By

With all the market disruption and uncertainty for business owners and the greater community of late, consistency and support are in high demand. Providing the latter has been National Mortgage Brokers’ primary focus in recent weeks so it can play its part in ensuring the broking community not only survives the current crisis but thrives in the future.

“nMB is backed by Liberty, one of the strongest financial institutions among the non-banks, and Liberty has been through a number of economic cycle challenges and come out stronger each time,” Foley says.

“Now, as through the GFC, nMB and Liberty remain open for business and ready to continue their support of nMB and our brokers, and the whole broker market.

”With over 18 years of experience, nMB is large enough to meet a borrower’s most complex needs, while also continuing to offer personalised service and a tailored approach.

Until the COVID-19 outbreak, nMB’s key focus in 2020 was on assisting its business partners in making the move from “broker to broker business”, which it was accomplishing by focusing on the 5Ps: people, premises, process, partners and planning (see boxout overleaf ).

Until the COVID-19 outbreak, nMB’s key focus in 2020 was on assisting its business partners in making the move from “broker to broker business”, which it was accomplishing by focusing on the 5Ps: people, premises, process, partners and planning (see boxout overleaf ).

In recent weeks, this focus has shifted to ensure that nMB is “supporting our brokers at three levels”, Foley says: “business operator, employer and personal”.

“Our broker network are small business owners themselves – they’ve got debt, families, they’re running a business, they’ve got staff – so they are going through a lot. What the COVID-19 crisis has shown is that borrowers not only need their broker to source a loan, but they are often their first port of call when things get difficult. We should really take that as a compliment. When a client rings their broker, the conversation is obviously about that client and their needs, but there is an immense burden on the broker to be problem-solving and supporting their clients at a time when they are under a lot of pressure themselves,” Foley says.

“Fortunately, we’ve been able to win the fight to keep trail for brokers. These are the times when trail commission is earned more than ever. If we were in a market where brokers lived off upfront commissions only, many brokers would have to consider whether to pack up and leave the industry. That’s not good for customers and it’s not good for lenders, especially smaller ones, who will need brokers when the market comes back.”

To that end, nMB has internally developed and released a number of resources in recent weeks, including tools and ‘how to’ guides for its network of brokers so they can continue to adapt and operate in this market.

“For instance, we’re extracting a lot of information and summarising it for our brokers, about the stimulus packages, what’s available and how to access it. We’ve put together a series of ‘How to’ guides on things like ‘How to build an online presence’ and ‘Social media for brokers’ – and, given the current climate, we’ve just launched our guide on ‘How to work well from home’. We can’t give advice on everything, but we can point our brokers in the right direction and give them the resources they need to get through this period.”

nMB has also reached out to every lender on its panel and put together a document outlining every lender’s different policies and processes around financial hardship.

“We were checking that everyone was OK and providing information so they could prepare for the big wave of enquiries and use this to help them quickly turn over calls. Our brokers don’t have time to scurry around the different lenders to get this information individually, because they’re being inundated by anxious clients who all have similar questions about financial hardship and loan repayment holidays,” Foley says.

“We can move quickly and work with our brokers ... [and we have] the backing of a really strong balance sheet and a company that’s got brokers in its DNA”

“We can move quickly and work with our brokers ... [and we have] the backing of a really strong balance sheet and a company that’s got brokers in its DNA”

“On that note, the use of expressions such as ‘repayment holidays’ has really created a lot of misunderstanding by borrowers. The number of calls brokers and lenders have received from borrowers thinking they were being offered a ‘holiday’ from being charged interest has been significant, so I’m really pushing to use and promote the term ‘repayment pause’ from here on.”

Foley says the lack of understanding around what a loan repayment holiday actually means has created unnecessary confusion and work for everyone in the industry.

This is because many people mistakenly thought a repayment holiday meant they were “getting something for nothing” – for instance, they thought it meant no interest would be charged on the loan whatsoever for six months – and, perhaps understandably, “they didn’t want to miss out”, Foley says.

He adds that out of every 100 enquiries about repayment pauses a lender or broker might receive, “over half hang up once you explain what it really means”.

“There have been some ridiculous examples. I was speaking to one lender who had a client with $140,000 in an offset account. They withdrew the money and then applied for financial hardship and requested a repayment pause. That isn’t the intended purpose of repayment pauses,” Foley says.

