By

Dwelling prices appear to have recovered from the declines caused by the COVID-19 but some markets have managed to defy the overall downturn from the onset of the outbreak, according to the latest study by CoreLogic.

Over the last quarter of the year, dwelling prices rose by 2.3%, reversing the decline in September. The dwelling prices in March last year could provide a good gauge for measuring the impacts of the outbreak on prices.

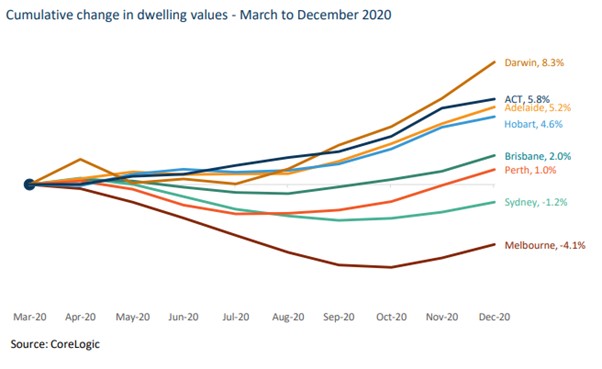

Looking at the movement of prices in capital cities, Melbourne, Sydney, Perth, Brisbane and Hobart reported some level of value falls close to the onset of the outbreak. By December however, housing values in Perth, Brisbane, and Hobart had surpassed their March 2020 highs.

Still, three markets emerged to have had consistently registered increases in house prices since the onset of the pandemic — Darwin, ACT, and Adelaide.

According to CoreLogic data, of the 95 LGA markets that witnessed a decline since the onset of the pandemic, 37 have already surpassed their levels in March last year. Some of these markets include Kwinana in Perth, Burnside in Adelaide, and Scenic Rim in Brisbane. These three markets have registered increases between 6.5% to 8.7%.

The report said most of the markets with a strong recovery had seen relatively mild downturns during the pandemic. Sydney’s Central Coast is a good example. Dwelling values in this market have declined by just 0.1% in April. However, they have increased 6.5% through to December since March.

Of the 10 regions where values have been the most impacted, eight were in Melbourne, which was affected by the extended period of lockdowns and restrictions. Inner-Melbourne council areas, according to the report, may be at greater risk of negative equity for recently purchased homes.

Still CoreLogic projects that more markets are likely to move into recovery mode, especially if economic conditions continue to recover and mortgage rates remain at record lows.