With 2020 now in the rear-view mirror, what will 2021 bring for the finance industry? Australian Broker asked brokers Tracy Kearey and Gerard Tiffen and Thinktank CEO Jonathan Street for their predictions.

Last year left many people across the country reeling from coronavirus lockdowns, job losses and Australia’s first recession in nearly 30 years. Despite this, the nation has done remarkably well compared to the US and UK when it comes to avoiding high rates of COVID-19 transmission and deaths.

The economy is starting to bounce back, with mortgage deferrals falling and job advertisements on the rise.

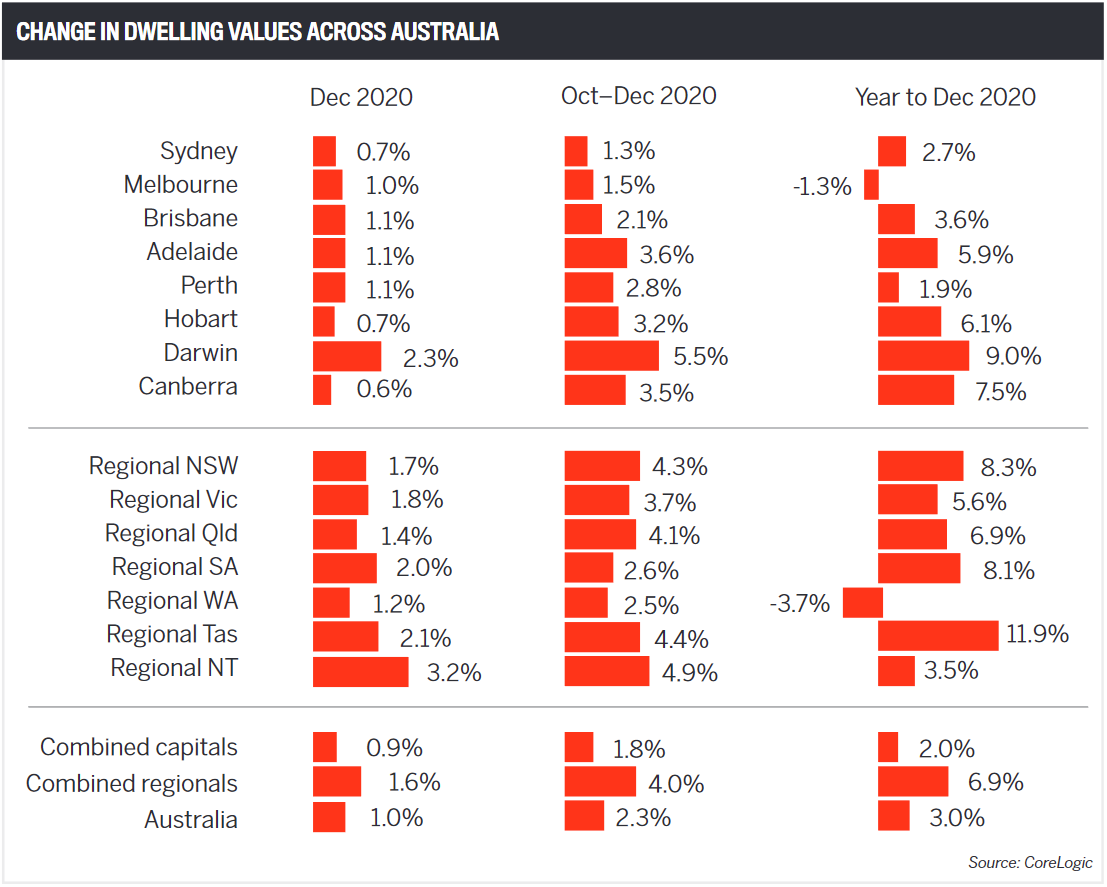

The property market is thriving; prices are booming in the regions and increases of up to 12% are predicted for the capital cities this year. Brokers and lenders are also optimistic about 2021.

Tracy Kearey is the managing director of Brisbane-based brokerage Home Loan Connexion. She leads a team of more than 30 brokers offering services across all forms of finance, including property, personal, commercial and equipment.

Kearey says 2021 will bring stability, opportunity and growth for the broking industry.

