By

With the government proposing to legislate changes to the clawback period, the industry is calling for the future arrangements to become fairer still. Australian Broker examines the proposed changes and the impact of clawbacks on brokers’ businesses

Responding to recommendations of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, the government recently consulted on the best interests duty and remuneration reforms for mortgage brokers.

The National Consumer Credit Protection Amendment (Mortgage Brokers) Bill 2019 includes proposed measures to limit the period in which commissions can be clawed back from brokers to two years, and to prohibit the cost of clawbacks being passed on to clients.

The industry was asked for feedback on the proposals in the draft bill, which outlines the best interest obligations of mortgage brokers as recommended by Commissioner Kenneth Hayne in the final report of the royal commission.

But with the government expected to table its best interests duty bill in Parliament before the end of the year, Peter White, managing director of the FBAA, says he is pushing for further amendments to be considered, including revisions to existing clawback arrangements.

If passed, the regulations are due to take effect on 1 July 2020.

Shorter clawback period

Many in the industry are calling on the government to reform the clawback period and bring it down from two years – as proposed by the draft bill – to 12 months.

Currently, many credit providers have clawback arrangements with aggregators, which in turn have arrangements with brokers allowing credit providers to recover some or all of the commission paid by the lender to the aggregator if the loan does not continue beyond the minimum ‘clawback period’.

The aggregator will then claw back the commission from the broker, with some brokers even passing on clawback fees to their clients.

This arrangement was initially designed to discourage brokers from refinancing or ‘churning’ consumers to a new lender, since the broker can potentially earn a new upfront commission with a new lender, adding costs to lenders and ultimately consumers.

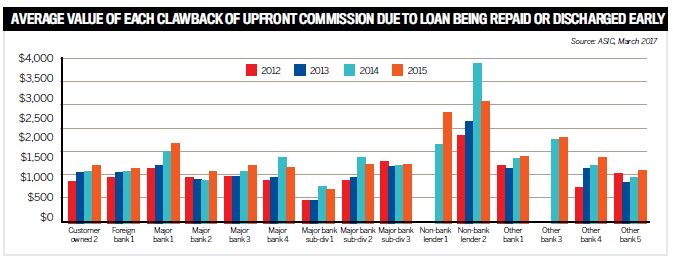

According to the latest Review of Mortgage Broker Remuneration report by ASIC, lenders typically recovered between 4% and 10% of upfront commissions as a result of their clawback arrangements.

The findings also showed the average value of upfront commissions recovered across all lenders exceeded $1,000, and for two non-bank lenders this was nearly $3,000.

But some brokers can lose up to 100% of the original commission, with some also passing on clawback fees to clients.

“Mortgage brokers can have a clause in place that they hand to clients when they’re doing the mortgage application, and in the clause you can say there’s a clawback fee,” explains Louisa Sanghera, managing director at Zippy Financial.

“But not everyone does that.”

But clawbacks could also be discouraging mortgage brokers and their clients from exploring new and better loans, as they add to the cost of switching products, and so many are calling for clawbacks to be scrapped, or at least shortened down to a fairer period, when loans are the least likely to be refinanced.

For example, White has been backing the implementation of fairer clawback arrangements, saying the existing arrangements of up to two years “are unfair” because “no one should be at risk of losing the money that they’ve rightfully earned”.

But if the current bill is passed, mortgage brokers could be at risk of losing upfront commissions for up to two years.

“Lenders would have the right to take that money off them for up to two years if the loan terminates early,” reiterates White.

However, if the original loan is terminated because the broker did something wrong, for example churning out loans, then White says “you get what you deserve for that”.

But most clawbacks occur after a client experiences a big life event, like moving overseas for work, etc, within the early years of the loan being taken out, so it’s usually outside of the broker’s control.

In such instances, brokers could lose money for “just doing their job”, which “is ludicrous’’, says White.

He continues: “The productivity commission identified that as a risk – for brokers acting in the best interest of the client – because you may not look after the client in the right way if you’re worried about losing all the money that you’ve earned.”

But with the government expected to table its best interests duty bill before the end of the year, it is difficult to say what the final bill will look like.

“Nothing is guaranteed until it’s done,” says White.

While it is unlikely that clawbacks will be scrapped altogether, he says there is very real hope for the time frame to be brought down to one year.

Whatever the outcome, White says brokers should not be discouraged and should instead focus their energy on the opportunity for growth presented by the best interest duty bill, especially when it comes to cultivating greater accountability and transparency across the industry.

Focus on client outcomes

Whatever commission structure the industry lands on, it should enable customers to move around in a way that gets them on the best deal as regularly as possible, according to Anthony Justice, CEO at Uno Home Loans.

“We should always be thinking about the customer and how to make sure they get the least friction in the market and are on deals that are within their best interests all the time,” says Justice.

But clawbacks could be discouraging brokers from refinancing customers in the first couple of years, when there might be better deals out there for them.

“It reduces the incentive for a broker to actively move somebody to a new lender for the first couple of years,” explains Justice.

“Anything you can do to remove the friction for the customer switching to a better deal is a good thing, and removing or reducing clawback would certainly help that,” he adds.

But what’s tricky is that there is no way to know when clients’ circumstances might change, which could lead to clawback, suggests Sanghera.

“When my clients take out a mortgage, they don’t know that they might be divorced within 12 to 18 months, or they don’t know that they’re going to move with a job.

“I had a client who within three months of doing his mortgage moved to Queensland with his job and bought a new house in cash because house prices are much cheaper there, and I needed to pay all my commission back for the initial loan,” she says.

“This was a second example where a Westpac member of staff settled with us and within months moved his mortgage over to a staff deal and I got clawback on it.

“I worked on that mortgage in good faith and actually took a loss; it cost my business, and the client felt terrible as well. How can that be fair?”

There has also been some argument that instead of brokers shouldering 100% of the burden, some of it should be passed on to the banks.

“I’ve had clawbacks that have really hurt me … the banks are much bigger businesses than us; it would be better to share the hit and the loss, rather than taking 100% off of the broker,” says Sanghera.

Struggle for small businesses

It can be especially difficult for smaller brokerage firms to plan for clawbacks.

“If you’re running a business, how do you provision for that on your balance sheet? You’ve got a risk there that could hit you at any time, so it’s very challenging from a business point of view,” explains White.

While clawbacks were put in place to stop brokers from churning mortgages, Sanghera argues that this is such a small portion of the industry it does not reflect the true nature of the profession.

“It makes it extremely difficult to manage cash flow … it’s an administrative nightmare,” she adds.

“We need to focus on looking for those brokers [churning mortgages] and not punishing the whole industry … I welcome the 12-month clawback period rather than 24 months; it’s a step in the right direction and a small win for brokers.”

But if the draft bill is not finalised and passed by early December, it is likely to be pushed out to next year.

“There must be another system where they can monitor brokers with high volumes of mortgages within a short time frame. Clawbacks should be scrapped,” Sanghera says.

Industry expects the legislation to take effect by July 2020.