Bendigo and Adelaide Bank reports a 13% increase in half-year net profit, but net interest margin faces pressure from “irrational” competition.

The Australian regional bank announced a 13.8% rise in net profit to $282.3 million for the six months ending in December, exceeding analyst expectations of A$257 million.

However, the bank's net interest margin, a key profitability metric, was impacted by competition in both lending and deposit markets with its home loan lending stalling over the period.

Marnie Baker (pictured above), the bank’s CEO and managing director, said the bank’s decision to repay the RBA’s Term Funding Facility (TFF) early and keep expense growth below inflation helped protect margins where “competitive tensions were irrational”.

“… (This ensured) efficient use of shareholder funds for the long-term benefit of our customers,” Ms Baker said.

Bendigo and Adelaide Bank’s mortgage books treaded water over the six-month period.

Total lending was down 0.7%, with competitive market pressures weighing on residential lending volumes, down 0.1%.

This was largely felt across the bank’s investor loans, which lost $623 million between the end of June and the end of December. But it was buoyed by its owner-occupied books, which grew by $603 million.

Bendigo and Adelaide Bank acknowledged that the competitive challenges outlined in their full-year results persist. Baker specifically mentioned facing "heightened competition across the mortgage portfolio," which has led to slower growth compared to the broader market.

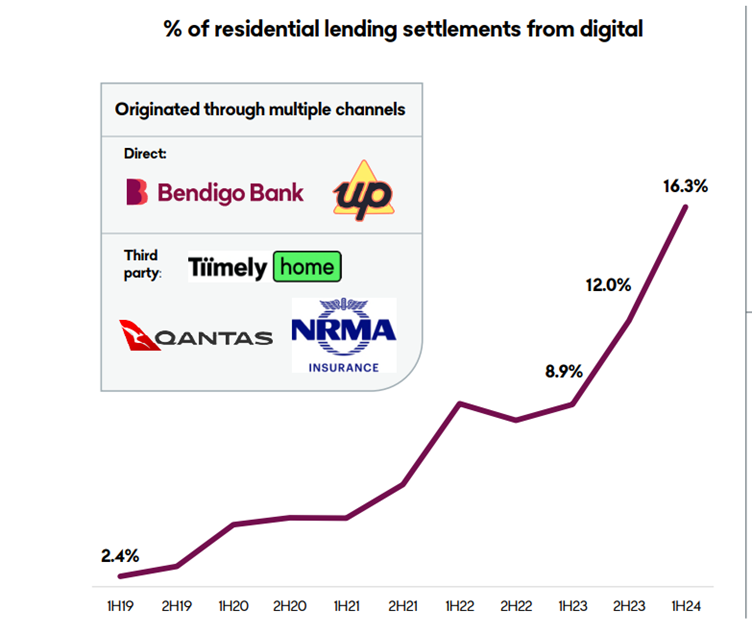

However, despite these headwinds, the bank finds optimism in its digital mortgage products, which now account for 7% of its entire mortgage portfolio. These products continue to experience growth across both the bank's direct channels (Bendigo Bank and Up) and its third-party partnership with Tiimely (formerly Tic:Toc).

Baker expressed confidence in the future, stating, "Digital mortgages continue to provide growth opportunities both directly and through our white label partnerships with Qantas Money Home Loans and NRMA Insurance."

This suggests that the bank views digital mortgage products as a key strategy to navigate the competitive landscape and achieve future growth.

“Digital mortgage settlements accounted for 16.3% of all residential lending settlements for the half,” Baker said. “For deposits, the launch of online functionality for term deposits and savings accounts for new and existing Bendigo Bank customers has seen a 28% increase in digital deposits.”

“The introduction of the bank’s new digital lending platform will provide greater optionality for scalable and sustainable growth.”

While overall business lending saw modest growth and agribusiness experienced a seasonal dip, Bendigo and Adelaide Bank highlighted positive developments in its newly formed commercial and agribusiness broker channels.

These channels saw a 25% increase in the half-year, demonstrating early signs of success in the bank's transformation efforts.

Despite a 3.9% decline in agribusiness lending due to seasonal factors, the business and agribusiness division posted a solid 16.7% increase in cash earnings. This growth reflects strong deposit growth, reduced operating expenses, and lower credit costs.

“Strategic decisions are always a balancing act, and we recognised some time ago the need for our business and agribusiness to be refreshed,” Baker said. “Early signs from the newly formed commercial and agribusiness broker channels are encouraging.”

The bank’s results showed Net interest margin (NIM) was down 15 basis points on the half to 1.83%, impacted by price competition in both lending and deposits and a higher level of liquid assets.

Baker said the revenue challenges the bank faced in the last half have sharpened its focus on accelerating investment in channels that drive profitable growth.

S&P echoed this conclusion in its rate check, saying the decline was due to price competition “on both sides of the balance sheet” as well a higher level of liquid assets.

“Furthermore, total lending was down 0.7% in the six months ended December 31, 2023, which was well below the system level.”

However the credit rater expects the bank’s capital position to “remain strong”over the next two years.

“We forecast BEN's credit losses will remain manageable at about 15 bps over each of the next two years, in line with those of its regional bank peers,” S&P said.

“We believe that low unemployment levels, modest economic growth, and a change in spending patterns will shield most borrowers against the rising interest burden and prices.”

For the full results, click here.