Homeowners continue to face challenges following increases over the previous months. Borrowers with a variable rate loan have been described to have been “feeling the pain of 12 rate hikes on a month-by-month basis.”

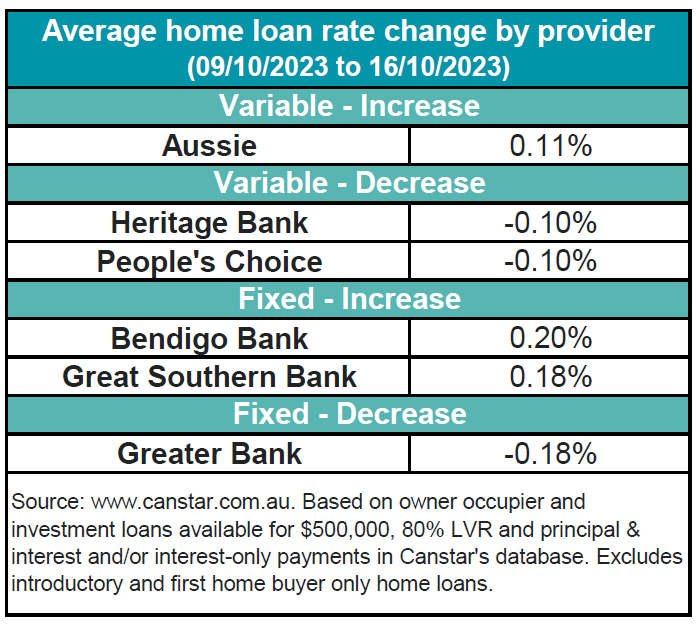

Aussie increased two owner-occupier variable rates by an average of 0.11%, while two lenders cut 12 owner-occupier and investor variable rates by an average of 0.1%. Two lenders increased 35 owner occupier and investor fixed rates by an average of 0.19%. Greater Bank cut 24 investor fixed rates by an average of 0.18%.

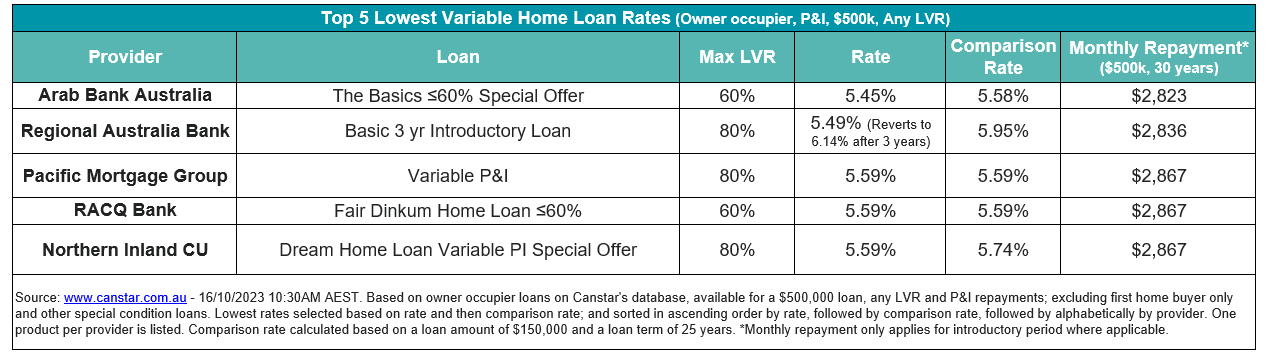

The average variable interest rate for owner occupiers paying principal and interest is 6.68% for 80% LVR, while the lowest variable rate for any LVR is 5.45%, which is offered by Arab Bank. There are eight rates below 5.5% on Canstar's database.

Source: Canstar

Effie Zahos (pictured above), editor-at-large and money expert at Canstar, said those with fixed-rate loans will have to endure “the pain in one fell swoop” when their fixed term comes to an end.

“Mortgage cliff or not, the pain of rolling off rock-bottom rates to budget-busting interest rates will put a whole new lot of households under financial strain,” said Zahos.

Zahos suggested a three-step plan for borrowers looking for options. “If your fixed-rate loan is coming to an end, the good news is that you have options. You don’t have to get stuck with a sky-high variable rate. It’s important to have a plan in place. Ideally, you need to start exploring your options at least one month before your fixed term is due to end,” she said.

Step 1. Compare. Borrowers are advised to ask their lender what rate they will be paying when their fixed term expires and then to check how this “stacks up” against loans from other providers.

“There's a massive difference of 1.19 percentage points between the cheapest variable rate with 80 percent loan to value ratio on Canstar’s database at 5.49 percent and the average variable rate at 6.68 percent. On a $500,000 loan over 30 years, that's a difference of about $380 on your monthly repayments. You may also want to look into what fixed rates are on offer,” said Zahos.

Step 2. Choosing the loan: “Fixed, variable, or both?” Borrowers are advised to decide on whether they would want a fixed rate.

“The cheapest one-year fixed rate with a 80% loan-to-value ratio on Canstar’s database is currently 5.70%,” said Zahos. She said it would be worth asking for a rate lock facility if borrowers decide to lock in. She noted borrowers also have the option to hedge their funds and split their loan between fixed and variable.

Step 3: “Stay or move?” Borrowers are advised to decide whether they would like to stay with their existing lender or to try out others.

“If you plan to refinance to a new lender you’ll need to ensure you have all your financial details at hand. This could include payslips, tax returns and bank statements,” she said.

Have thoughts about these insights? Leave your comments.