By

2019 IN REVIEW

Regulation and compliance

The biggest news this year was the release of the final report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

While not specifically a change to lending, the final report did put a spotlight on the lending industry as a whole and highlighted a need for change, according to Daniel Carde, general manager of third party distribution at Resimac.

There were a number of key releases from APRA, ASIC and Treasury, for example ASIC’s consultation paper requesting feedback on proposed updates to the responsible lending guidelines.

“These proposed changes were twofold,” Carde explains. “Firstly, ASIC are proposing to update the regulations to better align them with recent advancements in technology (for example, recognising bank-statement scraping for data collection), and secondly they are looking to provide additional guidance around some of the existing regulations (for example, what level of enquiry should be made into verifying living expenses).”

APRA also released updated guidance on mortgage serviceability assessments for authorised deposit-taking institutions (ADIs), which had been in place since December 2014. This effectively allowed lenders to set their own assessment rates.

Carde continues: “Many lenders, Resimac included, took the opportunity to review their assessment rates, with the majority lowering the assessment rate to be more in line with the current low interest rate environment.”

Treasury also released the first bill to be introduced as a direct result of the royal commission: the Financial Sector Reform (Hayne Royal Commission Response – Stronger Regulators (2019 Measures)) Bill 2019.

The bill was introduced into Parliament earlier this month, implementing recommendations 1.2 and 1.3 of the royal commission, including a best interests duty (BID) for mortgage brokers.

Sourcing appropriate loans for customers’ needs also became more demanding over 2019, as was the requirement to document and articulate the ‘why’, according to Aaron Milburn, general manager of mortgages and commercial lending at Pepper Money.

“Across the industry, whether it was a family looking to refinance their mortgage or a small business owner seeking a loan to support their business, lending conditions were difficult and ever-changing,” he says.

Interestingly, Milburn suggests it was actually the threat of more regulation hanging over the lending industry rather than actual legislative changes that created such an impact in 2019.

“But perhaps the biggest change stemming from the royal commission was how swiftly some lenders altered their appetites in 2019, particularly around the assessment of living expenses, which in turn affected turnaround times for those lenders,” he continues.

“Customers relying solely on the big four suddenly found themselves with fewer options, and it fell to the mortgage broking industry to help them find an alternative.

“Luckily, the non-bank sector proved to be more flexible, and better equipped to offer solutions based on the customer’s own unique needs whilst still adhering to the strict regulatory frameworks we all operate under.”

Another by-product of the royal commission was brokers being forced to justify their role in the financial ecosystem, explains Sarah Thomson, senior lending manager at Loan Market, who ranked seventh on this year’s Top 100 Brokers list compiled by Australian Broker’s sister publication Mortgage Professional Australia (MPA).

“Brokers had to show the public what we do, how we do it, our no-cost offering and the ongoing service we provide during the life of our customers’ journey … our value proposition is clearer than ever, now,” says Thomson.

Biggest changes

According to John Mohnacheff, national sales manager at Liberty Financial, there’s no denying that 2019 started on shaky ground, and the Hayne Commission’s recommendations in its final report left many brokers reeling.

“But despite an uncertain beginning, the industry has displayed unrelenting resilience this year and is now stronger than ever before. With businesses and individuals from all walks of life speaking up in the defence of the broker value proposition, we saw resounding support from the Australian community,” he says.

“What started as a threat quickly turned into a triumph as increased media attention, along with the MFAA’s Broker Behind You campaign, highlighted the many benefits that brokers bring to the table.”

For Holly Bundy, director of Bundy Financial Services and another MPA Top 100 Broker this year, a big impact on brokers’ work following the royal commission has been the treatment and assessment of customers’ living expenses.

“ Gone are the days of only using the household expenditure measure [HEM] to mitigate the client’s living expenses; we are now knee-deep, wading through our customers’ statements trying to assess what is and isn’t a recurring expense,” she says.

