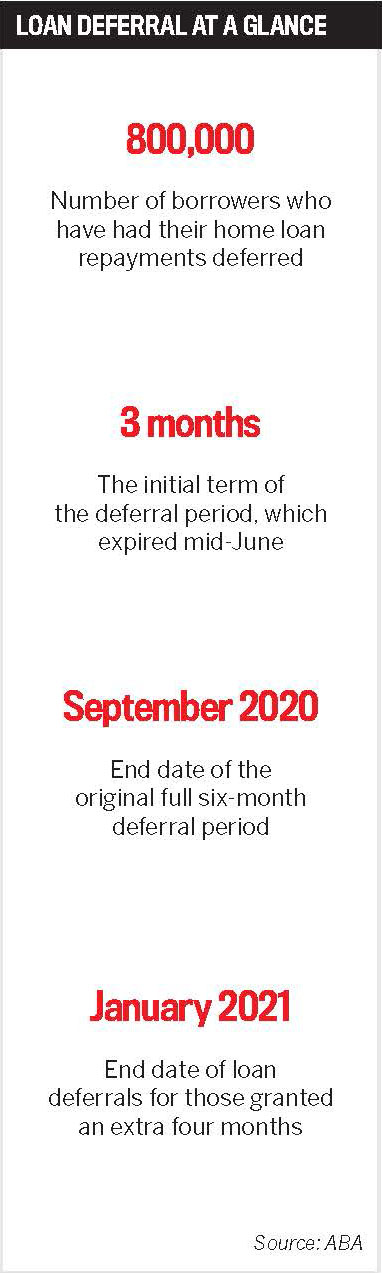

With the September deadline ofhome loan repayment deferrals looming, many have questioned how borrowers and the economy will cope with the double-whammy ‘fiscal cliff ’: the end of JobKeeper and the transition out of home loan deferrals.

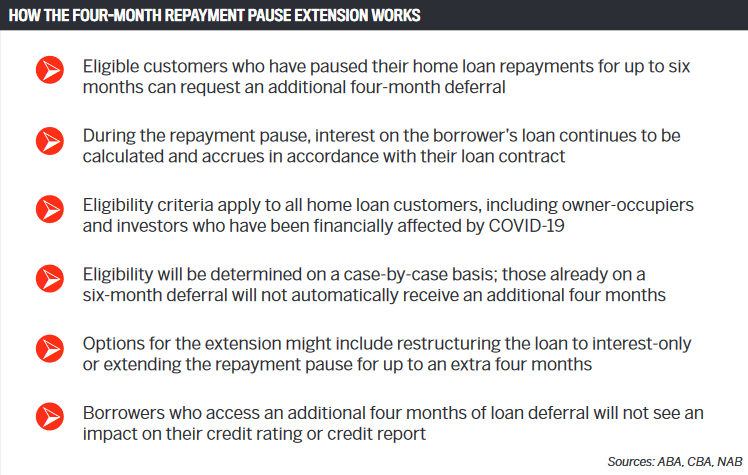

This month, banks and lenders provided some clarity around how they plan to handle the mortgage deferral side of the equation. The Australian Banking Association announced plans to implement a new phase of support to assist customers as the six-month loan repayment deferral period draws to an end.

The loan deferral scheme, which was introduced in March in response to the pandemic, allowed eligible borrowers to pause their mortgage payments while they dealt with the financial impact of the coronavirus-led economic slowdown.

As customers approach the end of the deferral period in September, banks will begin to implement what the ABA calls a “new phase of support to assist customers to get back to making their repayments”.

“Those who are able to repay their loans will resume doing so, which is in the best interests of those customers and allows support to be directed to those who need it. Encouragingly, many customers have already chosen to resume making repayments,” said Anna Bligh, CEO of the ABA.

Anna Bligh, CEO, Australian Banking Association

Anna Bligh, CEO, Australian Banking Association

Customers with reduced incomes, however, will be contacted as they approach the end of their deferral period to ensure that, wherever possible, they can return to repayments through a restructure or variation to their loan.

“If these arrangements are not in place at the end of a six-month deferral, customers will be eligible for an extension of their deferral for up to four months. Customers will be expected to work with their bank during this extra time to find the best solution for them,” Bligh said.

She confirmed that deferral extensions would not be applied automatically and would only be provided to “those who genuinely need some extra time” to get back on their feet financially.

“Those who are able to repay their loans will resume doing so, which is in the best interests of those customers and allows support to be directed to those who need it” Anna Bligh, CEO, Australian Banking Association

“Those who are able to repay their loans will resume doing so, which is in the best interests of those customers and allows support to be directed to those who need it” Anna Bligh, CEO, Australian Banking Association

“Many customers may need less than four months to either restructure their loan or to get back into full repayments,” Bligh said.

Federal Treasurer Josh Frydenberg welcomed the announcement and confirmed that APRA would continue to ease regulations imposed on the banks to encourage them to support customers.

“If somebody’s lost their job and they’ve got a residential mortgage, or indeed if their business has been closed and they’ve got a commercial loan, then they would be cases where the customer would need to talk to their bank, and I understand it that the bank is going to be very supportive of their customers,” he said.

Meanwhile, Adrian Kelly, president of the Real Estate Institute of Australia (REIA), said the plan was “to be applauded”.

Adrian Kelly, president, Real Estate Institute of Australia

Adrian Kelly, president, Real Estate Institute of Australia

“As the September deadline draws nearer, the banks have made a sensible decision to give homeowners a bit more breathing space for those who need it, to work with the banks and get them on their feet financially. The government will need to consider further rent subsidies post-September in order to ensure that tenants who have lost employment are not evicted,” he said.

