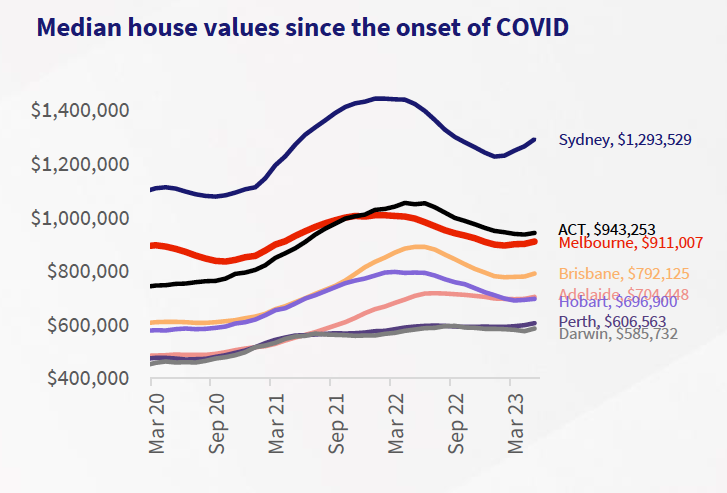

Between the onset of COVID-19 in March 2020 and the end of May 2023, Melbourne house values have risen by just 1.6%, significantly lower than the double-digit growth seen in every other capital city – from Sydney’s 16.5% to the 45.2% surge in Adelaide house values during that period.

But while Melbourne’s substantially lower growth rate may be a cause of disappointment for Melbourne homeowners, the city’s sluggish conditions can be an attractive affordability advantage for buyers, according to Tim Lawless (pictured above), research director at CoreLogic Australia.

When it comes to house prices, Sydney has always had the upper hand in its legendary rivalry with Melbourne, Lawless said.

“In March 2020, at the onset of COVID, Melbourne house values were 19.2% cheaper than Sydney’s,” he said. “By April 2022 the gap between Sydney and Melbourne house values had blown out to 30.3% – the biggest divergence since May 2006. The gap has closed a little since then, however, Melbourne’s median house value was 29.6% behind Sydney’s in May 2023, or the dollar equivalent of roughly $382,500.”

All capital cities but Canberra – the country’s second-most expensive capital city for houses – have significantly closed the house value gap to Melbourne. Brisbane houses were 47% cheaper than Melbourne at the onset of COVID, but that affordability gap has closed to just 15%. When compared with Adelaide, Melbourne was 85% more expensive, but the gap narrowed to just 29%. In Perth, where the gap was 88%, Melbourne house values are now just 50% more expensive.

Less substantial swings and roundabouts

Lawless said the under-performance of Melbourne house values relative to other capital cities was due to a combination of factors.

“The city experienced a more substantial drop in value than other capitals through the early stages of COVID, it recorded a softer increase through the upswing and there’s been a significant decline in values through the rate hiking cycle to-date,” he said.

“Melbourne house values fell by -6.7% between March 2020 and October 2020, before surging 20.6% through the growth cycle. House values subsequently fell by -11.2%, finding a floor in February this year. Since February, Melbourne house values have risen by 1.7% to the end of May 2023.”

Melbourne’s softer housing market conditions through the pandemic cycle coincided with a sharp decline in demographic trends, with both net overseas and interstate migration rates plummeting through the pandemic to hit record lows, lowering housing demand amid a series of lockdowns associated with the pandemic.

But with Australia’s annual net overseas migration surging to new record highs and Victoria’s first possible rise in interstate migration after 10 consecutive quarters of decline since Q1 2020, housing demand across Melbourne has begun to strengthen substantially, Lawless said.

“With housing affordability remaining stretched, this improvement in Melbourne’s value proposition could place Australia’s second largest city in a more competitive position to attract a greater share of housing market participants,” Lawless said.

Melbourne’s advertised supply level is down -13.4% compared to the same time last year and down -7% than the previous five-year average. That and the city’s rental vacancy rate now at 0.8%, which is one of the lowest in the country, are factors that potentially support purchasing demand for would-be buyers.

“Whether Melbourne’s strong demand, low supply and a relative affordability advantage can completely offset the impact of high interest rates remains uncertain,” Lawless said. “Demand from overseas migration is likely to remain a feature of the market for the next few years, however borrower’s access to credit will be challenging while interest rates are high.

“Additionally, it’s possible more homeowners choose, or need, to sell due to the substantial increase in mortgage repayments over the past 13 months alongside persistently high cost-of-living pressures. Any marked rise in new listings could add downwards pressure to housing prices.”

Use the comment section below to tell us how you felt about this.