Gone are the days of only using the household expenditure measure [HEM] to mitigate the client’s living expenses; we are now knee-deep, wading through our customers’ statements trying to assess what is and isn’t a recurring expense,” she says.

While the cost to deliver a great outcome has gone up for brokers, Bundy says brokers’ commissions have remained the same.

“The cost for brokers to deliver great outcomes for clients has gone up tenfold, with more time spent reviewing every transaction and statement for accuracy and missing information,” she explains.

But perhaps the biggest change resulting from the royal commission was the decrease in clients’ borrowing capacity, stemming from changes to lenders’ servicing calculators, Bundy says.

“This is also due to how living expenses are now assessed and what are considered voluntary and ongoing living expenses and how the banks assess these varying greatly between lenders and resulting in confusion among brokers,” she says.

Indeed, APRA’s amendments to interest floors for serviceability assessments marked “a significant regulatory change” that “many lenders across the market took advantage of ’’ says James Angus, chief customer officer at Bluestone.

He explains: “Coupled with lowering Reserve Bank of Australia cash rates, these changes effectively raised borrowing capacity … While a large range of factors plays into the recent recovery of property prices, lower interest rates and higher borrowing capacity should certainly be counted among them.”

Culture shift

The biggest change resulting from the banking royal commission according to Angus has been the dramatic “shift in culture” within financial services.

“The commission identified culture as a ‘root cause’ of misconduct in the financial services industry, describing culture as something which can both drive misconduct and discourage it,” Angus says.

“Commissioner Hayne pointed out that, until very recently, there has been scant overt attention given in Australia to the importance of culture, whether by entities or regulators, but that there are signs of change looking ahead,” he continues.

“As a result, the majority of participants in our industry, if not all, have taken steps to ensure they have effective leadership in place.”

He concludes that an effective leader is someone who drives a culture of embracing oversight, compliance and reports of wrongdoing, rather than ignoring or punishing those who raise concerns.

Ian Rahkit, general manager of third party at Bankwest, says brokers have done a “fantastic job helping people” find the right home loan for their needs and also giving ongoing service and support to their customers.

However, he adds that the question of ‘what does responsible lending look like?’ has become “a key focus for the financial services industry” and, looking back over the past 12 months, “serviceability and assessment has been a key topic of conversation”.

Rise of non-banks and alt lenders

Changes in floor rates, plus a general lowering of interest rates, improved housing affordability over the year.

Nevertheless, ensuring the accurate assessment of a customer’s ability to service a loan is still of paramount importance, Rahkit points out.

“As well as keeping across a number of updates to the HEM tables and ongoing interpretations of expenses, at Bankwest we’re constantly refining how to best assess the borrowing and repayment capabilities of our customers,” he says.

As the big banks have tightened and restricted their lending criteria, this has led to another big change: non-bank lenders providing niche solutions for customers, says Bundy.

“Even something as simple as how income is annualised or how self-employed income is viewed can make a big impact on our customers’ borrowing capacity, and this is why the non-bank lenders have played an essential part this year,” she explains.

Angus agrees that non-bank lenders are certainly taking a larger market share.

“Consumers are tired of the same customer-first rhetoric from banks, and there is clear regulatory intent to constrain banks’ home loan growth over the medium term,” he says.

“Brokers’ recent experiences with non-banks have been generally more positive compared to other lenders.”

Australia currently holds a 32% share of the alternative finance market in the Asia-Pacific region – after its share grew 88% year-on-year – and the total market is worth $1bn, according to recent figures from KPMG.

So non-bank lenders offered more competitive pricing, more reliable processes and more consistently applied policy than the majors, explains Susan Mitchell, chief executive of Mortgage Choice.

“The intense scrutiny of home loan applicant living expenses was one of the biggest changes to lending in recent memory. The depth of information brokers are required to submit when lodging a home loan application saw loan processing times dragged out to an unprecedented level,” she says.

