In the wake of the Reserve Bank’s recent cash rate hike of 0.25 percentage points, several mortgage rates have moved as Australian borrowers continued to grapple with increased home loan rates, according to Canstar.

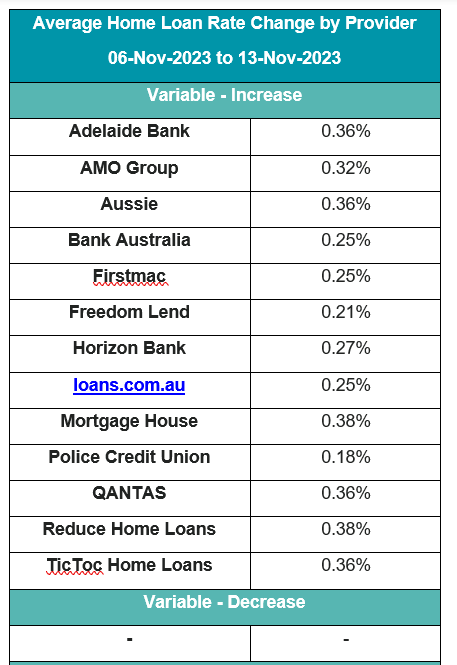

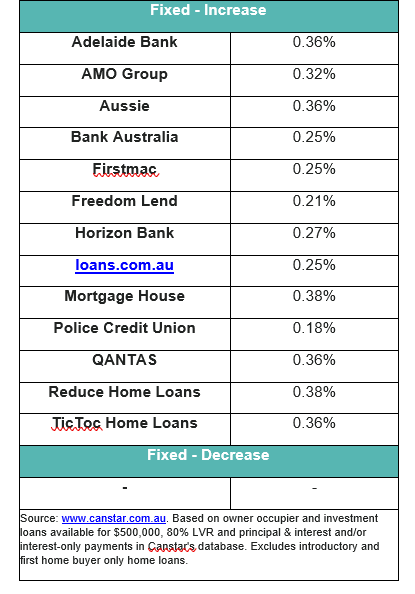

Over the week of Nov. 6-13, eight lenders increased 66 variable rates for owner-occupiers and investors by an average of 0.25%, while 13 lenders raised 288 fixed rates by an average of 0.32%, Canstar’s interest rates week wrap-up showed.

See table below for the lenders that made fixed and variable rate changes.

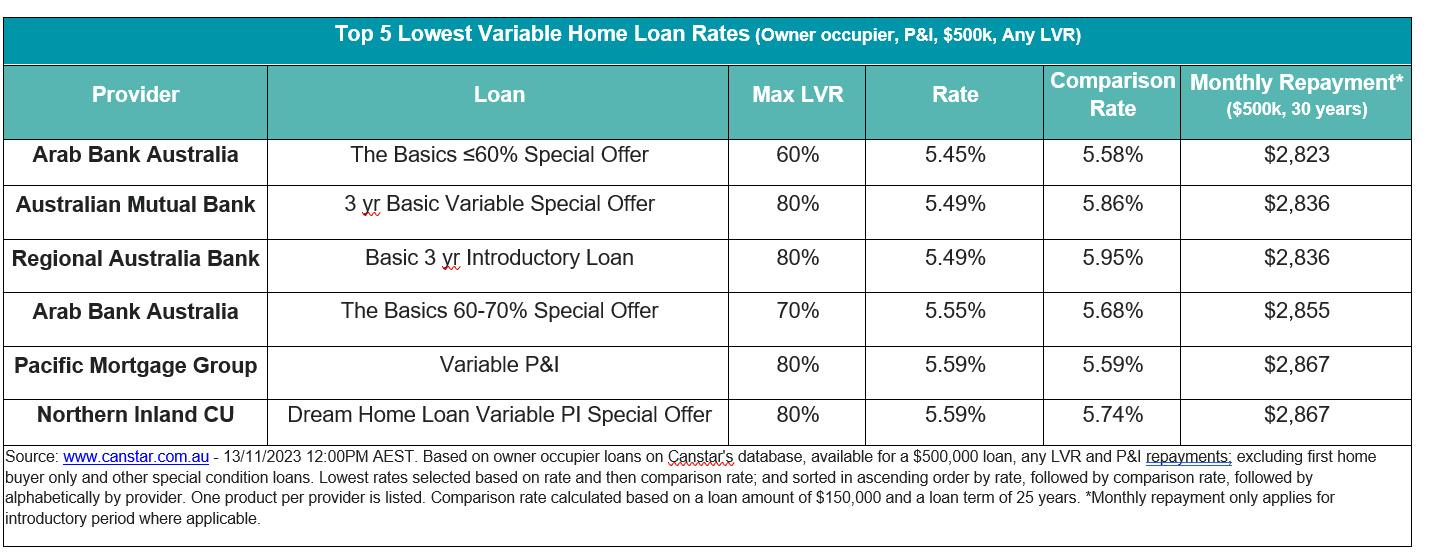

Following the week’s changes, the average variable interest rate for owner-occupiers paying principal and interest stands at 6.7% for an 80% LVR. The lowest variable rate, at 5.45%, is offered by Arab Bank for up to 60% LVR.

Canstar’s database revealed eight rates below 5.5%, maintaining consistency from the prior week. These rates were from Arab Bank Australia, Australian Mutual Bank, LCU, RACQ Bank, and Regional Australia Bank.

See table below for the lowest owner-occupied variable home loan rates on the Canstar database.

“It’s been one week since the Reserve Bank of Australia raised the cash rate by 0.25 percentage points to 4.35%, making it the thirteenth hike in 19 months,” said Effie Zahos (pictured above), Canstar’s editor-at-large and money expert.

“The November cash rate increase will add roughly $100 to the monthly repayments for borrowers with a $600,000 mortgage.”

Zahos suggested three swap-and-save strategies to counteract the financial impact of the November rate hike.

Borrowers can potentially save $465 per month for a $600,000 mortgage at the average variable rate of 6.7% by switching to the cheapest one-year fixed rate on Canstar’s database, at 5.5%, available to those with 60% LVR or less.

For borrowers with an 80% LVR, they could also secure a competitive one-year fixed rate of 5.7%, reducing repayments by $390 per month.

“While there are pros and cons to consider when locking in, this strategy has the potential to provide immediate relief and, given the latest forecasts from the big four banks don’t anticipate a rate cut until September 2024 at the earliest, there may be more advantages than disadvantages,” Zahos said.

With 281 variable rates and 178 fixed rates below 6% on Canstar’s database, Zahos said there are still many opportunities for borrowers to score a great rate.

For borrowers with a 60% LVR or less, switching from the average variable rate of 6.7% to the market's cheapest variable rate at 5.45% could potentially cut monthly repayments by $484 for a $600,000 loan.

Those with an LVR of 80%, meanwhile, can refinance to the cheapest ongoing variable rate of 5.59%, saving them $431 in repayments a month.

Borrowers can also consider switching to a basic style home loan with fewer features but a cheaper rate.

Canstar’s analysis revealed a 0.32 percentage point difference between the average variable rate and basic home loan rate, translating to potential monthly savings of $127 on a $600,000 loan.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.