Some brokers don’t offer personal loans, claiming they’re costly and cumbersome, but fintech lender MoneyPlace is determined to change their minds with fast funding and a simple online process.

Moneyplace head of broker sales Alf Vasta (pictured) is keen to dispel brokers’ myths about personal loans and educate them on how to expand into this space.

He spoke to Australian Broker about how the nimble, tech-driven lender is transforming the personal loan market. Brokers Mhairi MacLeod of Astute Ability Finance Group and Albert Lee of LendConnect also shared their views on MoneyPlace and the benefits of diversifying into personal loans.

Vasta says MoneyPlace was founded in 2014 by Stuart Stoyan and “we wrote our first loan in 2016”.

“We provide unsecured personal loans from $5,000 to $60,000 for any legal purpose. Importantly, we provide borrowers with a personalised interest rate, so customers who have good credit get rewarded with a market-leading interest rate.”

As an online business, MoneyPlace prides itself on efficiency.

As an online business, MoneyPlace prides itself on efficiency.

“In fact we recently funded a loan in 34 minutes from time of application to the funds hitting the customer’s account,” Vasta says.

“This process efficiency and strong automation helped us to be the leading personal loan provider throughout 2020.”

Vasta says common objections from brokers about personal loans include that they are “too expensive, time-consuming, paper-driven, not rewarding, and the purposes are limited”.

“The MoneyPlace proposition is the complete opposite – we have the lowest unsecured rate in the market, completely online. Loans are funded typically in four hours from a broker submitting an application to money going into the customer’s account, and we fund loans for any legal purpose.”

Vasta says the lender constantly makes changes to enhance its proposition and make it simple for brokers and customers, including taking on board feedback from brokers.

“The system for both broker and client is all online, and the time to lodge an application through the MoneyPlace portal on average is less than five minutes.

“The reason why our brokers like dealing with us is they have direct access to all our lending specialists, the people approving the loans.”

With the personal loan space dominated by the banks, Vasta says the most exciting aspect of MoneyPlace is bringing personal loans to the broker market.

“If you remember how 20-plus years ago the mortgage space was dominated by banks. Today around 60% of mortgages are from brokers.

“We hope to replicate this in personal loans, one broker at a time.”

Broker awareness of personal loans has grown in the last two years.

“We have really pushed the message out to the market that personal loans can convert more of your core business, whether it is residential or asset loans, but also create new opportunities with clients and professional connections,” Vasta says.

“[Diversification] not only puts the client in a better position, whether it is debt consolidation or gap funding, but it also helps the broker form even stronger relationships with their client.”

MoneyPlace offers a wide range of loans: for debt consolidation and gap funding; loans for medical and cosmetic products, recreation products and assets such as cars, boats and trailers; loans for solar panels, renovations and more.

“Our motto is as long as it is a legal purpose and the transaction makes sense, we will be able to help your client,” Vasta says.

