The loyalty tax in lending has stayed consistent despite the recent rises in interesting rates with existing borrowers paying more on average than new borrowers, according to the RBA’s latest lender’s interest rates data.

Together with the heightened media coverage surrounding changes in the cash rate, Tom Bracey (pictured above), a residential and commercial mortgage broker from Shore Financial, said existing borrowers had become “more aware” of their financial situation and were refinancing earlier.

With hundreds of thousands of homeowners still to come off their fixed rates this year, eliminating the loyalty tax could provide brokers with an additional incentive to promote refinancing.

“With inflation and consistent interest rate rises taking a hit to everyone’s hip pocket, a lot of clients who never really had an idea of what rate they were on are now aware of what they are paying and more often than not noticing that their current rate is well out of the market,” Bracey said.

“The savings on simply looking at refinance options or re-pricing with their current lender can be in the thousands to tens of thousands per year.”

Australian homeowners have experienced significant interest rate fluctuations in recent years.

Some 46% of homeowners jumped on the record low fixed interest rates at its peak during the pandemic, well above the fixed rates historical average of 15%.

But as the RBA hiked the official cash rate by 400 basis points in 13 months, mortgage cliff panic quickly set in across the country.

In its October 2022 Financial Stability Review, the RBA said about 35% of outstanding housing credit was on fixed terms, and roughly two-thirds of this debt was set to expire in 2023.

The market was over-leveraged, with PEXA estimating 800,000 fixed-rate loans were due to expire over the year.

Many of these were expected to land in “mortgage prison”, not being able to refinance due to the steep rate hikes and APRA’s 3% serviceability buffer and would suffer from reduced financial flexibility and increased risk of default.

However, the mortgage cliff has largely failed to materialise.

Refinancing has already peaked in July and PEXA’s Refinance Index, which measures the volume of refinances, has dropped to levels not seen since May.

So far, the refinancing boom hasn't caused widespread arrears, as non-performing loans (NPL), which indicate defaults or near-defaults, have returned to pre-pandemic levels, well below recent highs.

Admittedly, while APRA acknowledged NPLs could rise due to the roll-off of fixed rate loans, any deterioration is “expected to be limited as a resilient labour market and high savings buffers provide most households the ability to continue to service mortgage loans”.

While mortgage stress is growing among homeowners and ASIC has reported a 28% increase in calls to the National Debt Hotline compared to a year, this could also indicate a newfound understanding and level of concern of the homebuyer’s financial situation.

“As clients increasingly scrutinise the pricing of their loans in relation to the broader market, they are becoming more proactive in seeking out favourable terms,” said Bracey.

Lenders also now offer competitive products exempt from the 3% serviceability buffer, prompting many borrowers to refinance who wouldn't have otherwise.

“The competition among lenders, who are fighting for business by offering low rates, not only propels business growth within the market but also makes it easier for clients to achieve considerable savings on their loans,” Bracey said.

So, how does all this relate to the loyalty tax and the opportunity it presents to brokers?

Well, there are around 40% of the low fixed rate home loan terms set to expire by the end of 2024, and another 20% by the end of next year.

For this group of borrowers, brokers could add value by explaining their potential savings by refinancing and removing the loyalty tax.

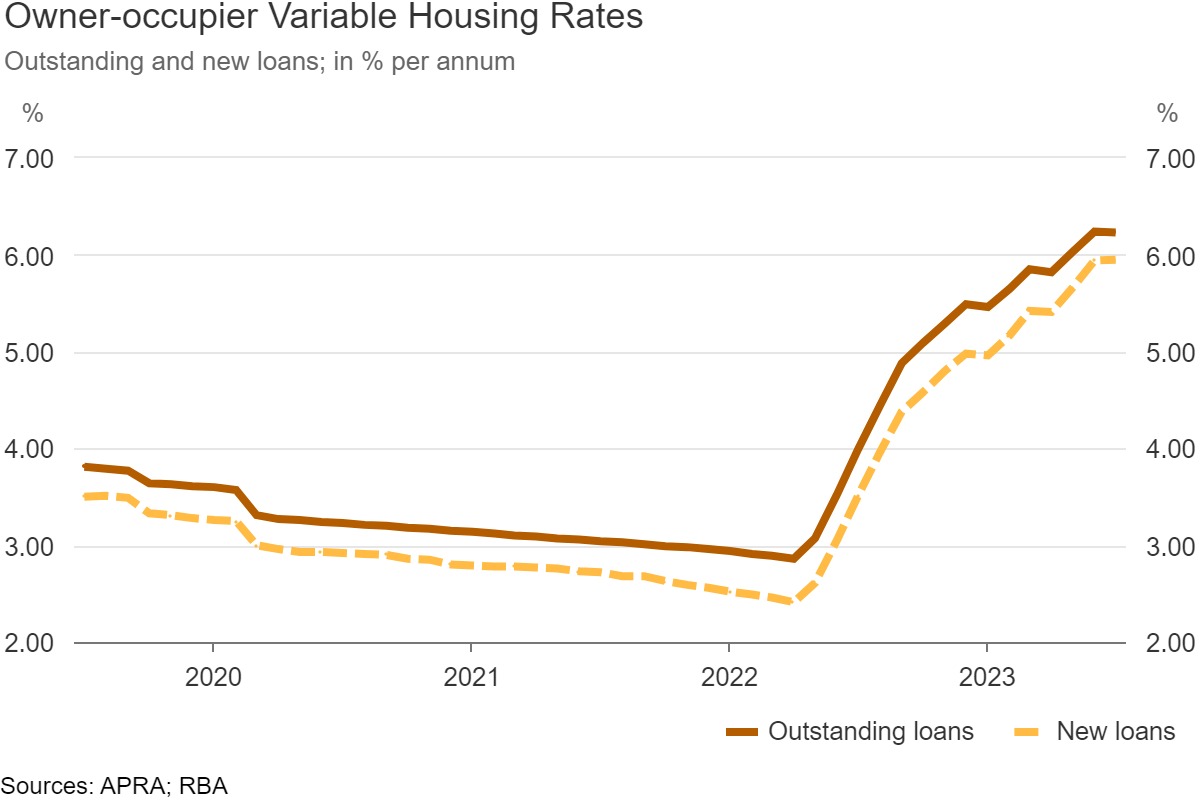

In July, existing borrowers were paying an average variable rate of 6.23% while new customers were paying 5.95% – a gap of 0.28%, according to the RBA.

However, on the ground, Bracey said he was seeing most owner-occupied clients with principal and interest (P&I) repayments land at around 5.79% which then widens the gap to 0.44%.

Bracey said this made the savings on refinancing “quite considerable”.

For example, on a $500,000 loan, clients could expect to save $142 on monthly repayments or an annual savings of $1,704 simply through refinancing and avoiding the loyalty tax.

For a $3 million loan, annual savings would reach $10,188 – a significant amount and a significant incentive to refinance.

Bracey said there were a few approaches Shore Financial took to help existing borrowers take advantage of these interest rate differentials.

“We regularly review our client portfolios and stay up to date with market trends, interest rate movements, and changes in lending products and policies,” he said.

“I’d recommend for brokers to negotiate with their clients’ current lenders, to be proactive not reactive, and to monitoring property trends to see if an uplift on the existing property could result in better pricing.”

What do you think about the issues discussed in the article? Comment below.