“Supporting homeowners during this phase, where they may be finding it di fficult to continue paying their mortgage, is to be applauded. If owners and landlords are supported, then tenants, some of who are from the most aff ected industries through COVID-19, are also supported.”

Kelly said the REIA had also put forward recommendations to the government to assist the real estate sector and renters to continue contributing to the economy as Australians collectively recover from the pandemic.

“The government could go further in their support of the economy through the real estate industry by abolishing or temporarily ceasing stamp duties on residential property. An abolition or temporary concession on land tax would also help stimulate an economy in recession,” Kelly said.

“However, the banking industry is to be commended for their continuing support of current homeowners, landlords and tenants. It is hoped the government will also consider a stimulus to the sector to boost expected low levels of unemployment and address growth in the Australian economy.”

Brokers who have customers currently on deferral programs are likely to receive an increase in enquiries around eligibility for further mortgage relief.

Eligibility for the four-month extension has yet to be confi rmed, although the ABA has warned that not all current repayment deferral customers will be eligible for an extension.

Westpac has announced its support of the policy, revealing a raft of additional assistance on loan deferral packages for home loan and small business customers who continue to be significantly impacted by the COVID-19 pandemic. The measures include further support for customers who are not in a financial position to resume their full loan repayments from the end of September.

“The COVID-19 pandemic is continuing to have a fast-changing impact here in Australia, and we know that for some customers, this will have a longer-term effect on their circumstances and further financial support will be required,” said Gary Thursby, Westpac’s acting chief financial o fficer.

Gary Thursby, acting chief financial officer, Westpac

Gary Thursby, acting chief financial officer, Westpac

“In discussion with the industry and regulators, we will be making changes to allow more time and breathing space for customers who aren’t in a position to return to full payments again from October. This includes access to tailored support through our customer assistance program, where our specialist team will work with customers to review their financial circumstances.”

For customers who remained under stress but could still contribute to their loan repayments, Thursby said the bank would “provide support where we can help work through options that may be available to adjust their loan”.

“As the September deadline draws nearer, the banks have made a sensible decision to give homeowners a bit more breathing space ... and get them on their feet fi nancially” Adrian Kelly, president, Real Estate Institute of Australia

However, he added that “we anticipate that a significant number of customers will be able to resume regular repayments when their deferral term ends. We expect these customers to start their repayments again, and we would encourage as many people as possible to do so”.

For small business owners who require further support, the banks are also inviting eligible small business customers to apply to extend their business loan repayment deferral period by up to four months. Interest will continue to capitalise on these commercial loans during the deferred repayment period, as is the case with residential loans.

According to CBA chief executive o fficer Matt Comyn, a number of the bank’s retail and business customers have resumed full or partial payments on loans that were placed in deferral at the start of the pandemic. As more customers restart their loan repayments, CBA plans to target its support at those people who most need it, he added. Comyn also confirmed that any customers who engaged in additional loan deferral for up to a further four months would see no impact on their credit report or their credit rating.

Matt Comyn, CEO, CBA

Matt Comyn, CEO, CBA

“While many customers are doing better than we expected, we know that some customers will require further support, and we will contact them over the coming months to discuss the options that might be available to them,” Comyn said.

“Supporting customers who continue to experience financial difficulty is a priority, and we are tailoring our support to make sure each customer gets the advice and assistance that suits them. This next phase of our support reinforces the strong collaboration and effective cooperation between federal and state governments, regulators, and the banking industry, which has allowed so much to be achieved in such a short time.”

As for the impact loan repayment deferrals will have on the broader property market, the offer of additional mortgage repayment pauses by lenders is further proof that the September “property market crash” was always unlikely, according to Daniel Walsh, director of buyers’ agency Your Property Your Wealth. Walsh said buyer demand had already been steadily increasing in some markets before the announcement was made.

Daniel Walsh, director, Your Property Your Wealth

Daniel Walsh, director, Your Property Your Wealth

“Savvy buyers and investors have recognised that lenders were never going to simply walk away from borrowers come September, so they have been more active in the market over the past two months,” he said.

“Banks have a duty to assist borrowers experiencing genuine financial hardship, which is exactly what the Australian Banking Association has said lenders will do with possible four-month extensions of mortgage repayment pauses.”

When the coronavirus first hit, buyers were able to get discounts on properties due to “poor consumer sentiment and concerns about the economy generally”, Walsh added.

“In some locations, not only are those discounts now gone, but there is also now strong competition for listings, which is pushing prices higher. This is especially the case in locations like Brisbane, which aren’t dependent on international migration and were already the beneficiary of strong interstate migration,” he said.

Walsh’s comments are in contrast to a recent survey of property professionals conducted by NAB. Prices across most state capitals are expected to fall over the next two years as property sentiment deteriorates amid the COVID-19 pandemic, according to the Q2 2020 poll, which predicted that house prices would fall by 2% nationally in the next 12 months and by 0.1% in the year after.

Alan Oster, chief economist at NAB, says prices could decline by around 10% to 15%, peak to trough.

Alan Oster, chief economist, NAB

Alan Oster, chief economist, NAB

“While prices have held up slightly better than expected, they have now declined for two consecutive months across the capitals, and we expect this to continue for some time yet,” he said.

Of the capital cities, NAB’s survey expects Melbourne to post the most significant annual price decline this year at 7.3%, followed by Sydney at 4.7%. Next year, it predicted prices in Melbourne are likely to fall by a further 6.5%.

On average, capital cities are slated to record declines of 4.6% this year and 4.3% next year, according to NAB.

“While the initial COVID-19-related restrictions on housing activity have eased, the economy has undergone a very large contraction, and while we appear to have passed the trough in activity, it will take time for the recovery to unfold,” Oster concluded.