“Technology and further automation will improve the service offered by brokers, which will in turn improve the customer experience, reducing time and resources for both the customer and broker,” she says.

“Technology and further automation will improve the service offered by brokers, which will in turn improve the customer experience, reducing time and resources for both the customer and broker,” she says.

“There is an opportunity for the broker channel to assist a broader range of clients due to access to new lenders and products.”

With lenders changing their policies very quickly in a “forever-changing market”, Kearey says it is very difficult for consumers to deal directly with lenders.

“If I were a borrower I would not apply for finance on my own, based on policy and understanding. You need to have an expert on your side when you are borrowing money.”

Brokers recorded their highest market share ever of residential mortgages in the July to September 2020 quarter, at 60.1%.

“We got so much momentum from the back end of last year,” Kearey says. “If it continues, I think [a higher share] will be sooner rather than later; we may see it in the first quarter. We could get to 70%, and it may go higher. We’ve now got BID, we’ve got open banking and we’ve got a lot more technology.”

Award-winning Canberra broker Gerard Tiffen agrees that brokers will gain a greater market share in 2021. He is the managing director of Tiffen & Co, leading a team of 13 staff, with five brokers assisting clients with residential and commercial loans, including first home buyers and investors.

Award-winning Canberra broker Gerard Tiffen agrees that brokers will gain a greater market share in 2021. He is the managing director of Tiffen & Co, leading a team of 13 staff, with five brokers assisting clients with residential and commercial loans, including first home buyers and investors.

“I think customers in particular will continue to vote with their feet when it comes to us,” Tiffen says. “They want real impartial advice from successful brokers who will be around for years to come and care about them and outcomes. As long as we receive support from the lenders, growth is still achievable.”

Tiffen feels confident and excited about the year ahead.

“With consumer confidence bouncing back and interest rates low, and likely to remain low for a sustained period, now is a great time to borrow. There is a lot of state and federal government focus on stimulating the housing sector, and lenders seem willing to lend again.

“I’m hoping the back office of a few lenders improves, as turnaround times have been very difficult to manage at times through 2020. I expect this will happen as resources are reallocated. It’s important that the borrower experience is similar, irrespective of whether a loan is presented to a lender through a branch or by a broker.”

Kearey says an increasing public awareness of brokers has been driven by the royal commission, marketing from industry groups, as well as word-of-mouth client referrals.

“The perception in the market has changed about who we are and what we offer. The level of professionalism has increased – we are seen as an expert in home lending for any type of property and asset,” she says.

Tiffen says 2021 will be about “bedding in of some of the lessons learned from the past 12 months”.

“The use of tech, particularly being able to meet with customers using a combination of online and in-person, makes accessibility a lot easier than previously thought,” he says.

“For the first time in Tiffen & Co’s 22-year journey, the customer mindset changed in 2020 from ‘I need to see you in person’ to ‘I just need to see you’.

“We now conduct many customer interviews online. It’s a better experience for many borrowers, particularly those who we already have a relationship with. The ability to find half or a full hour in the diary is easier if you can remove travel time.”

Tiffen says technology is moving rapidly. “I am hoping lenders and regulators move in line with the tech and enable brokers and borrowers to tap into the new ways of doing business.”

Australia’s economic recovery is difficult to predict, Kearey says, but she believes that the nation is in a great position globally. “We need to remember that the recession we have experienced was created by a health crisis, not a financial crisis.”

But 31 March will be a crucial date. This is when JobKeeper payments, the JobSeeker supplement and HomeBuilder are all due to end, and it could hurt the economy.

“It’s a delicate balance,” Kearey says. “Brokers will continue to gain market share as more banks close branches and borrowers look for a more personalised and tailored approach when it comes to their financial affairs.”

Like Tiffen, Kearey also believes advances in technology will give brokers an advantage.

“The reduction in paperwork that comes with positive credit reporting and open banking will certainly make it easier for customers to refinance when there are savings to be had.”

Kearey says she works with a lot of property investors who haven’t been affected by COVID. “There are certainly people out there who have good employment, have probably got more savings in the bank now because they’re not travelling and spending like they used to, so they are investing in property.”

Regulation is a key focus in 2021 – the best interests duty came into force on 1 January. But Tiffen says BID won’t have much impact on his business.

