With one in five of the mortgage industry’s 19,000 brokers not writing a loan within a six-month period, alarm bells are ringing over what this might mean for the industry.

Australian Broker asked some mortgage industry experts about why this might be occurring and what the industry can do about it in 2024.

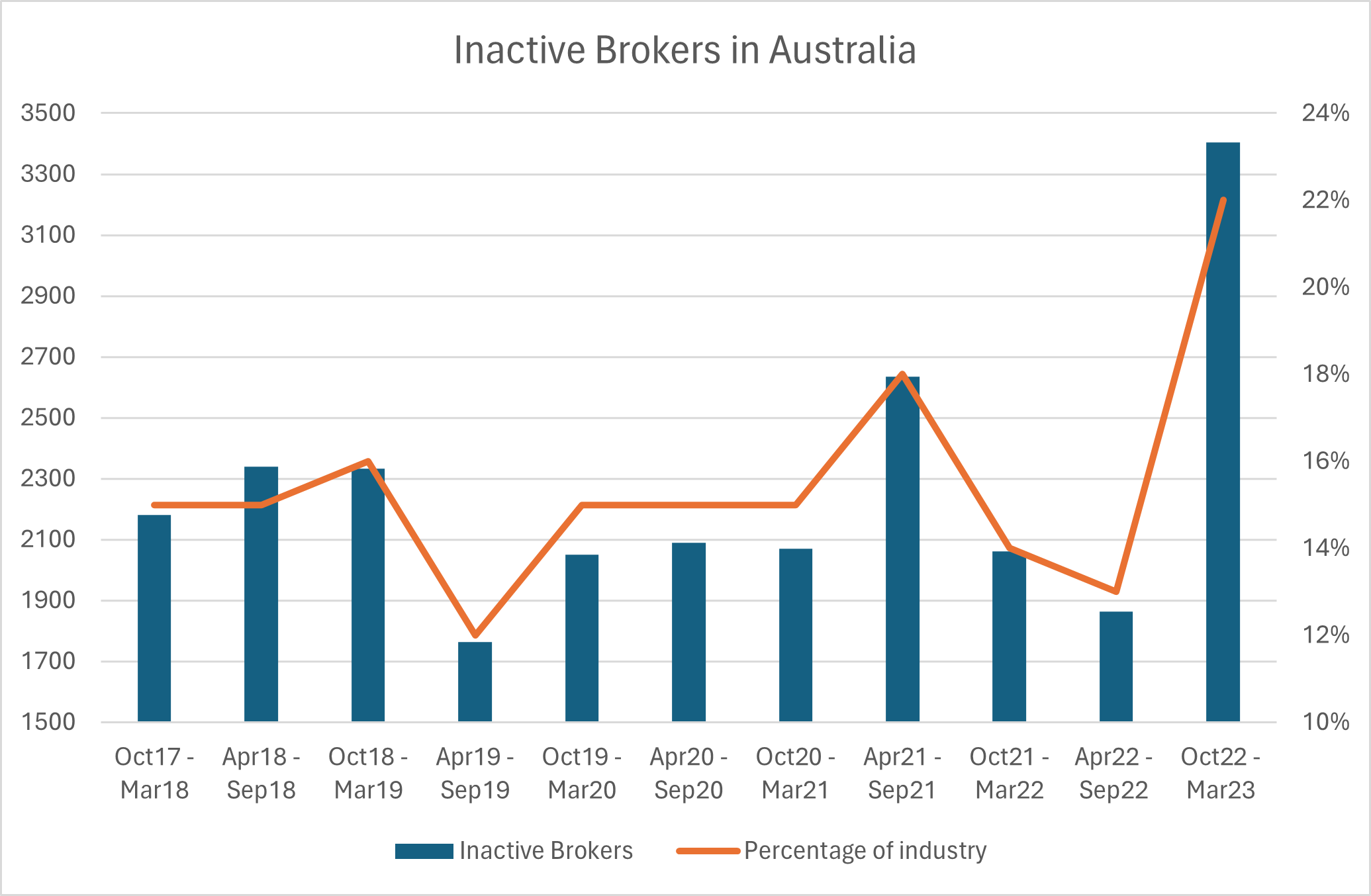

Over 3,400 Australian mortgage brokers did not settle a loan between October 2022 and March 2023, according to the MFAA Industry Intelligence Service (IIS) 16th edition report.