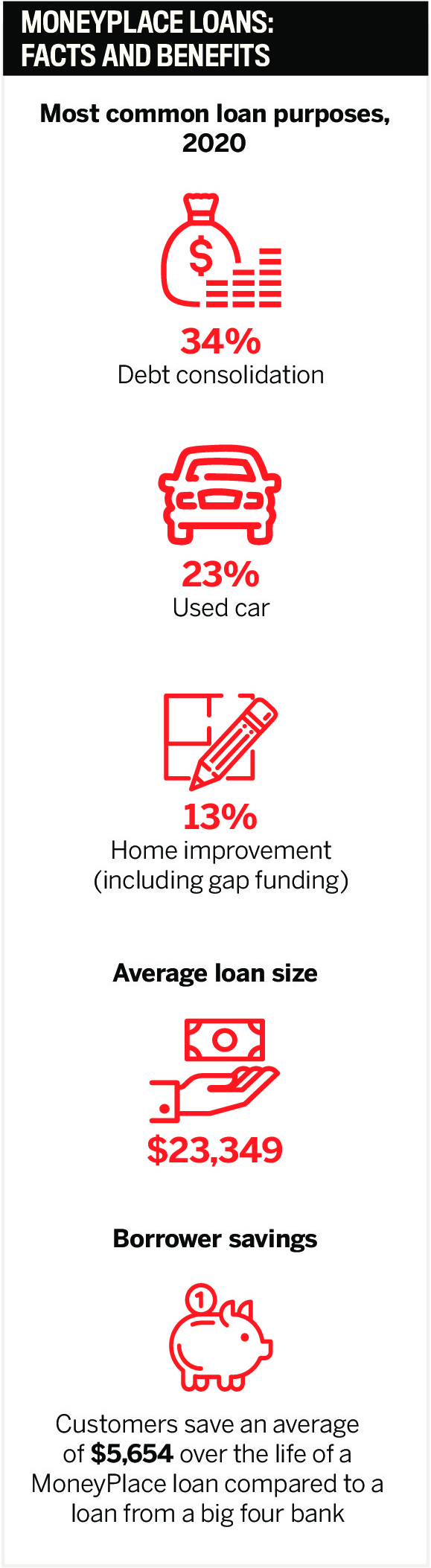

He adds that during COVID-19 the most common loan purpose has been debt consolidation as customers get their finances in order.

“On average, a borrower saves $5,654 on a personal loan with MoneyPlace compared to having a loan with a big four bank. Through COVID we saw brokers help their customers to get into a lot stronger financial position by reducing interest and also extending loan terms to reduce monthly repayments.”

Vasta says there have been some COVID-19-specific trends in loan purpose too, with a large number of pets having been funded, especially dogs, as more and more people work from home.

“We also funded a horse float and recently a funeral plot.”

There has been a big increase in gap finance and debt consolidation loans because they provide both brokers and clients with certainty.

Loans for recreation products have also increased, including for bikes, campervans, trailers and older cars.

“At MoneyPlace we offer up to seven-year loan terms with no exit penalties, no early repayment and no monthly fees. This allows clients to use structured payment strategy and improve their cash flow.

“We often see this as a direct benefit to the customer as we consolidate multiple credit cards, other personal loans and even tax debt. Brokers can confidently get clients on to a structured payment to help them down the track, especially if they are looking at a future property purchase.”

With more people wanting to renovate their homes, there’s a desire for quick finance, but Vasta says brokers often tell them that lenders’ service-level agreements for residential loans can be up to 20 working days and much longer for top-ups.

“Usually when clients are looking for top-ups, especially for renovations, they want the funding pretty quickly. Many customers also don’t want to go through a mortgage refi for the sake of an additional $50,000 to $60,000.”

Vasta says brokers can use a MoneyPlace loan to fund renovations within 24 hours. Once the renovations are complete, brokers can lodge the top-up as there are no exit penalties or monthly fees.

The benefits for brokers include “not running the gauntlet of whether the valuation will stack up” – as well as a quick start to renovations.

“You are also more likely to get a higher property valuation once the renovations are completed,” he says.

Gap funding loans help clients enter the property market sooner, Vasta adds.

“We often see clients with good income and strong employment fall short on the funds to complete because of where current rent prices are at. By offering a MoneyPlace personal loan the broker can help their clients borrow for the stamp duty, legal costs or even funds to complete.”

The lender also helps clients who have shortfalls in valuation which push the LVR above 80%.

Rather than pay lenders mortgage insurance at a high premium and have a higher interest rate with an LVR above 80%, clients can take out a personal loan to keep the LVR at 80%, avoid paying the LMI premium and have a lower mortgage rate.

Vasta says the client can pay out the MoneyPlace loan at any stage without penalty, such as a few years later when they refinance their mortgage.

He is urging brokers to introduce personal loans into their portfolio, with benefits including increasing revenue streams, working directly with clients to provide transactional or holistic solutions, and placing clients in a better financial position.

“It not only creates additional revenue streams but also allows a broker to convert more of their core business,” Vasta says.

“I often tell brokers, if they are stuck with a transaction, can a personal loan help?”

