supply of affordable land for housing by removing regulatory growth constraints such as urban growth boundaries and restrictive zoning. This would increase competition and contestability in the land market and lower land prices;

2. Speed-up development approval processes, so that housing supply is able to respond more quickly to changes in demand;

3. Ensure housing-related infrastructure is adequately financed and provided in order to facilitate the provision of affordable housing.