This inactivity rate nearly doubled compared to the previous six months and marked the first significant increase in inactive brokers ever observed.

The MFAA data is based on information from 11 leading aggregators: AFG, Choice Aggregation, FAST, nMB, Mortgage Choice, Loan Market, Finsure, Lendi Group, Vow Financial, PLAN Australia, and Connective.

Although the MFAA’s IIS reports have monitored broker inactivity for many years, it doesn't delve into the specific reasons behind its ups and downs. What it does show, however, is the recent surge in inactive brokers coincides with a drop in overall productivity.

Over the six-month period, (October 2022 to March 2023), mortgage brokers secured only $161.79 billion in residential loans, a significant 8.63% decline compared to the same period last year.

While specific data about individual inactive brokers (like experience, loan volume, or succession plans) would be helpful, mortgage broker Lukas Best (pictured above left) suggests several possible reasons for this trend.

“I wouldn’t discount a theory that after a rapid-fire period of change that involved the Royal Commission, the pandemic, best interests duty, an increasing interest rate, and all of the challenges that came and exist still with running a business and meeting client needs throughout all of it,” said Best, director of Best Financial Solutions.

“Many brokers may simply be experiencing burnout and wondering if this industry remains a worthwhile venture for them.”

Peter Nikolaou (pictured above centre), commercial finance broker at Peak Capital, agreed that the rise in inactive brokers was due to the Australian market’s current rate rising cycle.

“Interest rates have been rising, so less transactions are taking place,” Nikolaou said. “The banks have also removed cashback offers which removes the refinance market.”

“With the higher interest rates, customers don't meet the current lending criteria to refinance and are now in mortgage prison.”

These factors would lead to fewer loans to write and brokers that don't have a large network or referrals partners would be finding it difficult to write new loans, according to Nikolaou.

“In the good times, everyone makes money. In the bad times, you see the weak players fall by the wayside.”

If burnout is in indeed a contributing factor to a current rise in inactivity amongst brokers, Best said he’d encourage them to reach out to fellow brokers for guidance during troubled times.

“According to figures from the MFAA, almost half of mortgage broker businesses have a single loan writer within them so it stands to reason that for a lot of brokers they would feel quite isolated and that they don’t have a lot of colleagues to turn to for support, but it doesn’t have to be this way,” Best said.

“I’ve always kept a close cohort of brokers around me that I’ve developed relationships with during my business journey and we consistently check in with each other throughout the good times and bad.

“It’s certainly kept me motivated and educated to ensure I rise to the demands of an ever-changing broking landscape.”

For these inactive, possibly burned-out brokers to continue to write loans, Nikolaou said they needed to invest in marketing themselves and their business within their local market and online.

“They need to create partnerships and use the aggregator systems and processes to identify new opportunities.”

While there's no readily available data on the exact number of mortgage brokers who retire each year in Australia, anecdotal evidence suggests broker inactivity may be due to a large number of long-term brokers retiring, according to the personal opinion of mortgage broker Kerri Buurman (pictured above right).

According to the Australian Bureau of Statistics, the average age of retirement in Australia is 64.3 years. This can offer a rough estimate of the age at which some mortgage brokers might choose to retire.

“They may be holding onto the trail book, but not actively writing new business,” said Buurman who is also an MFAA non-executive chairperson.

Buurman also agreed with Best, saying that brokers who only write the occasional deal are finding the current economic climate more difficult and may not be actively sourcing new business.

While there’s not much to be done about retiring brokers, Buurman said the industry needed to move away from solo brokers and bring them into existing businesses.

“This will help them to grow and scale as they would have support of other brokers around them and admin staff to assist with processing and general admin,” Buurman. “It's far more sustainable than continuing to operate solo and also provides more security and stability for consumers.”

Whether its burnout, the current market environment, or brokers retiring en masse, one thing is clear: the state of being a mortgage broker is changing.

The industry may need to prioritise open communication within the industry to prevent adverse effects on both mortgage brokers and, more importantly, their clients.

Why do you think broker inactivity has risen? Comment below.