The Commonwealth Bank of Australia has lost market share in the mortgage market for three consecutive months marking the first time in two decades that Australia's largest lender has seen a quarterly decline in its home loan portfolio.

As competition heats up for a slice of the mortgage market, does CBA’s slide signal a changing of the guard or is this only a temporary blip in a history of steady growth?

Three mortgage brokers, who asked to remain anonymous, share their insights on the current state of the mortgage market, the role of the major banks, and the potential implications for the future.

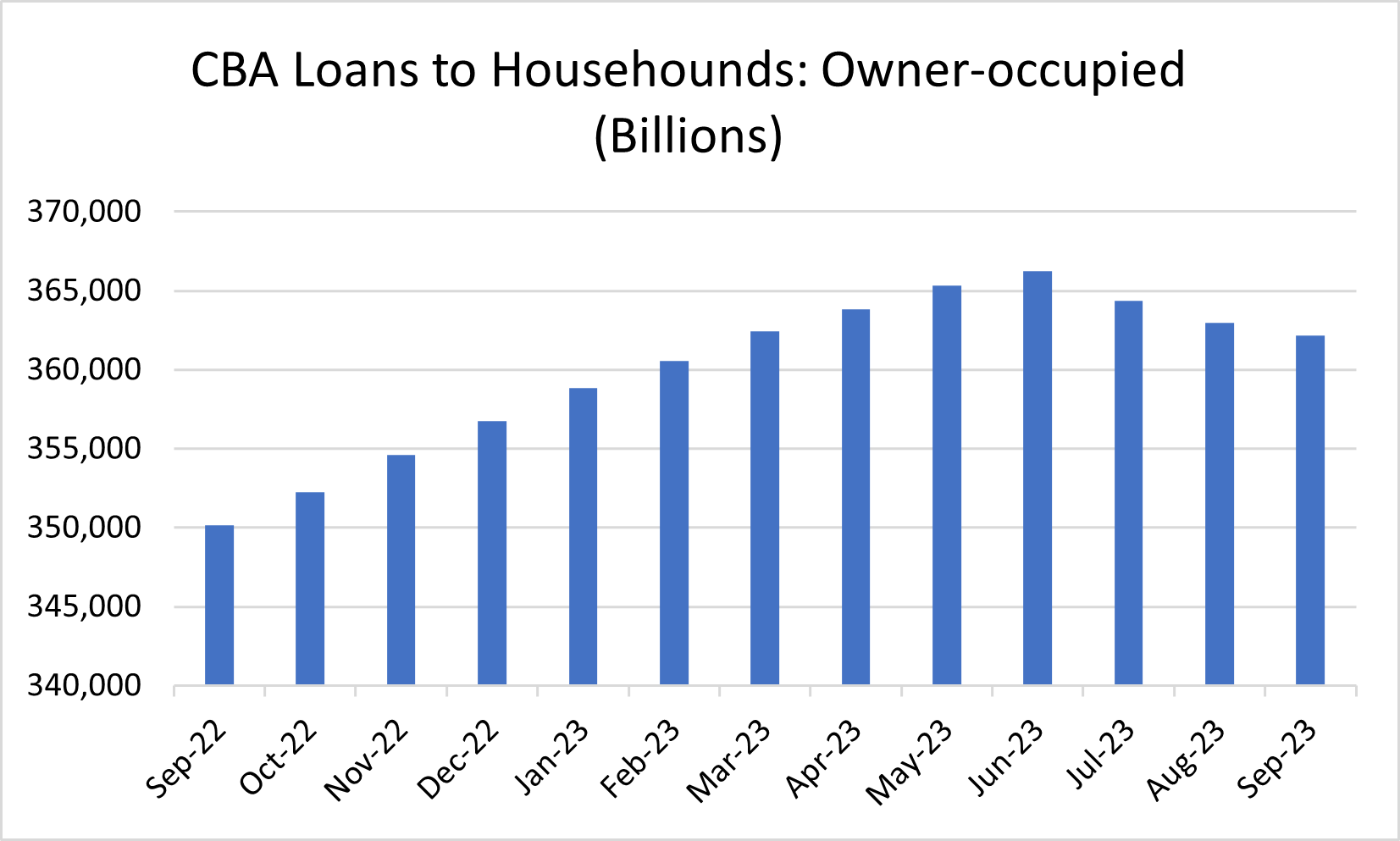

Data from APRA showed CommBank’s owner-occupied loans were worst hit, losing over $4 billion since the end June with a drop from $366.2 billion to $362.1 billion by the end of September.

CBA’s investor loans, which roughly make up half of its portfolio, managed to avoid the same fate after consecutive monthly losses, marginally recovering by $410 million.

Together, this has caused CBA’s mortgage market share to drop from 25.7% at the end of June to 25.43% by the end of September.

While the percentage is marginal, it leaves a significant space to fill in a $2.13 trillion market.

Conversely, the rest of the big four made considerable gains.

These gains inevitably increased their market share, with Westpac (21.3%), NAB (14.6%), and ANZ (13.3%) all making up ground on CBA.

And the rest? The 68 authorised deposit-taking institutions (ADIs) that had written mortgage loans – including second-tier banks, mutual groups, and credit unions - had collectively increased their books by $8 billion over the same period making up 25.1% of the market.