“There are many customers who don’t understand what ‘financial hardship’ actually means, and others are also responding or preparing for what may happen if this situation escalates, rather than what is actually happening to them. We always recommend our brokers have these discussions with their clients over email, because then you have a record of when you sent it, and also the person on the phone is not being required to record anything.

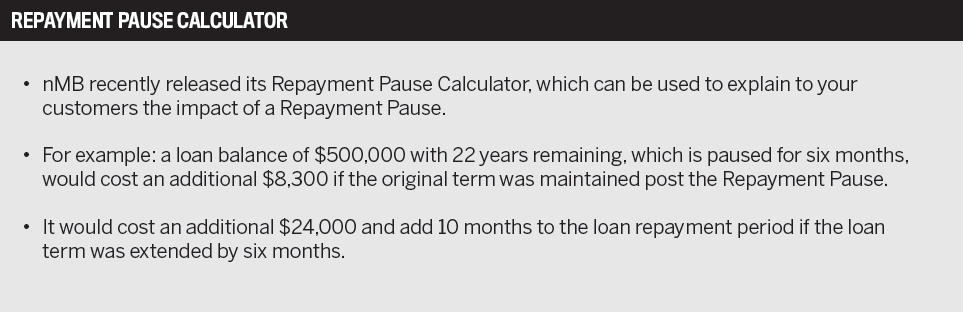

“In this area, we have also developed a Repayment Pause Calculator, which has been designed to help mortgage holders work out and understand what the financial impact will be.” (See boxout on p14 for an example of how the Repayment Pause Calculator works.)

While the rapidly evolving circumstances over recent weeks have certainly created plenty of challenges in the mortgage space, they may also be paving the way for innovations down the track, as people and businesses have been forced to adapt and problem-solve.

“What the COVID-19 crisis has shown is that borrowers not only need their broker to source a loan, but they are often their first port of call when things get difficult”

Case in point: loan interviews and ID requirements.

“Two years ago, we went out to all of our lenders and asked them for a clear policy around conducting a loan interview remotely. We wanted to be clear on whether the meeting had to be what we call ‘belly to belly’, meaning you’re in the room and potentially touching a person, or whether a face-to-face meeting conducted digitally would be acceptable,” Foley says.

“Two years ago, we went out to all of our lenders and asked them for a clear policy around conducting a loan interview remotely. We wanted to be clear on whether the meeting had to be what we call ‘belly to belly’, meaning you’re in the room and potentially touching a person, or whether a face-to-face meeting conducted digitally would be acceptable,” Foley says.

“We could not get responses from some lenders, and in the end we gave up. It was a constant thorn, as we just couldn’t finish this matrix off. However, in the middle of all this, they’ve now nearly all been able to review their policy and allow contactless meetings to proceed online. It shows that you can still build a very deep personal relationship between brokers and borrowers without necessarily being in the room.”

The broker’s key advantage to date has always been that personal connection, he says, and changing the way we communicate doesn’t change that.

“The world is saying, ‘don’t come nearby’, but the value proposition that brokers offer is still there – it’s just that the delivery is different,” he explains.

“Now you can have a four-way conversation in four different cities on Zoom if you need to. These are unprecedented times, and the lessons we can learn from the past are that those who have kept close to their customers will always become the first point of contact, and the value of the relationship will never be greater than during a crisis. A good customer care program is essential so that you can become the centre of influence, and then you will be able to reassure your clients and manage them through.”

Drawing from past challenges and finding the resilience and agility to pivot in these challenging times is something every business needs to do in order to survive them.

No one is immune to current market conditions, Foley adds, but it’s how brokers respond to the crisis and the service and support they provide to their clients that will truly set them up to traverse the uncertain road ahead and come out the other end wiser and with a sustainable business.

nMB is taking the same approach by ensuring it focuses on giving its network of brokers the resources they need to meet the challenges of the COVID-19 crisis.

“We’re structured in a way that we can move quickly and work with our brokers and help them manage their individual needs. We’ve got enough agility to work with our brokers and adapt as they need help, together with the backing of a really strong balance sheet and a company that’s got brokers in its DNA, which is really positive.”