By not offering personal loans, brokers risk losing clients to competitors, he says.

“We constantly see brokers come to us retrospectively, saying ‘I just lost this client so now I want to get informed about personal loans’.

“My recommendation is for brokers to take action now.”

Vasta says MoneyPlace has been educating brokers about the personal loan market and the services the lender provides – from BDM support to its head office broker support team and direct access to decision-makers.

“We run many face-to-face sessions with brokers and regular virtual sessions and webinars to help brokers grow their client base and convert more of their core business. We also have marketing support to help brokers market to their client base.”

Mhairi MacLeod is the founder and principal of asset finance brokerage Astute Ability Finance Group on the NSW Central Coast.

She has been broking personal loans for 22 years and MoneyPlace has been on her lenders panel for the past two years.

MacLeod says many brokers think personal loans are arduous and time-consuming, but diversifying is not only good for their business, “it’s fabulous for their clients”.

“I think personal loan lending is going to get a lot stronger over the coming 18 months, due to people wanting to look at debt consolidation,” she says.

MacLeod praised MoneyPlace’s lending policies, technology and platform.

“It’s straightforward, it’s clear; you’ve got clear pathways to BDMs, you can always get hold of someone.

“It’s not all robotic and online. You actually get to speak to real humans that make real decisions and make common-sense decisions.”

MacLeod says a $26,000 MoneyPlace loan for one of her clients was recently funded in less than 48 hours.

“That’s not only service on behalf of the broker delivering to the client but it’s more exceptional service from the lender to the broker. This customer was stoked. Not taking away from major banks, but their time delays are 10 days or more.”

MacLeod says brokers should consider their clients’ other needs, as people are taking out loans for debt consolidation and home office space or education courses to change careers.

“This is where brokers can actually utilise this personal loan space and still have the ability to provide a good service,” she says.

“The customer experience is awesome when you can use lenders that have this technology.”

MacLeod says MoneyPlace’s support is amazing – she and her team got to meet its BDMs and loan assessors.

“They walked us through every part of their product and the customer experience.

“I think that’s really important when you are choosing a lender of any kind – it’s understanding what the experience looks like for the customer after you’ve settled the deal. MoneyPlace have demonstrated that really, really well to me as broker.”

MacLeod says she gets many loan referrals from other brokers, but if they thought about it and worked with MoneyPlace BDMs, they would see it’s streamlined and not time-consuming.

“I think brokers just really need to give it a shot.”

Albert Lee is director of Sydney personal loan brokerage LendConnect, which assists brokers who refer clients for personal loans.

He says MoneyPlace has reinvigorated how personal loans should be transacted.

“They have a streamlined process with an accurate upfront quoting tool to provide clear transparency of what a potential customer can qualify for prior to applying.

“The partnership and support with open lines of communication has definitely empowered brokers like us with the ability to have a positive outcome for each of our clients and referrers.”

LendConnect’s experience with MoneyPlace has been fantastic, Lee says, especially its approval turnaround times, streamlined technology and communication.

“Approvals are always obtained within two hours, and we have a dedicated credit analyst to partner with us to ensure the client obtains the best outcome,” he says.

“Communication and transparency are key values at LendConnect which are aligned to the team at MoneyPlace. Alf and his team provide a hands-on approach with partners and a focus on achieving the goals of referrers alike.”

Lee says brokers who do not offer personal loans run a real risk of their clients looking elsewhere for finance, damaging their income stream and client relationships.

“Clients could connect with their own bank to obtain the personal loan they require. This will provide the bank with the opportunity to cross-sell a mortgage directly.”

Lee says that as a specialised personal loan business LendConnect spends time with each client to understand their personal loan needs, and it uses its experience to connect clients with the best loan offer.

“When a broker is unfamiliar with the process or not specialised in personal loans and attempts to transact directly with a lender, it may become strenuous,” he says. “This will often lead to a negative client experience and harm the client-broker relationship.”

Lee says brokers can be assured that a loan obtained via LendConnect will be efficient, transparent and executed with ease.