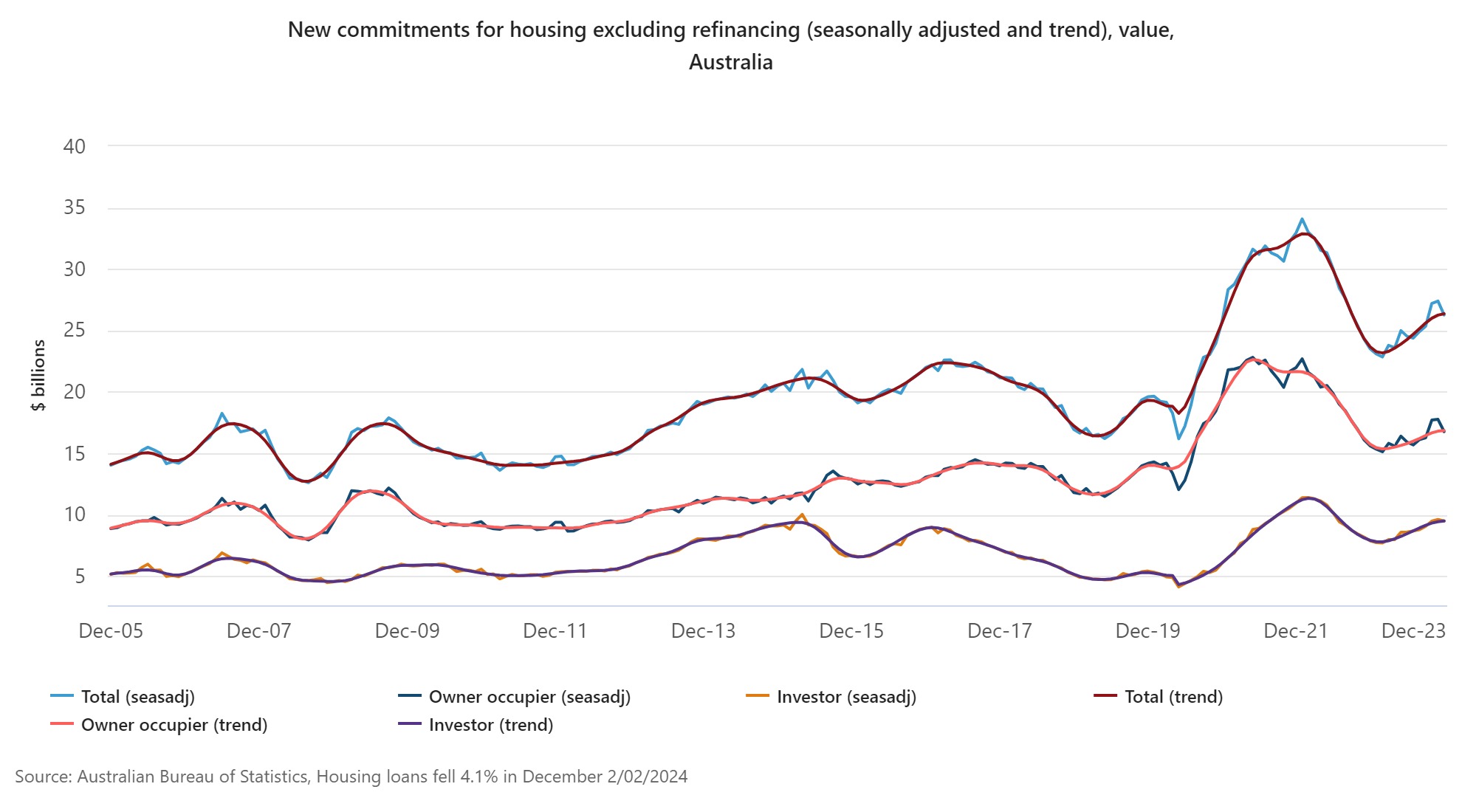

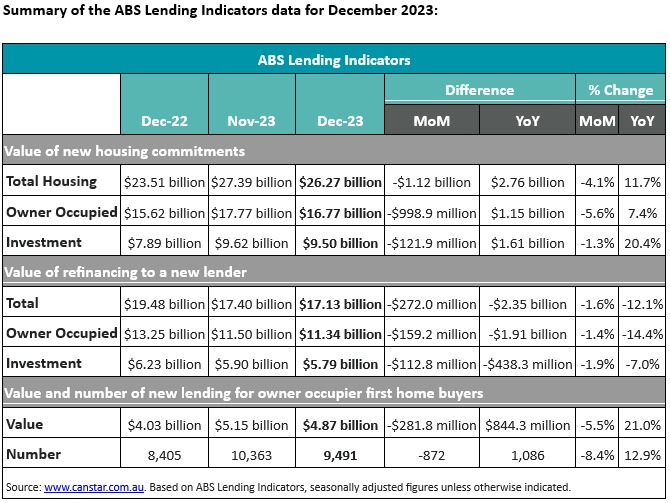

Australian housing loan growth screeched to a halt in December, according to the latest data from the Australian Bureau of Statistics (ABS). The total value of new commitments for home and investment properties fell by 4.1% compared to November, marking the first decline in five months.

Both owner-occupiers and investors appeared to hit the brakes, with owner-occupied loan commitments experiencing the most significant drop, decreasing by 5.6% to $16.77 billion. This ends a four-month period of consecutive growth for this segment.

Investor lending also witnessed a moderate decline of 1.3%, reaching $9.50 billion, representing the first downturn in ten months.

The value of loans to first home buyers broke a four-month trend and was also down for the first time since July by 5.5% over the month to $4.87 billion in December.

Canstar’s lending expert Steve Mickenbecker (pictured above) said the promising recovery in new lending over the last few months had proved to be a “false dawn” with lending to owner-occupiers being a major drag on the market only up 7.4% since December 2022.

“Even last month’s star performing investment lending was down, but by a relatively modest 1.3% for the month, leaving it still a healthy 20.4% above December 2022. Investment recovery looks to be sustainable on the back of the 2023 recovery of house prices and investors’ expectation of future price appreciation,” Mickenbecker said.

Housing prices reported by CoreLogic show a strong recovery over 2023, to the point where Brisbane, Perth and Adelaide are at 2021 highs.

But the softening over the past couple of months in the biggest markets in Melbourne and Sydney may suggest that demand is off in spite of rental and immigration pressures.

“The decline in inflation for the December quarter should lift the lending market this year, boosting buyer confidence that they no longer have to anticipate a further rate increase and just have to show a little patience for a rate cut later in the year,” Mickenbecker said.

The value of existing loans refinanced to a new lender in December fell by 1.6% when compared to November, which coincided with the most recent Reserve Bank cash rate rise. A total of $17.13 billion in loans were switched to a new lender at the end of the year, which is a far cry from the $21.5 billion at the peak in July 2023.

Canstar’s analysis shows the 4.25 percentage point increase in the cash rate since April 2022 adds approximately $1,562 to repayments on a $600,000 loan over 30 years or $2,603 on a $1 million loan.

Once the November rate increase flows through to borrowers’ repayments in the coming months, Mickenbecker said we could see another uptick in refinancing activity.

“Fewer existing borrowers were seeking out a better deal in December despite the Melbourne Cup rate rise still fresh in their minds,” he said.

“It can take around three months for rate rises to flow through to repayments, and when November's hike does hit it will hopefully encourage borrowers to pick up the phone to their lender to negotiate a better rate or make the switch to a new lender.

“The impetus for mortgage holders should be to look for a repayment cut now and not wait around for the Reserve Bank to make its call on rate cuts.”

Where do you think the housing loan market is heading? Comment below