Bundy adds, “We are finding that lending through normal channels has become increasingly difficult for our SME clients. This has opened the door for a range of non-bank lenders and specialised fintechs who have capitalised on where the big banks cannot assist.”

Alex Brgudac, head of partnerships at Prospa, says, “We expect to see more growth and consolidation in the market in 2020, and more companies scaling across geographies and products.

“The rollout of open banking will increase competition and innovation and make it easier for customers to compare and switch from traditional lenders. This will drive increased awareness and consideration of alternative lenders like Prospa.”

Indeed, brokers should make sure they’re on top of open banking and understand privacy regulations, particularly in relation to moving customer information around.

“Trust and customer experience will be more important than ever, and every one of us will need to work hard to keep delivering those ‘wow’ moments for customers,” Brgudac adds.

Meanwhile, Cory Bannister, vice president and chief lending officer at La Trobe Financial, says, “We expect to see continued growth in non-bank volumes over the coming year and beyond, as the current economic and regulatory conditions are accelerating the shift in the near term and, in our view, this is likely to be the catalyst for longer-term growth in the sector.

“In our view, monoline businesses will get left behind in the wake of full-service, diversified operations. The key for brokers is to diversify or risk being left exposed.”

SME lending

Awareness of online lenders as a source of finance has grown significantly over the past year, especially among businesses that have had a poor experience with mainstream banks, according to Cameron Poolman, chief executive at OnDeck Australia.

A recent survey by OnDeck found that one in five (22% of ) SME owners would consider an online lender in the future, compared to one in 10 (11%) who have considered them in the past. Interest in online lenders also rose significantly, to 42%, for those who have previously had an application for finance rejected by a bank.

But a large number of SMEs may not be reaching their full potential because they can’t secure bank finance, or because an inefficient and lengthy lending process is adding to the cost burden, Poolman admits.

He says it is therefore important for small business owners and brokers to realise that more efficient funding options are available through online lenders.

“And with around 50% of SMEs turning to a finance broker to access their capital requirements, brokers shouldn’t underestimate the opportunity presented by this market,” he adds.

“The growth of online small business lending is a win-win for brokers and their clients. It’s not just about brokers broadening their revenue streams, though of course that’s a key benefit.”

My Home Loan’s Darren Liu, first on this year’s MPA Top 100 list, agrees the SME space has seen great growth, but that may not be the case for every broker.

“It’s good for brokers’ clients with business requirements to be able to extend their business to SME lending, but for brokers focusing mainly on residential loans, they will need to spend more time on education and marketing as it is a completely new journey for them. We’ve found that challenging,” he says.

Jean-Pierre Gortan, MD of Marketplace.finance, points out that SMEs make up a substantial percentage of GDP, supporting the health of Australia’s economy, so it’s important that they continue to have access to capital.

“Growth in this sector has been steady thanks to the assistance of new fintech entry players like OnDeck, Prospa and now new bank competitors like Judo,” he says.

Nevertheless, while there have been plenty of enquiries about SME lending, it’s been harder to secure, especially for start-ups, Thomson says.

“The federal election result in May was unexpected, and that created a bump in confidence at the start of the new financial year. But again, banks were acting with caution when assessing applicants. More lenders are coming into this space, which will add healthy competition,” she says.

LOOKING AHEAD TO 2020

Best interests duty

The broker industry has had a challenging year, but it has also adapted to many of the changes in order to continue providing the services many customers value so highly, according to Rahkit.

Looking ahead, he says three pieces of legislation will be paramount: the best interests duty, net of offset commission, and broker information sharing – all currently signposted to be live from 1 July 2020.

“These pieces of legislation will undoubtedly strengthen the sustainability of the industry but will also require a tremendous effort from all. I look forward to seeing the industry come together to support their implementation,” says Rahkit.

But many brokers are already trying to get ahead of the curve and implement things they believe will be necessary and required as part of the BID, suggests Bundy.