“The requirements of BID reflect the way we approach every customer engagement today,” he says. “We seek to understand their needs, look at the available options and, if a first-time borrower, explain how everything works and their obligations when borrowing money.

“I’m hopeful – and expect – the winding back of responsible lending provisions gets through Parliament. The level of scrutiny required doesn’t reflect the reality at the moment. I know from my customer experiences they understand spending habits change when you take on new debt.”

Kearey says the only significant change for brokers with BID “is the requirement to keep better records – most brokers were already acting in the best interest of the customer anyway”.

“The changes to the responsible lending obligations and in particular the requirement to verify actual living expenses will make doing business easier,” she says. “Conflicted remuneration such as the volume bonus were removed by the Combined Industry Forum some time ago now.”

Summing up the year ahead, Kearey says: “If it’s anything like the year just gone for loan writing, and with the cash rate set to remain at an all-time low for the next few years, I am extremely optimistic about the prospects.”

But she believes continued government stimulus remains the key to consumer confidence and how the property market tracks, while low population and wage growth and high unemployment need to be closely monitored.

“If we can keep COVID-19 at bay, implement a successful vaccination program and see Australia’s borders open to international visitors, our chances of getting back to some form of normality and achieving stability in our property market will be greater.”

Tiffen says coming off the back of a “very unusual 2020”, a sense of normal will return with a “very active buying and borrowing market”.

“It’s good to see the amendments to responsible lending legislation are already before Parliament,” he says. “The current level of scrutiny is not warranted. It delays the process and, at times, precludes good borrowers from obtaining an approval.

“With lending regulations back at a more reasonable level, consumer confidence high and interest rates low, I’m expecting more records for Tiffen & Co in 2021. Can’t wait!

Non-bank lender Thinktank is a specialist commercial, residential and SMSF property finance provider with more than 100 staff across Sydney, Melbourne and Brisbane. Thinktank CEO Jonathan Street says he has an optimistic view of lending in 2021.

Non-bank lender Thinktank is a specialist commercial, residential and SMSF property finance provider with more than 100 staff across Sydney, Melbourne and Brisbane. Thinktank CEO Jonathan Street says he has an optimistic view of lending in 2021.

“This is based on continued growth through the presence of new lending opportunities supporting borrower needs across the financing needs of expansion, rationalisation and restructuring,” says Street. “One of the key sectors of activity will be in the non-bank space, with a greater focus on near prime residential, commercial and business lending.”

This, he says, will lead to increasing competition between existing players and new entrants, with the cost of capital low and availability high.

He believes another area of focus will be the continued rapid digitisation of systems by all banks.

“This will include having to manage an increased level of rigour via BID, and reliance upon electronic compliance and documentation systems,” Street says.

Automation will enable quicker lodgement and turnaround times, and lenders will be able to spend more time with brokers and their clients to offer the best financial solutions, he says. “It will be important to balance digitisation with the human side of lending to help effectively guide borrowers, while the role of a broker in facilitating this cannot be underestimated.”

Changes to responsible lending won’t necessarily lead to an easing in the supply of credit, Street says, but it should make it faster for consumers to access finance, with an improved application experience and approval times.

While a stronger economy and favourable property market will provide more opportunities for lenders, market share will be driven by “service, innovative products, insights and genuinely understanding a broker’s and borrower’s business., he says. “For this reason, non-bank lenders are well positioned for growth, given our strong emphasis on ingenuity and a service proposition that is well balanced between borrowers and brokers.”

Street says there are opportunities for both brokers and lenders. Strongly performing businesses will require extra capital for expansion, while those that are struggling may need help restructuring debt or rationalising assets. Flexible and alternative lending solutions, such as alternative verification (mid-doc) products and SMSF, will be also be critical.

Thinktank anticipates that the residential property market will steadily improve, coinciding with an economic uplift, particularly within the SMSF sector, but commercial property may take some time to reset.

“There will always be factors out of the control of a borrower or broker in regard to market conditions, lender product and policy movements, rates, external events – such as COVID-19 – government intervention, and the business and employment environment in general,” Street says.

He believes the relationship between a broker and customer remains an essential and valuable one to be relied on in uncertain times.

“Brokers who build and maintain these deep relationships will be highly sought after by customers to manage their financial requirements, be it for growth or stability,” he says.