Overall, this still means that CBA has more mortgage market share than 68 banks combined excluding the other three major banks.

However, to put the consecutive slide in perspective, out of the 185 months between March 2004 and June 2019, CBA had only eight months where its mortgage portfolio declined.

Originating nearly 70% of residential loans, mortgage brokers perhaps have the best understanding of what’s happening in the mortgage market.

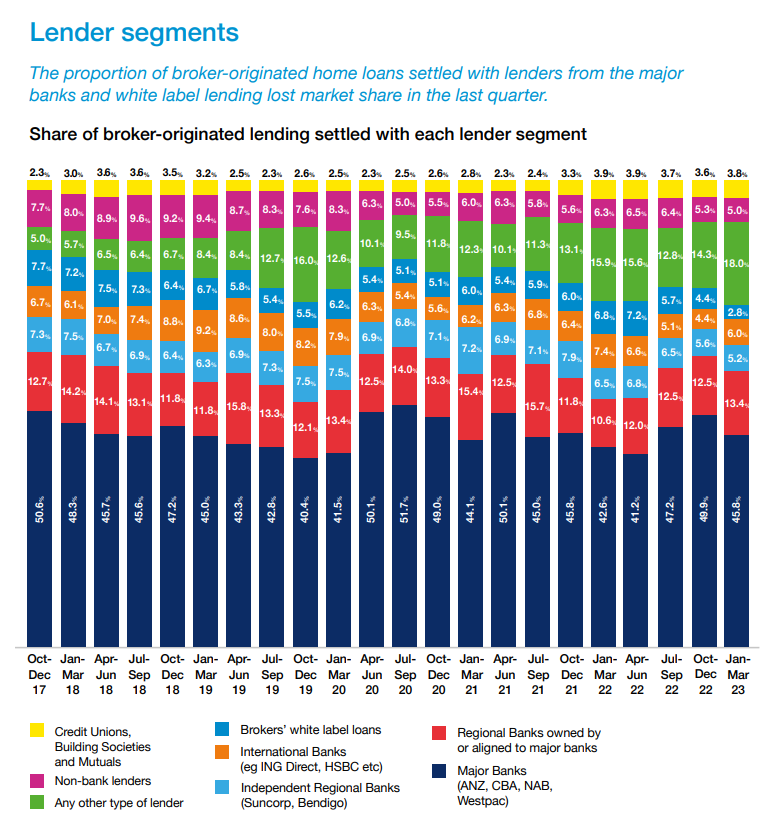

Even at the height of the mortgage wars, where lenders were offering cashbacks and cutting rates, the major banks saw a decline in broker-originated lending from 49.9% to 45.8% between the December 2022 quarter and March quarter of 2023.

However, when including their regional affiliates, the big four still wrote 59.2% of the broker-originated market in the March quarter, according to the latest MFAA Industry Intelligence Report.

Australian Broker has heard anecdotally from three brokers that the big four banks are still relatively competitive from a rates perspective, but that there are also other lenders out there with compelling offers.

One broker said lenders like HSBC, ING, and Qudos had consistently low rates, and others, such as Athena, which had larger borrowing capacities due to their buffer rate, had “very compelling” interest-only options.

“In this tough economic environment where every dollar counts these savings can be the difference between staying afloat or going under,” the broker said.

“I’m not one to only offer the big four and Macquarie … I’ll go as far or wide as I need to help my clients.”

A different broker said now that cashbacks were generally off the table, it was a “more even playing field” for lenders to compete for business.

“Right now, a sharp rate is everything,” the broker said. “Yes, the mechanics of the product need to stack up and yes you need to ensure that the loan product can work for the client in ways other than rate – but if all of that is even, rate is everything.”

The third broker said he had found more people were comfortable with going outside the major banks, which was “a great thing”.

“The old ‘you need to be with the big four for security’ is something I’m hearing less and less, and it certainly makes less sense than it did back in the day.”

However, he acknowledged the big four were a “key part of the mortgage industry” because the larger institutions could take bigger risks on policy which frees up the flow of money for housing.

“We shouldn’t actually want them to drift into obscurity, as their size actually has great overall benefits for the mortgage market and obviously other benefits economy wide.”

Overall, all three brokers agreed that CBA's market share drop is likely due to its pricing strategy.

They all mentioned that CBA's rates have been less attractive than other lenders in recent months, despite being “among the best” policy-wise.

“I love CBA. They are one of my biggest lenders but of late they have had very unattractive rates on offer and have offered poor revert rates for clients coming off their fixed rates,” said one broker.

Another broker said that during the middle of the year, CBA’s pricing for new customers was “quite expensive”, which would have then led to a decrease in new loan applications during that time.

“I know there were several occasions where CBA would have been up there and possibly the best option policy-wise for a client but due to poor pricing they weren’t the best overall choice for the client.”

With full year results season starting next week, the major banks have so far avoided commenting on their mortgage strategy recently.

And while all eyes are on CBA’s senior executives to see what’s next, the major bank has been far from idle.

In the few months after posting record growth in its asset finance division, Commonwealth Bank partnered with Tesla and enabled open banking.

Still, CBA’s mortgage strategy in the coming months is likely to have major ramifications to borrowers, brokers, and the mortgage market in general.