“Having the right processes to record and document your conversation with the customer and ensure that all the essentials are not only discussed with your customer but also communicated to them in writing and documented in the BID will be essential in 2020, giving customers more ownership and control of their information and how it is communicated to the banks,” Bundy says.

She believes that “an amortised clawback of commissions to brokers would be more appropriate, instead of 100% in the first year and 50% in the second”.

Over the past few months the industry has been busy providing input on the National Consumer Credit Protection Amendment (Mortgage Brokers) Bill 2019 and preparing for the introduction of BID, says Anja Pannek, CEO of PLAN Australia.

Importantly, she predicts this will be a key focus as the industry heads towards the legislation’s July implementation.

“We’ve already been engaging with members on this and will continue to work closely with them to understand updated responsible lending guidance and navigate through any changes,” Pannek says.

“The introduction of a best interest duty is likely to be a game changer for the industry. Borrowers will be able to go to a broker and know they are bound by law to act in their best interests – a change we believe will help to build even greater trust in our industry.

“This aligns closely with what we have been talking to members about and how we know our members operate their businesses, understanding the importance of placing customers at the centre of everything broking businesses do. We encourage brokers to analyse their customer base, process and team and look for ways to make their businesses as customer-centric as possible. We see this as a crucial ingredient for long-term broker success.”

Technology

Pannek also predicts that technology will have a key role to play in customer-obsessed broker businesses, with the CRM “providing opportunities to surprise and delight the customer” by “enabling better communication between broker, lender and customer, and facilitating longer-term relationships with customers”.

Gortan says technology will be the “next biggest disruptor for the broking industry”, and that brokers who do not embrace it will be “left behind fighting” for scraps.

“There is a current industry demand for greater business diversification that I don’t think we will see go away any time soon, so it’s important for residential brokers to develop their skills and market share in the commercial space, and embrace new technology and platforms that will enable them to fulfil the current gap so that they are not left behind,” he reiterates.

“Brokers and referrers who draw most effectively on these new ways of working to upskill and create a new service proposition will be best placed to sustain and scale their businesses and remain relevant.”

As technology advances and Australian SMEs have to increasingly compete in a global marketplace, technology will enable brokers to save time and resources – a valuable competitive advantage.

Liu adds, “We understand the importance of transforming from a transaction-based relationship into a relationship-based transaction, where brokers do need to have more understanding of clients’ needs and requirements, finding solutions and giving advice on achieving their objectives.”

“With the competition from fintechs, the skill of utilising technology will be key, and how we apply technology to better create the customer experience and maintain the relationship is going to drive future transactions,” he explains.

“This will also empower brokers to explore more opportunities, not only for the finance transaction but by also providing more add-on services around the transaction from industry partners to comprehensively take care of all their related needs.”

Key skills

All of the above means there could be a significant amount of consolidation in the broking industry, suggests Gortan.

“Single operators will find it more difficult to compete against large players, especially with the compliance costs, processing times and economies of scale,” he says.

In such a competitive environment, brokers will need to have the right tools and support in place to adapt to the changes looming ahead.

Mitchell reiterates, “Brokers will need the right tech tools to allow them to implement a smooth operational process in order to save time and deliver a consistent, high level of customer service.

“They will also need these tools in order to demonstrate that they have met BID. We can expect to see a gradual lift in dwelling values, but we are unlikely to see values return to peak levels,” she adds.

Professional standards are already increasing and will continue to do so; therefore the pressure on brokers to adapt, take market share and drive competition will likewise grow, according to Renee Blethyn, national partnerships manager at Suncorp.

“A continuing trend for brokers in 2020 will be their ability to diversify,” she says.

Indeed, the broker who can build upon their skills, knowledge and capability in SME and commercial lending will be rewarded by more customers and increased opportunities.

“Brokers who can take their business to the next level and take themselves out of their traditional comfort zones stand to benefit the most,” says Blethyn.

There is no question that the next year presents a real opportunity for brokers – and the industry as a whole – to genuinely assist Australians with their biggest financial investments and commitments.

