While many borrowers are struggling with interest rates reaching its peak, one NAB staffer has helped a 19-year-old enter the property market in a move that suggests there is still room for the younger generation to climb Australia’s crowded property ladder.

NAB home lending executive Fayaz Meghani (pictured above) said he discussed strategies with now-property owner, Josh, after he showed interest in becoming a homeowner several months ago.

“After meeting with Josh, we discussed strategies, how to create wealth, lay down the plans to buy his first home and take advantage of the home guarantee scheme at 5% with no LMI,” Meghani said.

A couple of weeks ago, Meghani helped Josh settle his first home and officially became his “youngest ever homeowner” client.

“My advice to parents and young adults is to start early,” Meghani said. “Time is critical to wealth creation. Small steps. You don’t need to buy $1.5 million Sydney home as your first home. Just get in the market and build your wealth.”

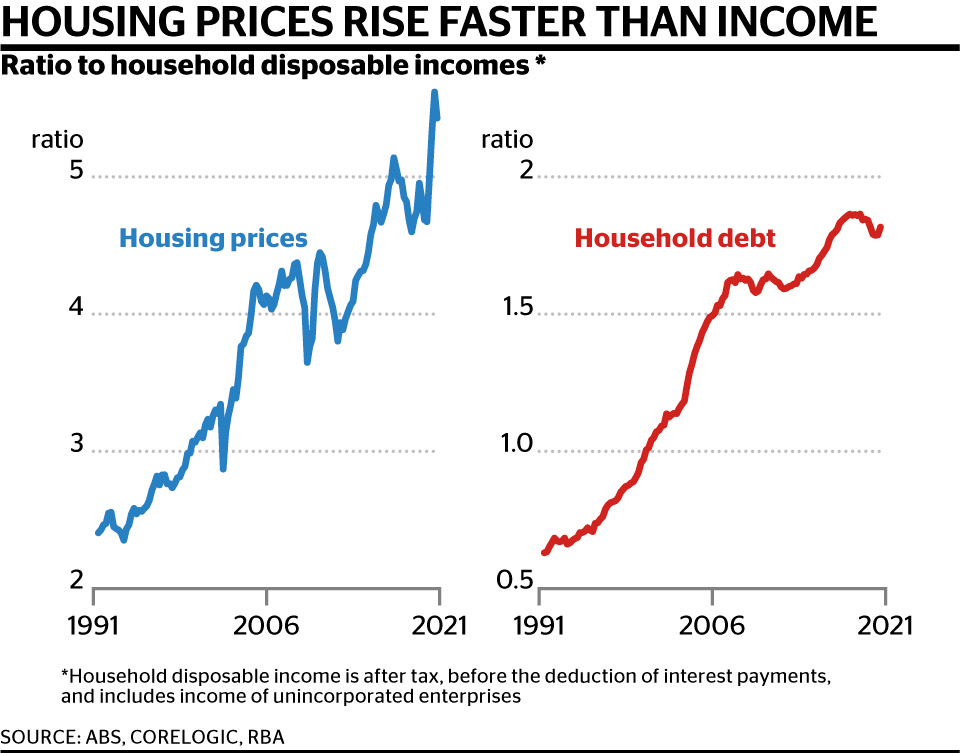

With property prices skyrocketing over the past few decades compared to subdued increases in income, it’s little wonder that many younger Australians have found it difficult to get a foothold on the property ladder.

In 1991, housing prices were around 2.5 times household disposable incomes, according to RBA data. By 2021, the same metric had risen to 5.5.

Consequentially, 2022 ABS data found only 55% of Millennials, 25 to 39 year olds, are homeowners compared with 62% of Generation X and two thirds (66%) of Baby Boomers when they were the same age.

Add in the recent increase in interest rates and now more than two-thirds of young people (25 to 34-year-olds) don’t believe they will ever own a home, according to a February survey by Resolve Strategic.

While the challenges are tough for many young prospective buyers, Meghani said it was not insurmountable for many with a proper plan in place.

“Purchasing a property is usually the biggest transaction a customer will experience in their lifetime, so it is a decision that shouldn’t be taken lightly without careful planning and having clear strategies in place,” Meghani said.

Meghani said the two key challenges that young people generally faced were borrowing capacity and savings.

While the median house and unit price for Sydney, where Meghani primarily operates, is around $1.33 million and $817,000 respectively, Meghani said the focus should be on “what we can control” and “how to enter the market sooner rather than later”.

“I’ve had many conversations over the years with young first home buyers who have set themselves an expectation to buy a $1.5m property but they can only borrow one-third of that. I’ve followed up with some of these first home buyers after a couple of years and they’ve stagnated without making any progress, being in the same position as they were a few years ago,” Meghani said.

“My key message to first home buyers is to have a conversation to work out your borrowing capacity, set a realistic expectation on a purchase price, start somewhere small and gradually build on to that.”

With potential homebuyers far from optimistic about their prospects of buying a home, it’s largely up to those in the industry to underscore the importance of homeownership and provide a path forward.

Meghani said discipline and focus were foundational attributes for aspiring young homeowners. He urged brokers and lending executives to help their clients adopt a “rigorous routine for money management”, utilising tools for effective budgeting, and gaining control over expenses.

“Everybody knows how much money is coming into their bank account on pay day but not everybody knows how to control how much money is going out. That’s budgeting 101,” Meghani said.

“Avoid buy now pay later – if they need to pay something later, that means they have cash flow problem. They need to get into the mindset of treating their income like a business. Don’t spend what you don’t have. If there is something you want, ask yourself – is this something you need?”

Meghani said he had seen firsthand how buying a home had helped customers build wealth over the past three years.

Another way for the industry to add value is to promote first home buyer schemes and other incentives, which often reduce the deposit amount and remove LMI and stamp duty, as many may not understand the value, said Meghani.

“I recently had a customer that bought a $800,000 property under the Home Guarantee Scheme. The customers managed to save $31,000 on stamp duty and potentially $25,000 on LMI if it wasn’t for the incentives that are available today.”

Another key option for young people is to tap into the bank of mum and dad.

A recent Finder Parenting Report indicated that around 50% of parents are willing to contribute to their children’s future home deposits, with an average planned contribution of $33,278.

“We’re now seeing people working until the age of 70 so if you’re purchasing your first property at 20, you’ve got 50 years to potentially capitalise of capital growth,” Meghani said.

“This is the power of compound growth over time which Albert Einstein has once called the eighth wonder of the world. Obviously, I don’t want to see my customers working till they’re 70 years of age as I hope I can help them retire early through property investing.”

While not every client will have the circumstances to buy a property at 19, there may be a path towards homeownership for many young people that they may not have considered.

Meghani said the opportunity was there for the industry to fill this gap and help younger Australians enter the property market “as soon as possible” with a long-term plan in place.

“By building equity in your property as early as possible, it can help protect you in later stages of life when we start to juggle more responsibilities, such as raising a family, or if we face job insecurity or market fluctuations, for example,” Meghani said.

“Taking steps towards homeownership early on in life can help smooth out the bumps in the road and hopefully avoid the panic that may come to many who face such changes.”

Have you got a mortgage win you’d like to share? Email me at [email protected]

What do you think about this article? Comment below.