“It’s our collective duty to do this professionally and with honesty, underpinned by a genuine desire to deliver the best customer outcomes,” adds Blethyn.

Housing outlook

How the industry responds to BID regulations will shape many outcomes in 2020 – for the broker, the lender and the customer, says Milburn.

“Essentially, a good broker has nothing to fear from the implementation of BID, but they will need to adapt. Brokers who stay on top of the changes in the industry will surely benefit from adopting early,” he says.

However, when it comes to predicting the outlook for housing, things get a little tricky. But Milburn says there are many reasons to be optimistic about the outlook for housing in 2020.

“Many key markets appear to have bottomed out and are now set to increase in the next few years. A decrease in official interest rates has driven this trend, with people now more willing to re-enter the market,” he says.

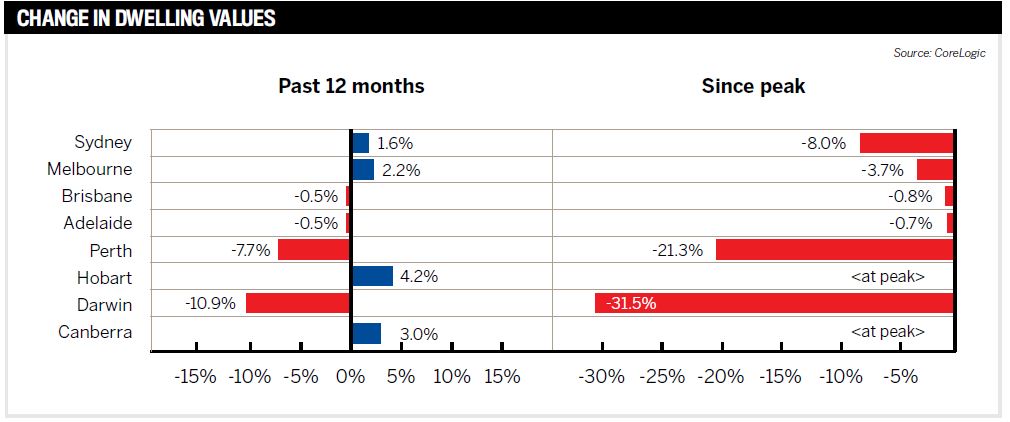

Angus adds that “the trough in our housing market appears to be behind us, as evidenced by improving auction clearance rates in Sydney and Melbourne, alongside the return of monthly home value growth”.

“Fundamentals like these support the outlook for ongoing improvement: the housing market has responded well to the RBA’s cash rate cuts and the corresponding reduction in borrower interest rates,” he says. “Also significant is the easing of macroprudential measures that were at the time designed to constrain the growth in investor lending.”

Overall, Angus says the fundamentals of the housing sector remain sound.

Mitchell concludes: “With the worst now behind us, we should see the last 12 months as a wake-up call: we have been forced to reassess how we operate as an industry, improve our businesses and practices.

According to Bannister, population growth will be the main driver in the market, with an underlying demand for 180,000 new dwellings per annum.

“In recent years, a surge in construction activity in Sydney, Melbourne and Brisbane, in particular, has met that demand and even produced a small excess supply, which has enabled a reduction in dwelling prices over the last two years,” says Bannister.

“As developers progressively complete and then sell existing construction works, there will be no new works coming online, and therefore it is likely we will start to see a structural supply shortfall re-emerging in 12 to 18 months.

“The challenge we face is to ensure that we don’t let these learnings go to waste, and implement the changes we know will enable this industry to continue thriving into the future.”

Finally, first home buyers will benefit from the assistance of the First Home Loan Deposit Scheme commencing on 1 January, Liu points out.

“We’ll see steady growth in existing dwellings, however, the apartment market – especially off-the-plan projects – might still face challenges selling, with concerns surrounding build quality and valuation issues remaining,” he says.

“The main drivers of the housing market will be the accessibility of credit and the demand for properties.”